Emergency Fund Calculator

Financial security planner • 2026 finance standards

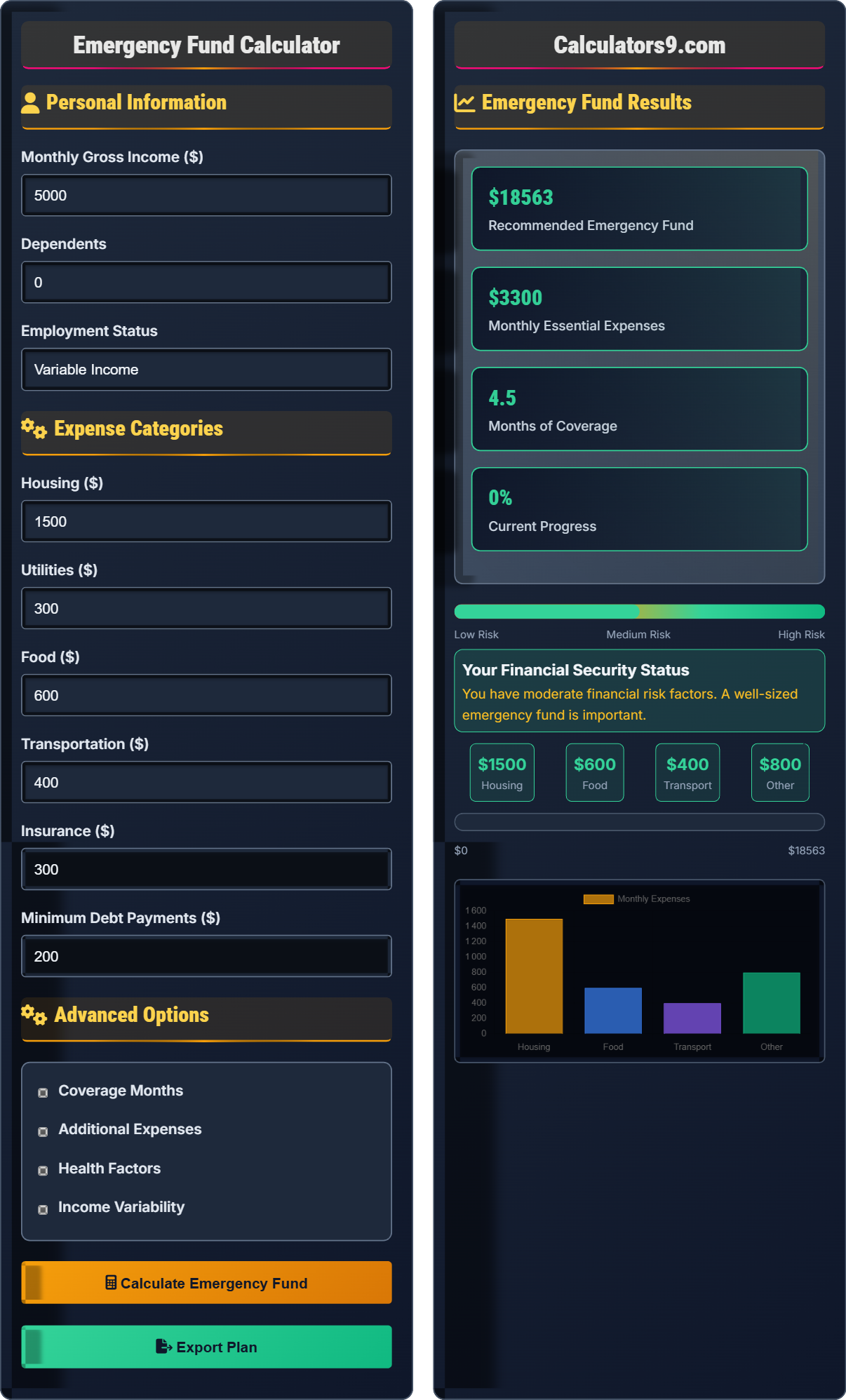

Emergency Fund Formula:

Show the calculator\( \text{Emergency Fund} = \text{Monthly Essential Expenses} \times \text{Months of Coverage} \)

Where:

- \( \text{Monthly Essential Expenses} \) = Housing, utilities, food, transportation, insurance, minimum debt payments

- \( \text{Months of Coverage} \) = 3-6 months (standard recommendation)

For families with dependents or unstable income, consider 6-12 months coverage.

Example: For monthly essential expenses of $3,000:

Conservative: $3,000 × 3 = $9,000

Moderate: $3,000 × 4.5 = $13,500

Aggressive: $3,000 × 6 = $18,000

Therefore, the emergency fund should range from $9,000 to $18,000 depending on risk tolerance.

