Car Payment Calculator

Auto loan payment estimator • 2026 rates

Car Payment Formula:

Show the calculator\( CP = \frac{L \times r \times (1 + r)^n}{(1 + r)^n - 1} \)

Where:

- \( CP \) = Car Payment

- \( L \) = Loan Amount (Vehicle Price - Down Payment)

- \( r \) = Monthly Interest Rate (Annual Rate ÷ 12)

- \( n \) = Number of Payments (Loan Term in Months)

This formula calculates the fixed monthly payment required to fully pay off a car loan over the specified term, accounting for compound interest. It helps determine affordable payment amounts before purchasing a vehicle.

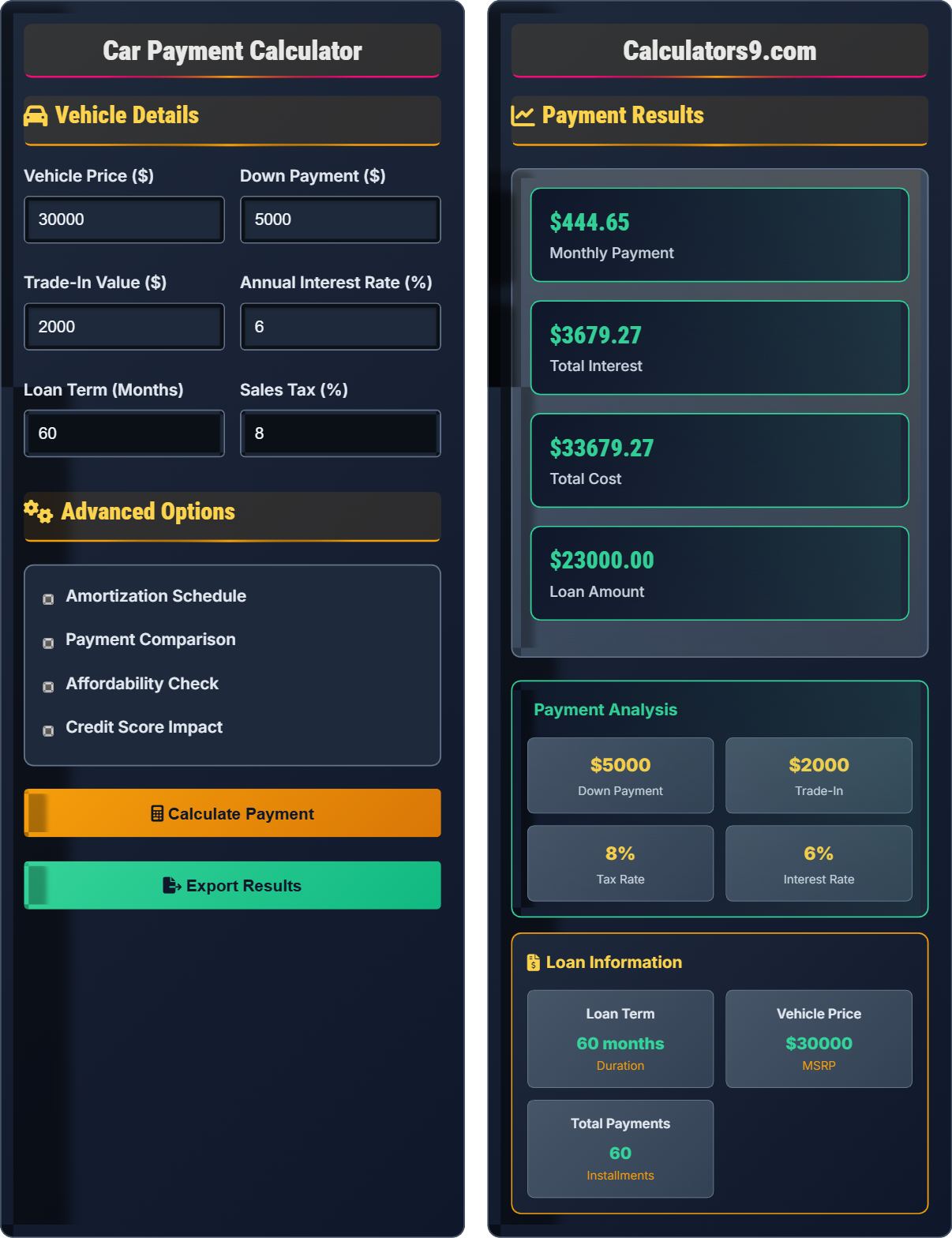

Example: For a $30,000 car with $5,000 down payment, 6% annual interest rate, and 60-month term:

Loan Amount = $30,000 - $5,000 = $25,000

Monthly Rate = 6% ÷ 12 = 0.005

Number of Payments = 60

\( CP = \frac{25{,}000 \times 0.005 \times (1 + 0.005)^{60}}{(1 + 0.005)^{60} - 1} \)

\( CP = \frac{25{,}000 \times 0.005 \times 1.3489}{1.3489 - 1} = \frac{168.61}{0.3489} = \$483.29 \)

Thus, the monthly car payment would be approximately $483.29.

Vehicle Details

Advanced Options

Payment Results

Car Payment Planning Guide

A car payment is the monthly amount paid to a lender to repay an auto loan. It includes principal (the amount borrowed) and interest (the cost of borrowing). Understanding your car payment helps determine how much vehicle you can afford while maintaining financial stability. The payment amount depends on the loan amount, interest rate, and loan term.

The standard car payment calculation uses the following formula:

Where:

- \(CP\) = Car Payment

- \(L\) = Loan Amount

- \(r\) = Monthly Interest Rate

- \(n\) = Number of Payments

Current auto loan trends and benchmarks:

- Average Interest Rate: 6.5-8.5% for new cars

- Typical Loan Terms: 60-72 months for new, 48-60 for used

- Recommended Down Payment: 20% for new, 15% for used

- Payment-to-Income Ratio: No more than 10-15%

