Customer Acquisition Cost Calculator

CAC calculator • 2026 metrics

Customer Acquisition Cost Formula:

Show the calculator\( CAC = \frac{\text{Total Marketing Spend} + \text{Sales Expenses}}{\text{New Customers Acquired}} \)

\( LTV:CAC \text{ Ratio} = \frac{\text{Customer Lifetime Value}}{\text{Customer Acquisition Cost}} \)

Where:

- \( CAC \) = Customer Acquisition Cost

- Total Marketing Spend includes advertising, campaigns, promotions

- Sales Expenses include salaries, commissions, tools

- New Customers Acquired = number of customers gained in period

- LTV:CAC ratio indicates marketing efficiency

This formula calculates the average cost to acquire a new customer, helping businesses evaluate marketing effectiveness and optimize spending.

Example: For a company spending $50,000 on marketing and $20,000 on sales to acquire 1,000 customers:

\( CAC = \frac{50,000 + 20,000}{1,000} = \frac{70,000}{1,000} = 70 \)

If the Customer Lifetime Value is $210: LTV:CAC = $210:$70 = 3:1

Thus, the customer acquisition cost is $70 per customer with a 3:1 LTV:CAC ratio.

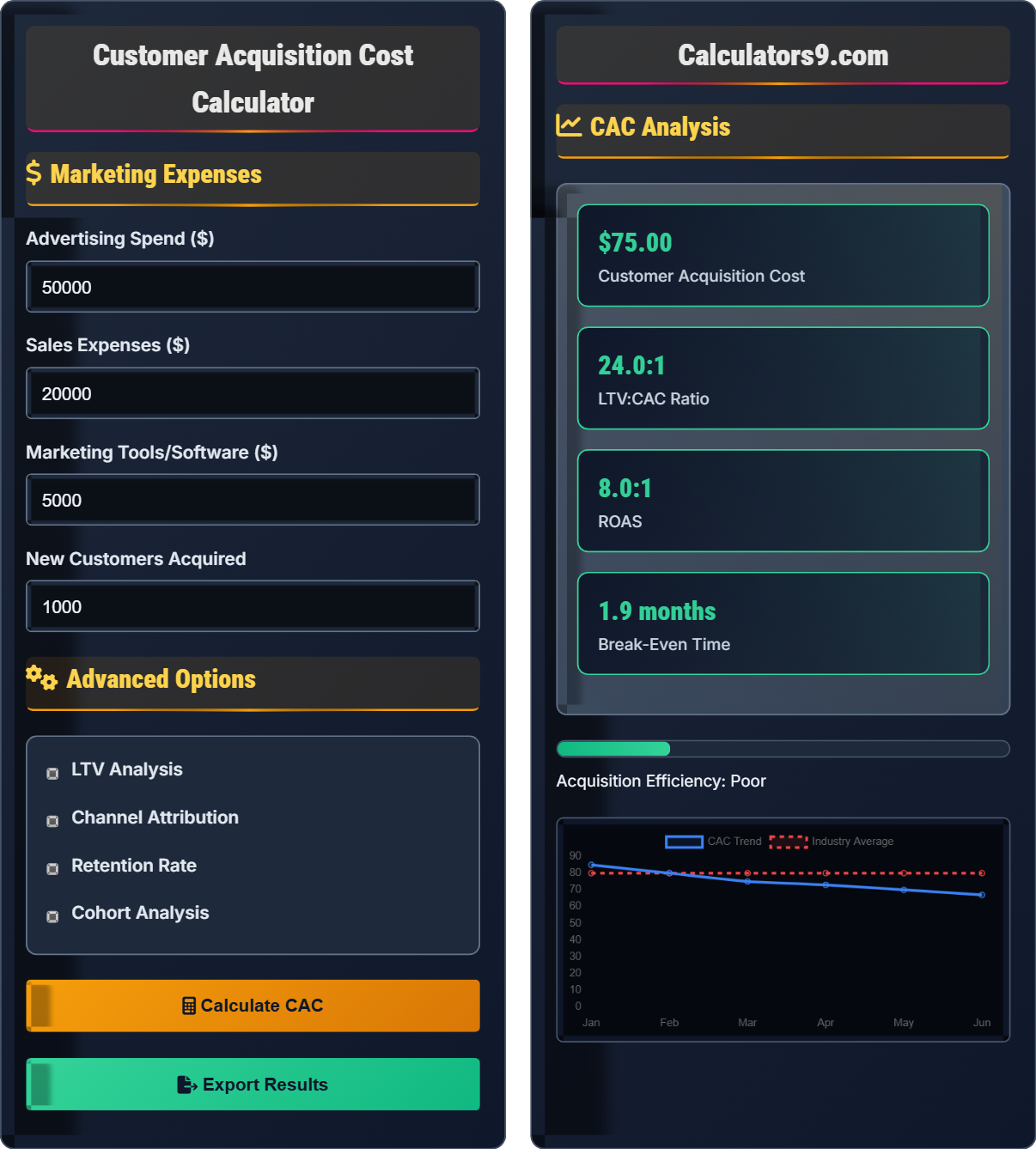

Marketing Expenses

Advanced Options

CAC Analysis

Acquisition Efficiency: Good

| Metric | Formula | Value | Industry Benchmark | Interpretation |

|---|

| Channel | Spend | Customers | CAC | Efficiency |

|---|

Comprehensive Customer Acquisition Guide

Customer Acquisition Cost (CAC) is the total cost associated with acquiring a new customer, including all marketing and sales expenses. It's a critical metric for evaluating the efficiency of customer acquisition efforts and determining the sustainability of growth strategies. Understanding CAC helps businesses optimize marketing spend, set pricing strategies, and measure the effectiveness of different acquisition channels.

The basic CAC calculation uses the following formulas:

Where:

- Marketing Expenses include advertising, campaigns, content creation

- Sales Expenses include salaries, commissions, tools, training

- LTV:CAC ratio of 3:1 is generally considered healthy

- ROAS of 3:1 or higher indicates good marketing efficiency

