Budget Planner Calculator

Personal finance management • 2026 budgeting tool

Budget Planning Formula:

Show CalculatorThe fundamental budget equation is: Net Income = Fixed Expenses + Variable Expenses + Savings + Debt Payments

Effective budgeting follows the 50/30/20 rule:

- 50% for needs (housing, utilities, groceries, transportation)

- 30% for wants (dining out, entertainment, hobbies)

- 20% for savings and debt repayment

This calculator helps you allocate your income across these categories based on your specific financial situation and goals.

Debt-to-Income Ratio: Total monthly debt payments ÷ Gross monthly income

Savings Rate: Monthly savings ÷ Gross monthly income × 100%

Emergency Fund: Recommended 3-6 months of essential expenses

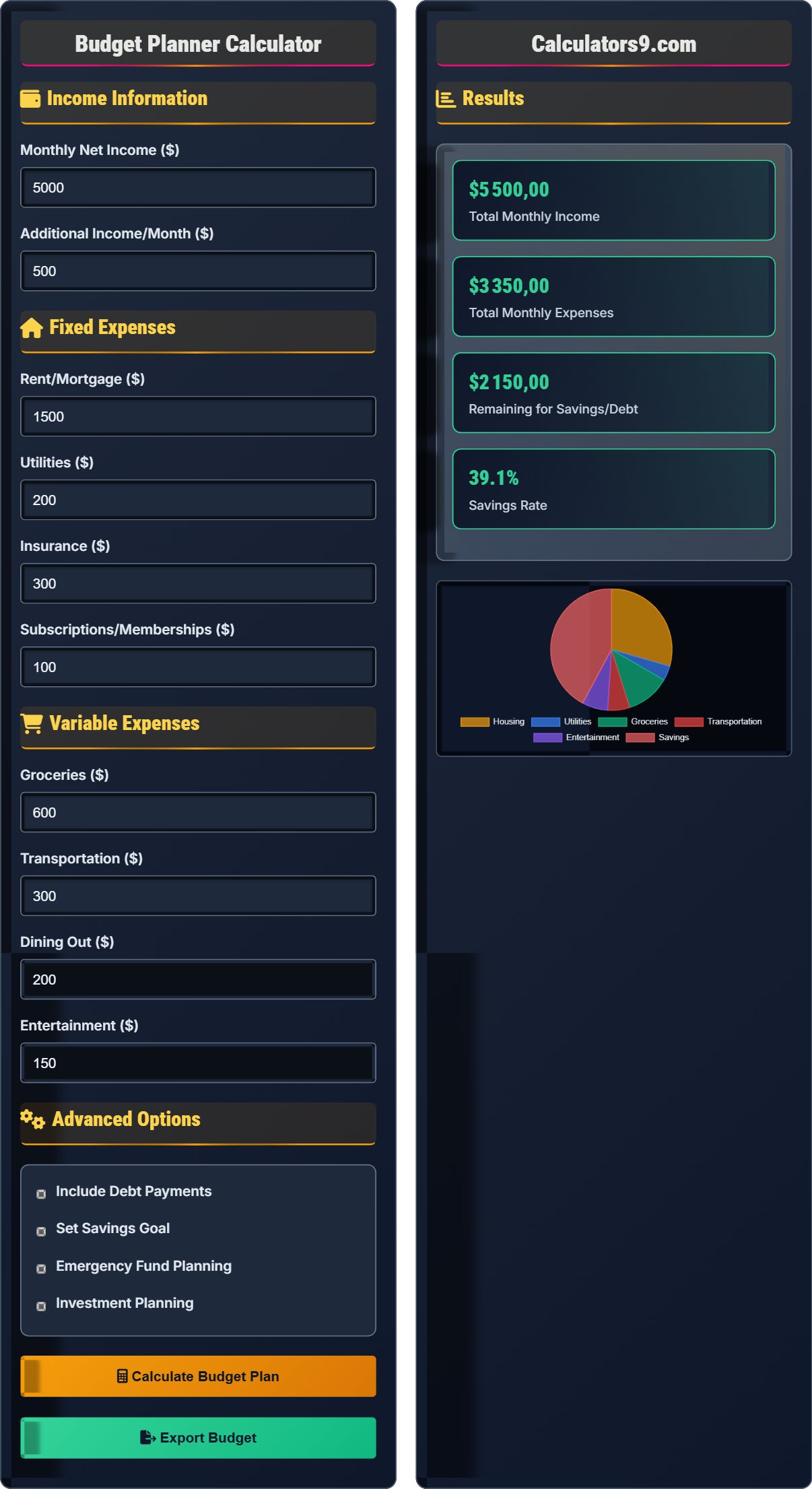

Income Information

Fixed Expenses

Variable Expenses

Advanced Options

Results

| Category | Amount ($) | % of Income | Status |

|---|---|---|---|

| Housing | $1,500.00 | 27.3% | Good |

| Utilities | $200.00 | 3.6% | Good |

| Groceries | $600.00 | 10.9% | Good |

| Transportation | $300.00 | 5.5% | Good |

| Entertainment | $350.00 | 6.4% | Good |

| Savings | $1,950.00 | 35.5% | Excellent |

| Item | Budgeted | Spent | Difference |

|---|---|---|---|

| Salary | $5,000.00 | $5,000.00 | $0.00 |

| Freelance | $500.00 | $450.00 | -$50.00 |

| Rent | $1,500.00 | $1,500.00 | $0.00 |

| Groceries | $600.00 | $580.00 | $20.00 |

| Utilities | $200.00 | $210.00 | -$10.00 |

| Savings | $1,950.00 | $1,950.00 | $0.00 |

Comprehensive Budget Planning Guide

The 50/30/20 rule is a simple budgeting technique popularized by Senator Elizabeth Warren. It divides your after-tax income into three main categories: 50% for needs (essential expenses), 30% for wants (non-essential spending), and 20% for savings and debt repayment. This method provides a balanced approach to managing your finances while ensuring you're building wealth and reducing debt.

The core budget equation is: Total Income = Fixed Expenses + Variable Expenses + Savings + Debt Payments

Where:

- Total Income: All monthly income sources after taxes

- Fixed Expenses: Consistent monthly bills (rent, insurance, subscriptions)