- Loan-to-Value Ratios: 80-85% preferred by lenders

- Shop Around: Compare rates from multiple lenders

- Improve Credit: Boost score before applying for better rates

- Shorter Terms: Choose shorter terms to save on interest

- Substantial Down: Put down 20% to avoid negative equity

- Consider Used: Certified pre-owned offers better value

Payment Calculation

Monthly installment paid to repay an auto loan, including principal and interest.

\(CP = \frac{L \times r \times (1 + r)^n}{(1 + r)^n - 1}\)

Where CP=payment, L=loan amount, r=monthly rate, n=number of payments.

- Lower interest rates save money

- Higher down payments reduce payments

- Shorter terms save on interest

Financing Planning

Loan amount as percentage of vehicle value, indicating lending risk.

- Calculate 10% of monthly income

- Subtract other debt payments

- Ensure payment fits in budget

- Consider insurance and maintenance

- Plan for unexpected expenses

- Insurance costs increase payment

- Maintenance costs apply

- Depreciation affects equity

- Tax and registration apply

Car Payment Learning Quiz

A buyer is considering a $35,000 car with a $7,000 down payment and $3,000 trade-in value. The loan has a 5.5% annual interest rate and a 6-year term. Calculate the monthly payment, total interest paid, and total cost of the loan. Show all calculations and explain how changing the loan term to 4 years would affect these values.

Step 1: Calculate Loan Amount

Loan Amount = Vehicle Price - Down Payment - Trade-in Value

Loan Amount = $35,000 - $7,000 - $3,000 = $25,000

Step 2: Convert Annual Rate to Monthly Rate

Monthly Rate = Annual Rate ÷ 12

Monthly Rate = 5.5% ÷ 12 = 0.055 ÷ 12 = 0.004583

Step 3: Calculate Number of Payments

Number of Payments = Loan Term (years) × 12

Number of Payments = 6 years × 12 = 72 payments

Step 4: Apply Car Payment Formula

\( CP = \frac{L \times r \times (1 + r)^n}{(1 + r)^n - 1} \)