Acceptable CAC varies significantly across industries:

- SaaS: LTV:CAC ratio of 3:1 to 5:1 is considered healthy

- E-commerce: CAC typically ranges from $10-100 depending on niche

- Mobile Apps: CAC can range from $1-50 based on category

- Financial Services: Higher CAC due to regulatory compliance and longer sales cycles

- Education: High CAC due to consideration period and high-value transactions

- Retail: Lower CAC with focus on volume and repeat purchases

- Channel Optimization: Allocate more budget to channels with lowest CAC

- Retargeting: Focus on high-intent prospects who've shown interest

- Content Marketing: Build organic traffic to reduce paid acquisition dependence

- Referral Programs: Leverage existing customers for low-cost acquisition

- Improved Landing Pages: Increase conversion rates to reduce CAC

- Lookalike Audiences: Target prospects similar to existing customers

CAC Fundamentals

Cost to acquire a new customer including all marketing and sales expenses.

CAC = \(\frac{\text{Total Marketing + Sales Expenses}}{\text{New Customers Acquired}}\)

LTV:CAC = \(\frac{\text{Customer Lifetime Value}}{\text{CAC}}\)

- Lower CAC is generally better

- LTV:CAC ratio should be 3:1 or higher

- Track CAC by channel for optimization

Analysis Framework

CAC measures acquisition cost; LTV measures customer value over time.

- Calculate CAC for each channel

- Estimate Customer Lifetime Value

- Compare LTV:CAC ratios

- Optimize budget allocation

- Seasonal variations affect CAC

- Long-term customer value matters

- Quality of customers varies by channel

Customer Acquisition Learning Quiz

A company spent $30,000 on digital advertising, $15,000 on sales commissions, and $5,000 on marketing software. They acquired 500 new customers. What is their CAC?

The answer is D) $100. To calculate CAC: Total Marketing + Sales Expenses = $30,000 + $15,000 + $5,000 = $50,000. New Customers Acquired = 500. CAC = $50,000 / 500 = $100 per customer. This calculation includes all costs associated with customer acquisition, not just advertising spend.

