Inflation Adjustment Calculator

Financial planning tool • 2026 finance standards

Inflation Adjustment Formula:

Show the calculator\( \text{Future Value} = \text{Present Value} \times (1 + r)^n \)

\( \text{Purchasing Power} = \frac{\text{Present Value}}{(1 + r)^n} \)

Where:

- \( \text{Present Value} \) = Current amount of money

- \( r \) = Annual inflation rate (as decimal)

- \( n \) = Number of years

These formulas calculate the impact of inflation on money over time.

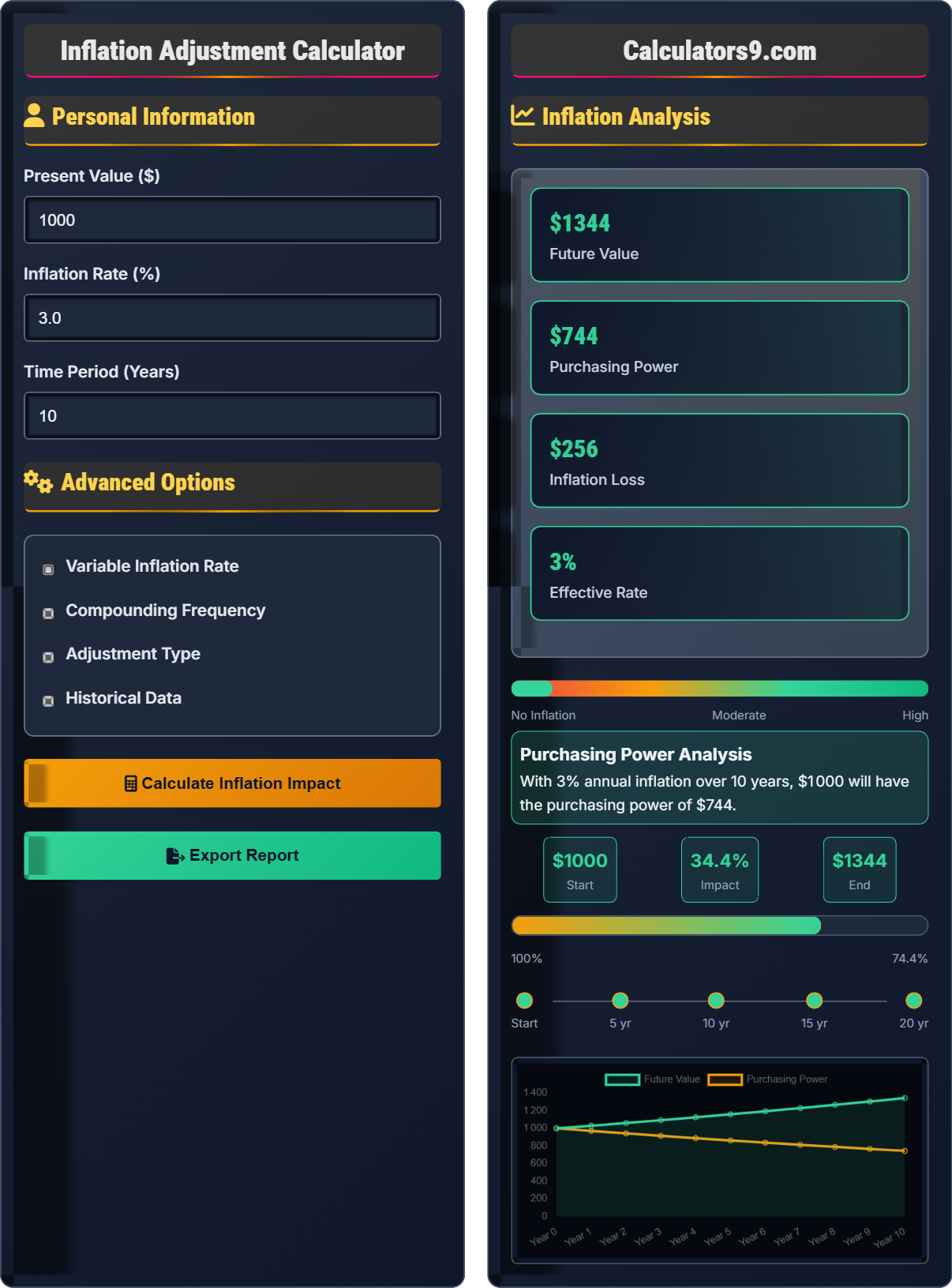

Example: $100 today with 3% annual inflation over 10 years:

Future Value = $100 × (1.03)^10 = $100 × 1.344 = $134.40

Purchasing Power = $100 ÷ (1.03)^10 = $100 ÷ 1.344 = $74.41

Therefore, $100 today will have the purchasing power of $74.41 in 10 years.

Personal Information

Advanced Options

Inflation Analysis

Purchasing Power Analysis

With 3% annual inflation over 10 years, $1,000 will have the purchasing power of $744.

| Metric | Value | Change | Impact |

|---|

| Year | Future Value | Purchasing Power | Cumulative Inflation |

|---|

Comprehensive Inflation Guide

Inflation is the rate at which the general level of prices for goods and services rises, leading to a decline in purchasing power. As inflation increases, each unit of currency buys fewer goods and services. Understanding inflation is crucial for financial planning as it affects the real value of money over time.