\( CP = \frac{25{,}000 \times 0.004583 \times (1 + 0.004583)^{72}}{(1 + 0.004583)^{72} - 1} \)

\( CP = \frac{25{,}000 \times 0.004583 \times 1.3895}{1.3895 - 1} \)

\( CP = \frac{159.37 \times 1.3895}{0.3895} = \frac{221.44}{0.3895} = \$568.53 \)

Step 5: Calculate Total Interest and Cost

Total Payments = Monthly Payment × Number of Payments

Total Payments = $568.53 × 72 = $40,934.16

Total Interest = Total Payments - Loan Amount

Total Interest = $40,934.16 - $25,000 = $15,934.16

Total Cost = Vehicle Price + Total Interest

Total Cost = $35,000 + $15,934.16 = $50,934.16

Step 6: Compare with 4-Year Term

Number of Payments = 4 years × 12 = 48 payments

\( CP = \frac{25{,}000 \times 0.004583 \times (1 + 0.004583)^{48}}{(1 + 0.004583)^{48} - 1} \)

\( CP = \frac{25{,}000 \times 0.004583 \times 1.2454}{1.2454 - 1} = \frac{140.92}{0.2454} = \$574.25 \)

Total Interest (4-year) = ($574.25 × 48) - $25,000 = $27,564 - $25,000 = $2,564

Monthly Payment (6-year): $568.53, Total Interest: $15,934.16

Monthly Payment (4-year): $574.25, Total Interest: $2,564

The 4-year term has a slightly higher monthly payment but saves $13,370.16 in interest over the life of the loan.

This problem demonstrates the trade-off between monthly payments and total interest costs. The longer loan term results in lower monthly payments but significantly higher total interest paid over the life of the loan. The mathematical relationship shows how compound interest accumulates over time, making shorter terms more cost-effective despite higher monthly payments. The calculation emphasizes how small changes in loan terms can result in substantial differences in total cost.

Loan Amount: The principal amount borrowed after down payment and trade-in

Compound Interest: Interest calculated on both principal and accumulated interest

Amortization: Gradual repayment of loan through regular installments

• Longer terms reduce monthly payments but increase total interest

• Shorter terms save money on interest

• Monthly payment includes both principal and interest

• Even small increases in down payment significantly reduce total cost

• A few basis points in interest rate can save thousands

• Consider the total cost, not just monthly payment

• Focusing only on monthly payment instead of total cost

• Not considering the impact of loan term on total interest

• Forgetting to convert annual rate to monthly rate

A buyer with a credit score of 620 qualifies for a 7.5% interest rate on a $28,000 car loan for 60 months. If they improve their credit score to 720, they would qualify for a 4.5% rate. Calculate the difference in monthly payments and total interest paid between these two scenarios. How much would the buyer save over the life of the loan by improving their credit score?

Scenario 1: Credit Score 620 (7.5% Rate)

Monthly Rate = 7.5% ÷ 12 = 0.00625

Number of Payments = 60

\( CP = \frac{28{,}000 \times 0.00625 \times (1 + 0.00625)^{60}}{(1 + 0.00625)^{60} - 1} \)

\( CP = \frac{28{,}000 \times 0.00625 \times 1.4533}{1.4533 - 1} = \frac{254.33}{0.4533} = \$561.06 \)

Total Interest = ($561.06 × 60) - $28,000 = $33,663.60 - $28,000 = $5,663.60

Scenario 2: Credit Score 720 (4.5% Rate)

Monthly Rate = 4.5% ÷ 12 = 0.00375

\( CP = \frac{28{,}000 \times 0.00375 \times (1 + 0.00375)^{60}}{(1 + 0.00375)^{60} - 1} \)

\( CP = \frac{28{,}000 \times 0.00375 \times 1.2513}{1.2513 - 1} = \frac{131.39}{0.2513} = \$522.84 \)

Total Interest = ($522.84 × 60) - $28,000 = $31,370.40 - $28,000 = $3,370.40

Difference Calculation:

Monthly Payment Difference = $561.06 - $522.84 = $38.22

Total Interest Difference = $5,663.60 - $3,370.40 = $2,293.20

By improving their credit score from 620 to 720, the buyer would save $38.22 per month and $2,293.20 over the life of the loan. This demonstrates the significant financial impact of credit scores on auto financing costs.