This problem teaches students to include all acquisition-related expenses in the CAC calculation. Many people mistakenly think CAC only includes advertising costs, but it should encompass all expenses related to customer acquisition, including sales commissions, marketing tools, and other related costs. The comprehensive approach ensures accurate measurement of acquisition efficiency.

CAC: Customer Acquisition Cost - total cost to acquire one customer

Marketing Expenses: Costs related to attracting prospects

Sales Expenses: Costs related to converting prospects to customers

• Include all acquisition-related expenses in CAC

• CAC should be calculated per customer acquired

• Consider both marketing and sales costs

• List all acquisition-related expenses

• Include indirect costs like tools and overhead

• Calculate CAC for each marketing channel separately

• Only including advertising costs

• Forgetting sales commissions and tools

• Not tracking CAC by channel

Explain the relationship between Customer Lifetime Value (LTV) and Customer Acquisition Cost (CAC), including the significance of the LTV:CAC ratio. Provide a mathematical model showing how changes in acquisition cost affect business profitability and growth sustainability.

The LTV:CAC ratio is calculated as: LTV:CAC = Customer Lifetime Value / Customer Acquisition Cost. This ratio indicates the return on investment for customer acquisition. A ratio of 3:1 means for every $1 spent acquiring a customer, the business generates $3 in lifetime value. The mathematical model for profitability is: Profit = (LTV - CAC) × Number of Customers. For sustainable growth: LTV > CAC, and ideally LTV ≥ 3×CAC. If LTV:CAC = 3:1, then for every $100 spent on acquisition, the business receives $300 in lifetime value, generating $200 profit per customer. If CAC increases by 25% while LTV remains constant, the new ratio becomes 2.4:1, reducing profitability and potentially threatening growth sustainability. The critical threshold is when LTV = CAC (ratio of 1:1), indicating break-even acquisition.

This problem demonstrates the fundamental relationship between acquisition cost and customer value. Students learn that CAC alone doesn't indicate business health; it must be evaluated relative to customer lifetime value. The ratio provides context for understanding whether acquisition investments are profitable and sustainable over time.

LTV: Customer Lifetime Value - total revenue from a customer over their lifetime

CAC: Customer Acquisition Cost - cost to acquire one customer

LTV:CAC Ratio: Efficiency metric comparing customer value to acquisition cost

• Maintain LTV:CAC ratio of 3:1 or higher

• LTV must exceed CAC for profitability

• Track ratio by customer cohort and channel

• Calculate LTV accurately for meaningful ratios

• Monitor changes in the ratio over time

• Optimize channels based on LTV:CAC ratios

• Focusing only on CAC without considering LTV

• Using inaccurate LTV calculations

• Ignoring the importance of the ratio

FAQ

Q: How often should I calculate and review my CAC?

A: CAC should be reviewed monthly at minimum, with weekly tracking for rapidly growing companies. The calculation period should match your marketing campaign cycles. For seasonal businesses, track CAC quarterly to account for fluctuations. Critical periods for review include: after launching new campaigns, when entering new markets, during product launches, and when experiencing changes in conversion rates. The key is to have enough data points for statistical significance while maintaining agility to adjust strategies. A common approach is to calculate CAC monthly, analyze trends quarterly, and make strategic adjustments annually. For accurate CAC calculation: CAC = (Total Marketing + Sales Expenses) / New Customers Acquired, where expenses should be attributed to the period when customers were acquired, not when spent.

Q: Is a high CAC always bad for a business?

A: No, a high CAC isn't always bad—it depends on the Customer Lifetime Value (LTV). The critical metric is the LTV:CAC ratio. For example, a SaaS company with a $500 CAC but $3,000 LTV has an excellent 6:1 ratio, making the high CAC worthwhile. High CAC may be justified when: targeting high-value customers, entering premium market segments, investing in brand building, or during market expansion phases. The formula to evaluate this is: Profit per Customer = LTV - CAC. If LTV significantly exceeds CAC (aim for 3:1 ratio), the high acquisition cost is sustainable. However, if CAC approaches or exceeds LTV, the business model is unsustainable. The mathematical threshold is when LTV = CAC, indicating break-even acquisition. Beyond this point, the business loses money on each acquisition.