- Variable Expenses: Fluctuating costs (groceries, entertainment, transportation)

- Debt Payments: Credit cards, loans, mortgages

- Remaining Funds: Available for savings and investments

Key financial ratios help assess your financial health:

- Debt-to-Income Ratio: Total monthly debt payments ÷ gross monthly income (aim for under 36%)

- Savings Rate: Monthly savings ÷ gross monthly income (aim for 20% or more)

- Emergency Fund: Liquid savings ÷ monthly essential expenses (aim for 3-6 months)

- Housing Ratio: Housing costs ÷ gross monthly income (aim for under 28%)

- Automate savings: Set up automatic transfers to savings accounts

- Track spending: Use apps or spreadsheets to monitor expenses

- Review monthly: Adjust categories based on changing needs

- Pay yourself first: Prioritize savings before discretionary spending

- Use the envelope method: Allocate cash for variable expenses

Budget Basics

A plan for your money that ensures expenses don't exceed income while building financial security.

\( \text{Needs} = \text{Income} \times 0.5 \), \( \text{Wants} = \text{Income} \times 0.3 \), \( \text{Savings} = \text{Income} \times 0.2 \)

Where income is your after-tax monthly earnings.

- Track all income and expenses

- Review and adjust monthly

- Build emergency fund first

Financial Health

Metrics that measure your financial stability and progress toward goals.

- Calculate monthly ratios

- Compare to benchmarks

- Identify improvement areas

- Set targets for next month

- Savings rate: 20% or higher

- Debt-to-income: Below 36%

- Emergency fund: 3-6 months expenses

Budget Planning Learning Quiz

According to the 50/30/20 budget rule, what percentage of your after-tax income should be allocated to savings and debt repayment?

The answer is A) 20%. The 50/30/20 rule allocates 50% of after-tax income to needs (essential expenses), 30% to wants (discretionary spending), and 20% to savings and debt repayment. This allocation provides a balanced approach to financial management while ensuring you're building wealth and reducing debt. The 20% for savings and debt repayment includes emergency fund contributions, retirement savings, and any debt payments above minimums.