This problem illustrates how credit scores directly impact loan costs. The 3 percentage point difference in interest rates resulted in nearly $2,300 in savings over the loan term. This quantifies the value of credit improvement efforts before financing. The calculation shows that even modest improvements in credit scores can yield substantial savings, making credit score enhancement a valuable financial strategy before major purchases.

Credit Score: Numerical expression of creditworthiness (300-850 range)

Interest Rate: Percentage charged for borrowing money

Credit Risk: Likelihood that borrower will default on loan

• Higher credit scores qualify for lower interest rates

• Check credit reports for errors before financing

• Pay down existing debts to improve credit utilization

• Avoid opening new credit accounts before major purchases

• Not checking credit score before applying for loans

• Accepting first financing offer without shopping around

• Not understanding how credit scores affect rates

FAQ

Q: What's the difference between APR and interest rate, and how do they affect my car payment?

A: Understanding the difference between APR and interest rate is crucial for car financing:

Interest Rate:

- Definition: Pure cost of borrowing money, expressed as a percentage

- Calculation: Based solely on the principal loan amount

- Examples: 4.5%, 6.0%, 8.5%

- Impact: Directly affects monthly payment calculation

- Factors: Credit score, loan term, down payment

APR (Annual Percentage Rate):

- Definition: Total cost of borrowing including interest and fees

- Calculation: Interest rate + origination fees, processing fees, etc.

- Examples: 4.7%, 6.3%, 9.1%

- Impact: More accurate representation of true borrowing cost

- Required Disclosure: Lenders must show APR by law

Impact on Car Payment:

- Payment Calculation: Use interest rate for monthly payment formula

- Comparison Shopping: Use APR to compare loan offers

- True Cost: APR reflects total cost including fees

- Transparency: APR provides complete picture of borrowing cost

Practical Example: A loan with 5% interest rate and $500 in fees might have an APR of 5.2%. When comparing lenders, focus on APR for the complete cost picture, but use the interest rate in payment calculations.

Q: How should I determine what percentage of my income to allocate to car payments, and what other costs should I consider?

A: Determining appropriate car payment allocation requires comprehensive budget analysis:

Income Allocation Guidelines:

- 28/36 Rule: Housing + Debt ≤ 36% of gross income

- Car Payment Specific: No more than 10-15% of gross monthly income

- Conservative Approach: 8-10% for financial flexibility

- Aggressive Approach: Up to 20% only if no other debt

- Emergency Fund: Maintain 3-6 months expenses before large purchases

Additional Car-Related Costs:

- Insurance: $100-300+ monthly depending on vehicle and driver profile

- Fuel: $100-300+ monthly depending on driving habits and vehicle efficiency

- Maintenance: $75-200 monthly for newer vehicles, more for older ones

- Registration/Taxes: Annual costs of $100-500+

- Parking/Tolls: $20-100+ monthly in urban areas

Comprehensive Budget Analysis:

- Total Vehicle Cost: Payment + Insurance + Fuel + Maintenance

- Ratio Calculation: Total vehicle costs ÷ Gross monthly income

- Debt-to-Income: All debt payments ÷ Gross monthly income

- Disposable Income: Ensure adequate funds for other expenses

Financial Planning Tips:

- Rule of Thumb: Keep total vehicle costs below 15-20% of income

- Consider Depreciation: New cars lose 20-30% value in first year

- Certified Pre-Owned: Offers better value than new cars

- Long-term Impact: Consider opportunity cost of payments

Example: For $5,000 monthly income, car payment should not exceed $500-750, with total vehicle costs ideally under $1,000.