Personal Information

Expense Categories

Advanced Options

Emergency Fund Results

Your Financial Security Status

Building your emergency fund will provide financial security during unexpected events.

| Category | Monthly | Annual | % of Total |

|---|

| Time Frame | Monthly Savings | Target Date |

|---|

Comprehensive Emergency Fund Guide

An emergency fund is a critical component of financial security. It provides a safety net for unexpected expenses like medical bills, job loss, car repairs, or home maintenance. Without this cushion, you might resort to high-interest debt, which can derail your financial goals and create long-term financial stress.

The standard formula for calculating your emergency fund:

Essential expenses include:

- Housing (rent/mortgage)

- Utilities (electricity, gas, water, internet)

- Food (groceries, basic necessities)

- Transportation (gas, public transit, car payments)

- Insurance (health, auto, life)

- Minimum debt payments

Best options for storing your emergency fund:

- High-Yield Savings: Easy access, modest interest

- Money Market Accounts: Higher yields with limited transactions

- Short-Term CDs: Fixed rates but penalties for early withdrawal

- Series I Bonds: Inflation protection but 1-year minimum

- Start Small: Begin with $1,000 if $3,000+ seems overwhelming

- Automate: Set up recurring transfers to build consistently

- Keep Separate: Don't mix with other savings goals

- Easy Access: Choose accounts with immediate availability

- Don't Touch: Reserve only for true emergencies

Emergency Fund Fundamentals

Cash reserve for unexpected expenses. 3-6 months of essential expenses. Financial security buffer.

\( \text{Fund} = \text{Monthly Essentials} \times \text{Months} \)

Adjust based on personal circumstances and risk factors.

- Only for true emergencies

- Keep liquid and accessible

- Rebuild after use

Building Strategies

Unexpected situations threatening financial stability. Job loss, medical bills, urgent repairs.

- Start with $1,000

- Automate monthly transfers

- Use windfalls (tax refund, bonus)

- Reduce non-essentials temporarily

- Build to full target

- Life circumstances matter

- Job stability affects target

- Family size impacts needs

- Health factors are important

Emergency Fund Learning Quiz

What is the primary purpose of an emergency fund?

The answer is B) To provide a financial safety net for unexpected expenses. An emergency fund is specifically designed to cover unforeseen situations like job loss, medical bills, car repairs, or home maintenance. It's not meant for planned expenses or investments. The fund provides peace of mind and prevents the need to rely on high-interest debt during difficult times.

Understanding the purpose of an emergency fund is fundamental to financial planning. The fund acts as a buffer between you and financial hardship. It's distinct from other savings goals because it's only for true emergencies. This concept is crucial for developing proper financial discipline and avoiding debt accumulation during unexpected events.

Emergency Fund: Cash set aside for unexpected expenses

Financial Safety Net: Protection against economic hardship

True Emergency: Unplanned event threatening financial stability

• Only use for genuine emergencies

• Keep separate from other savings

• Maintain even while pursuing other goals

• Think of it as insurance for your finances

• Set up automatic transfers to build consistently

• Keep in easily accessible account

• Using for planned expenses

• Investing the emergency fund

• Not rebuilding after use

Calculate the recommended emergency fund for someone with monthly essential expenses of $2,500 and 4.5 months coverage.

Step 1: Identify the formula

Emergency Fund = Monthly Essential Expenses × Months of Coverage

Step 2: Insert the values

Emergency Fund = $2,500 × 4.5

Step 3: Calculate the result

Emergency Fund = $11,250

Therefore, the recommended emergency fund is $11,250.

This calculation demonstrates the basic formula for determining emergency fund needs. The formula is straightforward but the key is accurately identifying essential expenses. These are expenses that must be paid to maintain basic living standards, not discretionary spending. The number of months (4.5) represents a moderate level of security, balancing preparedness with opportunity cost.

Essential Expenses: Necessary costs for basic living

Months of Coverage: Duration of financial security

Emergency Fund Target: Calculated savings goal

• Include only essential expenses

• Adjust months based on personal risk

• Recalculate periodically

• Track expenses for accurate calculation

• Review when life circumstances change

• Consider your job stability in planning

• Including non-essential expenses

• Using outdated expense figures

• Not accounting for personal risk factors

A family of four has monthly essential expenses of $4,000. They have two children, variable income, and moderate health concerns. What would be an appropriate emergency fund target, and how long would it take to build if they save $500 per month?

