Financial Independence Calculator

Reach FIRE fast • 2026 rates

Financial Independence Formula:

Show the calculator\( FI = \frac{Y}{r - g} \)

Where:

- \( FI \) = Financial Independence Amount

- \( Y \) = Annual Expenses

- \( r \) = Expected Return Rate (decimal form)

- \( g \) = Inflation Rate (decimal form)

This formula calculates the amount needed to achieve financial independence based on the 4% rule, adjusted for inflation and expected returns.

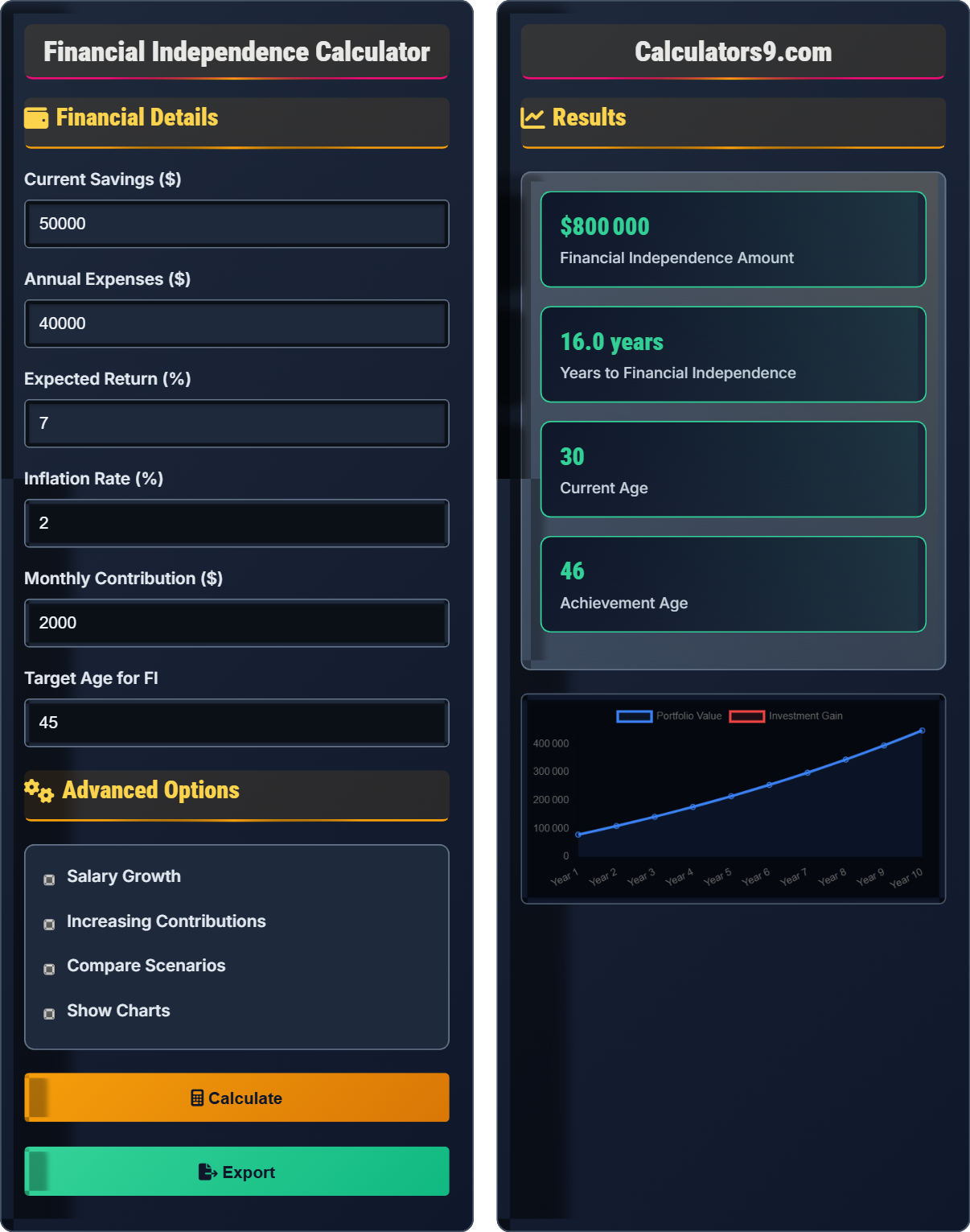

Example: For annual expenses of \( Y = \$40{,}000 \) at a return rate of 7% and inflation of 2%:

\( FI = \frac{40{,}000}{0.07 - 0.02} = \frac{40{,}000}{0.05} = \$800{,}000 \)

Thus, you would need approximately $800,000 to achieve financial independence.