The 50/30/20 rule is a foundational budgeting principle that simplifies financial planning. The 20% allocation to savings and debt repayment is crucial for long-term financial security. This percentage ensures you're consistently building wealth while reducing liabilities. The rule works because it provides flexibility within a structured framework, allowing adjustments based on individual circumstances while maintaining focus on financial goals.

After-tax Income: Your total income minus all taxes and deductions

Needs: Essential expenses required for basic living (housing, utilities, food)

Wants: Discretionary spending for enjoyment and comfort

• 50% for needs (essential expenses)

• 30% for wants (discretionary spending)

• 20% for savings and debt repayment

• Start with the 20% savings portion first ("pay yourself first")

• Adjust percentages based on your financial situation

• Review and adjust monthly as needed

• Confusing gross income with net income

• Including wants in the needs category

• Not accounting for irregular income

If someone has a monthly after-tax income of $4,500, calculate the dollar amounts for each category using the 50/30/20 rule. Then determine if they can meet their goal of saving $1,000 per month.

Calculating 50/30/20 allocations:

Needs (50%): $4,500 × 0.50 = $2,250

Wants (30%): $4,500 × 0.30 = $1,350

Savings/Debt (20%): $4,500 × 0.20 = $900

Analysis: With a monthly after-tax income of $4,500, the 50/30/20 rule allocates $900 to savings and debt repayment. Since their goal is to save $1,000 per month, they fall short by $100. To meet their goal, they could either: 1) Increase their income, 2) Reduce their wants by $100 (from $1,350 to $1,250), or 3) Reduce their needs by $100 (which would require careful budgeting).

This calculation demonstrates how to apply the 50/30/20 rule to a specific income amount. The formula is straightforward: multiply the after-tax income by 0.50, 0.30, and 0.20 respectively. When personal goals conflict with the rule, it's important to evaluate trade-offs. In this case, increasing savings beyond the 20% guideline requires reducing another category, showing the importance of flexibility in budgeting.

After-tax Income: Income after all taxes and deductions

Budget Allocation: Distribution of income across spending categories

Trade-offs: When increasing one budget category requires decreasing another

• Always use after-tax income for calculations

• The sum of all categories must equal total income

• Adjust allocations based on individual goals and circumstances

• Use the formula: Category Amount = Income × Percentage

• Round to nearest $5 or $10 for easier tracking

• Review allocations quarterly to ensure they still fit your needs

• Using gross income instead of net income

• Forgetting to account for irregular expenses

• Not adjusting for life changes or financial goals

FAQ

Q: How do I handle irregular income when budgeting with the 50/30-20 rule?

A: Irregular income requires a modified approach to the 50/30/20 rule. Instead of applying percentages to variable monthly income, establish baseline budgets based on your lowest expected monthly income:

Base Budget Formula: Base Income = Average of lowest 3 months' income

Apply 50/30/20 to this base income to ensure your needs are covered even in low-income months. During high-income months, allocate surplus funds as follows:

- 50% to emergency fund (until 6-month buffer is reached)

- 30% to savings/investments

- 20% to debt repayment or special goals

For example, if your base income is $3,000 (50/30/20 = $1,500/$900/$600) but you earn $5,000 in a good month, the extra $2,000 should be directed to financial priorities rather than increasing wants. This approach provides stability while maximizing opportunities during high-income periods.

Q: My debt payments are so high that I can't follow the 50/30/20 rule. How should I adjust my budget?

A: When debt payments exceed the typical 20% allocation, you need a modified approach. The key is to prioritize debt elimination while maintaining essential needs:

High Debt Formula: Debt-to-Income Ratio = Total Monthly Debt Payments ÷ Gross Monthly Income

If your debt-to-income ratio exceeds 40%, consider the modified 40/30/30 rule:

- 40% for needs (including minimum debt payments)

- 30% for debt repayment beyond minimums

- 30% for wants and remaining savings

Alternatively, use the debt snowball or avalanche method: allocate extra funds to the highest interest debt while maintaining minimum payments on all debts. Once debt is reduced below 20% of income, revert to the traditional 50/30/20 rule. For example, with $5,000 income and $1,500 in debt payments (30%), you'd need to adjust to approximately 45/25/30 until debt is reduced.