Step 1: Calculate base emergency fund

Base = $4,000 × 6 months = $24,000

Step 2: Adjust for risk factors

Risk factors: Dependents, variable income, health concerns

Adjusted = $24,000 × 1.25 = $30,000

Step 3: Calculate time to build

Time = $30,000 ÷ $500 per month = 60 months

Time = 5 years

The appropriate target is $30,000, which would take 5 years to build at $500 per month.

This problem shows how personal circumstances affect emergency fund targets. Families with dependents, variable income, or health concerns typically need larger emergency funds. The calculation demonstrates how multiple risk factors compound to increase the recommended amount. The time calculation shows the importance of starting early or increasing monthly contributions for larger targets.

Risk Factors: Circumstances requiring larger emergency funds

Time to Build: Duration needed to reach target

Monthly Contribution: Amount saved regularly

• Adjust for personal circumstances

• Consider multiple risk factors

• Plan for realistic timeframes

• Start with smaller target and increase gradually

• Use windfalls to accelerate building

• Consider higher contributions if possible

• Not accounting for personal risk factors

• Setting unrealistic timeframes

• Underestimating expenses with dependents

After building a $15,000 emergency fund, Sarah faces a $3,500 car repair bill. She has $12,000 in the fund. Should she use the emergency fund, and how should she rebuild it afterward?

Step 1: Assess if it's a true emergency

Yes, car repair is essential for transportation to work.

Step 2: Evaluate fund adequacy after use

After $3,500 withdrawal: $12,000 - $3,500 = $8,500 remaining

If monthly expenses are $3,000, this covers 2.8 months.

Step 3: Decision

Yes, use the fund. $8,500 still provides 2.8 months coverage.

Step 4: Rebuilding plan

To restore to $15,000: Need $6,500 more

At $500/month: 13 months to rebuild

Use the fund for the repair and commit to rebuilding it over 13 months.

This scenario illustrates proper emergency fund usage. The car repair qualifies as a true emergency since it's unexpected and essential for work. After the withdrawal, the fund still provides reasonable coverage (2.8 months). The key is having a plan to rebuild the fund after use, ensuring continued financial security. This demonstrates the cyclical nature of emergency fund management.

True Emergency: Unexpected event threatening financial stability

Rebuilding: Restoring fund after use

Financial Security: Adequate protection against hardship

• Use only for genuine emergencies

• Rebuild after any use

• Maintain adequate coverage

• Establish criteria for what constitutes an emergency

• Have a specific rebuilding plan ready

• Don't wait until fully rebuilt to use again if needed

• Using for planned expenses

• Not rebuilding after use

• Being too rigid about what's an emergency

Where is the best place to keep an emergency fund?

The answer is B) High-yield savings account. An emergency fund must be readily accessible when needed, so it should be kept in a liquid account. While stock market investments, real estate, and cryptocurrency can provide higher returns, they are subject to volatility and may not be accessible when you need them most. A high-yield savings account provides safety, liquidity, and modest interest earnings.

This question highlights the fundamental principle that emergency funds must prioritize accessibility and safety over returns. The fund needs to be available immediately when an emergency occurs, regardless of market conditions. This is why liquidity is more important than growth potential for emergency funds. The "opportunity cost" of not earning higher returns is worth the security of having guaranteed access to funds when needed.

Liquidity: How quickly assets can be converted to cash

Volatility: Fluctuation in value of investments

Accessibility: Ease of accessing funds when needed

• Prioritize safety over returns

• Ensure immediate access

• Avoid volatile investments

• Look for high-yield savings accounts for better returns

• Keep separate from other accounts to avoid temptation

• Ensure FDIC insurance coverage

• Investing emergency funds in volatile assets

• Keeping in hard-to-access accounts

• Mixing with other savings goals

FAQ

Q: How do I calculate my monthly essential expenses accurately?

A: Essential expenses are costs you must pay to maintain basic living standards:

\( \text{Essential Expenses} = \text{Housing} + \text{Utilities} + \text{Food} + \text{Transportation} + \text{Insurance} + \text{Minimum Debt Payments} \)

Exclude discretionary spending like entertainment, dining out, or luxury items. Track your expenses for 2-3 months to identify true essentials. The mathematical approach is to sum only necessary recurring costs that would remain if income stopped.

Q: Should I build an emergency fund while paying off debt?

A: The standard recommendation is to build a small emergency fund first:

- Start with $1,000-$2,000 emergency fund

- Pay minimum debt payments

- Focus on high-interest debt (credit cards)

- Build full emergency fund

- Accelerate debt payments

This prevents going further into debt if an emergency occurs while paying off existing debt. The mathematical principle is: Small emergency fund + debt payments < potential new debt from emergency.