Financial Details

Advanced Options

Results

| Year | Balance | Contributions | Investment Gain | Total Gain |

|---|

| Category | Amount | Percentage |

|---|

Comprehensive Financial Independence Guide

Financial independence (FI) is a state where an individual no longer needs to work to maintain their lifestyle. It's achieved when passive income from investments exceeds living expenses. The FIRE (Financial Independence, Retire Early) movement focuses on reaching this milestone as quickly as possible through aggressive saving, investing, and expense management.

The standard financial independence calculation uses the following formula:

Where:

- \(FI\) = Financial Independence Amount

- \(Y\) = Annual Expenses

- \(r\) = Expected Return Rate (decimal form)

- \(g\) = Inflation Rate (decimal form)

Reaching financial independence involves several key steps:

- Calculate your expenses: Track spending for at least 3 months to understand your true expenses

- Maximize savings rate: Aim for 50%+ savings rate by increasing income and reducing expenses

- Invest wisely: Focus on low-cost index funds with broad diversification

- Monitor progress: Regularly track net worth and investment growth

- Aggressive saving: Save 50-70% of income to accelerate FI timeline

- Side hustles: Increase income through part-time work or freelancing

- Expense optimization: Eliminate unnecessary expenses and negotiate bills

- Diversified portfolio: Invest in low-cost index funds across asset classes

- Automatic investments: Set up automatic transfers to investment accounts

Financial Independence Basics

State where passive income covers all expenses without needing employment.

\(FI = \frac{Y}{r-g}\)

Where FI=financial independence amount, Y=annual expenses, r=return rate, g=inflation rate.

- Save 25x annual expenses for basic FI

- Higher savings rate = faster FI

- Invest in diversified index funds

Strategies

Early contributions grow exponentially over time due to compound interest.

- Increase income

- Reduce expenses

- Maximize investment returns

- Start early

- Healthcare costs

- Tax implications

- Market volatility

- Inflation protection

Financial Independence Learning Quiz

What does achieving financial independence mean?

The answer is B) Passive income covering expenses. Financial independence is achieved when your passive income (from investments, rental properties, etc.) is sufficient to cover all your living expenses without needing to work for money.

Financial independence is fundamentally about creating sustainable income streams that match or exceed your expenses. It's not about having a specific dollar amount saved, but rather about the relationship between your expenses and your passive income. The goal is to build assets that generate enough income to support your desired lifestyle indefinitely.

Passive Income: Income received regularly with little or no effort required to produce it

Financial Independence: State where one's passive income exceeds expenses

Assets: Items that generate income or appreciate in value

• FI is about income vs. expenses, not a specific dollar amount

• Passive income continues regardless of work status

• Achieving FI provides freedom of choice

• Focus on building income-producing assets

• Track your actual expenses to determine FI number

• Remember: FI = Passive Income ≥ Expenses

• Confusing FI with having a certain amount saved

• Underestimating the importance of expense tracking

• Focusing on debt elimination without building income streams

Calculate the financial independence amount needed for someone with $50,000 annual expenses, expecting a 7% return rate and 2% inflation. Show your work.

Using the financial independence formula: \(FI = \frac{Y}{r-g}\)

Given:

- Y = $50,000

- r = 0.07 (7%)

- g = 0.02 (2%)

Step 1: Calculate r - g = 0.07 - 0.02 = 0.05

Step 2: Calculate FI = $50,000 ÷ 0.05 = $1,000,000

Therefore, this person would need $1,000,000 to achieve financial independence.

This calculation demonstrates the 4% rule concept in reverse. The 4% rule suggests that you can safely withdraw 4% of your investment portfolio annually without running out of money. By dividing annual expenses by the safe withdrawal rate (5% in this case: 7% return - 2% inflation), we find the required portfolio size.

Safe Withdrawal Rate: The percentage of portfolio you can withdraw annually without depleting it

4% Rule: Guideline suggesting 4% annual withdrawal is sustainable

Return Rate: Expected annual growth rate of investments

• Higher return rates reduce required FI amount

• Higher inflation increases required FI amount

• The formula accounts for inflation-adjusted withdrawals

• Remember: FI = Annual Expenses ÷ Safe Withdrawal Rate

• Common SWR ranges from 3-4%

• Conservative investors use lower SWR

• Forgetting to account for inflation in calculations

• Using unrealistic return expectations

• Not adjusting for market volatility

Alice earns $100,000 annually and spends $50,000. Bob earns $100,000 annually and spends $30,000. Both invest at 7% annually. Using the 4% rule, who will reach financial independence faster and by how much?

Step 1: Calculate Alice's FI target = $50,000 ÷ 0.04 = $1,250,000

Step 2: Calculate Bob's FI target = $30,000 ÷ 0.04 = $750,000

Step 3: Calculate savings rates: Alice saves $50,000/$100,000 = 50%

Bob saves $70,000/$100,000 = 70%

Step 4: Due to higher savings rate and lower target amount, Bob will reach FI significantly faster than Alice. The exact timing depends on compound growth, but Bob's combination of higher savings rate and lower target creates a substantial advantage.

This example demonstrates that both savings rate and target FI amount matter. While Alice and Bob earn the same amount, Bob's combination of lower expenses and higher savings rate gives him a dual advantage: a smaller target to reach and more money going toward that target each year. The power of compound interest means this advantage grows over time.

Savings Rate: Percentage of income saved after expenses

Compound Growth: Growth that builds upon previous growthFinancial Independence Target: Amount needed to achieve FI

• Higher savings rate accelerates FI timeline

• Lower expenses reduce FI target amount

• Both factors work together synergistically

• Focus on increasing savings rate through income or expense management

• Track spending to identify areas for reduction

• Automate savings to maintain consistent contributions

• Focusing only on increasing income without managing expenses

• Underestimating the impact of small expense reductions

• Not accounting for the multiplicative effect of savings rate and target amount

Jennifer has $100,000 invested and saves $10,000 annually. She's considering two investment strategies: Strategy A offers 5% average returns, Strategy B offers 8% average returns. Assuming she needs $800,000 for FI, how many years sooner could she reach FI with Strategy B compared to Strategy A?

Using the future value of a growing annuity formula: \(FV = PV(1+r)^n + PMT \times \frac{(1+r)^n - 1}{r}\)

Strategy A (5% returns):

Need to solve: $800,000 = $100,000(1.05)^n + $10,000 × [(1.05)^n - 1]/0.05

Strategy B (8% returns):

Need to solve: $800,000 = $100,000(1.08)^n + $10,000 × [(1.08)^n - 1]/0.08

Through iterative calculation:

Strategy A: Approximately 25 years

Strategy B: Approximately 18 years

Therefore, Strategy B would allow Jennifer to reach FI about 7 years sooner.

This demonstrates the exponential nature of compound growth. The 3 percentage point difference in returns becomes increasingly impactful over time. While the difference seems modest in the first few years, it compounds dramatically over decades, resulting in a substantial time advantage for the higher-return strategy.

Future Value: Value of an investment at a future date

Compounding: Process where returns generate their own returns

Growing Annuity: Series of payments that increase over time

• Higher returns accelerate FI timeline exponentially

• Time amplifies the impact of return differences

• Risk considerations must balance with return expectations

• Focus on low-cost, diversified index funds

• Minimize fees to maximize net returns

• Maintain long-term perspective despite market volatility

• Expecting high returns without accepting appropriate risk

• Overlooking the impact of fees on long-term returns

• Chasing performance without considering sustainability

Which of the following statements about FIRE strategies is TRUE?

The answer is C) Coast FIRE allows early investment cessation. Coast FIRE is a strategy where you invest aggressively for a period until your investments grow enough to reach financial independence by a traditional retirement age without further contributions. The other options are incorrect: Lean FIRE typically requires very high savings rates (70%+), Fat FIRE often requires higher savings rates than normal FIRE, and normal FIRE follows the 25x rule, not 50x.

Coast FIRE is a unique strategy that leverages the power of compound interest over long time horizons. By investing heavily early in life, the resulting growth can continue to compound for decades, eventually reaching the FI target without additional contributions. This strategy requires significant early sacrifice but offers maximum flexibility later in life.

Lean FIRE: Minimalist approach with very low expenses

Fat FIRE: Comfortable retirement with higher expenses

Coast FIRE: Early investment followed by no contributions

• Different FIRE approaches suit different lifestyles

• All require significant savings rates

• Time and compound interest are key factors

• Choose FIRE strategy that matches your lifestyle preferences

• Consider healthcare costs in your FI planning

• Factor in geographic differences in cost of living

• Assuming all FIRE approaches have similar requirements

• Not accounting for healthcare costs before Medicare eligibility

• Underestimating the psychological challenges of early retirement

FAQ

Q: How do I calculate my financial independence number?

A: Your financial independence number is typically calculated using the 4% rule. Multiply your annual expenses by 25 to get your target:

\( FI = Annual\ Expenses \times 25 \)

For example, if your annual expenses are \( \$40{,}000 \), your financial independence target would be \( \$40{,}000 \times 25 = \$1{,}000{,}000 \).

This assumes you can safely withdraw 4% of your portfolio annually without depleting it over a 30+ year period. Adjust the multiplier based on your expected return rate and inflation assumptions.

Q: How much should I save monthly to reach FI in 10 years?

A: The required monthly savings depends on your target FI amount and expected investment returns.

Using the future value formula: \( FV = PMT \times \frac{(1+r)^n - 1}{r} \)

If your FI target is \( \$800{,}000 \), starting with \( \$50{,}000 \) in savings, and expecting 7% annual returns:

\( 800{,}000 = 50{,}000(1.07)^{10} + PMT \times \frac{(1.07)^{10} - 1}{0.07} \)

After calculations: \( PMT \approx \$4{,}800 \) per month

This represents a savings rate of approximately 65-70% of gross income, which is quite aggressive but achievable with high income or significant expense reduction.