The compound inflation formula:

Where:

- Present Value: Current amount of money

- r: Annual inflation rate (as decimal)

- n: Number of years

Historical U.S. inflation rates:

- 1950-2020 Average: ~3.2%

- 1970s (High): ~7.1%

- 1980s-2010s: ~2.5%

- 2020-2022 (Recent): ~4.5%

- Target Rate: ~2% (Federal Reserve)

- Invest in Stocks: Historically outpace inflation

- Treasury Inflation-Protected Securities (TIPS): Indexed to inflation

- Real Estate: Appreciates with inflation

- Commodities: Hedge against currency devaluation

- Income Growth: Pursue raises and promotions

Inflation Fundamentals

Rise in general price levels. Reduces purchasing power of money. Measured as percentage increase.

\( \text{Future Value} = \text{Present Value} \times (1 + r)^n \)

Compound interest formula applied to price increases.

- Higher rates compound faster

- Longer periods magnify impact

- Even low rates matter over time

Protection Strategies

Amount of goods/services money can buy. Inflation reduces this over time.

- Invest in growth assets

- Consider inflation-protected securities

- Focus on income growth

- Review spending regularly

- Plan for long-term costs

- Historical rates may not predict future

- Regional variations exist

- Personal inflation rate varies

- Deflation is also possible

Inflation Learning Quiz

What is inflation?

The answer is D) Both B and C. Inflation is defined as an increase in the general price level of goods and services over time. This increase in prices leads to a decrease in the purchasing power of money. So both definitions are correct - inflation is both a rise in prices AND a decrease in purchasing power.

Inflation is fundamentally about the relationship between money and goods. When prices rise (inflation), each unit of currency buys fewer goods and services. This dual nature of inflation - affecting both price levels and purchasing power - is essential to understand for financial planning. The mathematical relationship shows how the same amount of money will buy less over time.

Inflation: Rise in general price levels over time

Purchasing Power: Quantity of goods/services money can buy

Price Level: Average of current prices across economy

• Inflation reduces purchasing power

• Affects all goods and services

• Measured as percentage change

• Remember: Rising prices = Falling purchasing power

• Inflation affects everything equally

• Compounding makes impact exponential

• Confusing inflation with deflation

• Not accounting for compounding effect

• Assuming inflation rate is constant

Calculate the future value of $1,000 after 5 years with 4% annual inflation.

Step 1: Identify the formula

Future Value = Present Value × (1 + r)^n

Step 2: Insert the values

Future Value = $1,000 × (1 + 0.04)^5

Future Value = $1,000 × (1.04)^5

Step 3: Calculate the exponent

(1.04)^5 = 1.21665

Step 4: Calculate the result

Future Value = $1,000 × 1.21665 = $1,216.65

Therefore, $1,000 will have the future value of $1,216.65 after 5 years with 4% inflation.

This calculation demonstrates the compound effect of inflation. Each year, the price level increases by 4%, and the next year's increase is applied to the already higher level. This compounding creates exponential growth in the required amount to maintain the same purchasing power. After 5 years, the original $1,000 would need $1,216.65 to buy the same goods.

Future Value: Amount needed in the future to maintain purchasing power

Compounding: Exponential growth from repeated increases

Purchasing Power: Goods/services a dollar can buy

• Convert percentage to decimal (4% = 0.04)

• Apply exponent to the entire factor (1+r)

• Future value is always higher than present value

• Use a calculator for exponents

• Double-check decimal conversion

• Remember this is what you need, not what you'll have

• Forgetting to convert percentage to decimal

• Adding instead of multiplying by the factor

• Misunderstanding what the result represents

If $100 today can buy a certain basket of goods, how much will that same basket cost in 10 years if inflation averages 3% annually?

Step 1: Identify the formula for future cost

Future Cost = Present Cost × (1 + r)^n

Step 2: Insert the values

Future Cost = $100 × (1 + 0.03)^10

Future Cost = $100 × (1.03)^10

Step 3: Calculate the exponent

(1.03)^10 = 1.34392

Step 4: Calculate the result

Future Cost = $100 × 1.34392 = $134.39

The same basket of goods will cost $134.39 in 10 years with 3% annual inflation.

This problem illustrates how inflation reduces the purchasing power of money. The same $100 that buys the basket today will only buy about 74% of the same basket in 10 years (100/134.39). This demonstrates why investors seek returns that exceed inflation to maintain or grow purchasing power over time.

Basket of Goods: Representative sample of consumer items

Purchasing Power: Amount of goods money can buy

Consumer Price Index: Measures changes in basket prices

• Higher inflation = Higher future costs

• Longer periods = Greater impact

• Compounding accelerates the effect

• Think in terms of what things will cost

• Consider this for long-term planning

• Plan for higher future expenses

• Confusing cost increase with purchasing power decrease

• Underestimating compound effect

• Not adjusting for inflation in planning

John earns $50,000 annually. If inflation averages 3.5% over 5 years, what salary would he need to maintain the same purchasing power? If he receives a 3% annual raise, what will his real purchasing power be relative to today?

Part 1: Calculate salary needed to maintain purchasing power

Required Salary = $50,000 × (1.035)^5

Required Salary = $50,000 × 1.1877 = $59,385

Part 2: Calculate John's salary with 3% annual raises

Future Salary = $50,000 × (1.03)^5

Future Salary = $50,000 × 1.1593 = $57,965

Part 3: Calculate purchasing power relative to today

Purchasing Power = $57,965 ÷ $59,385 = 0.976 or 97.6%

John would need $59,385 to maintain purchasing power, but with 3% raises he'll earn $57,965, giving him 97.6% of today's purchasing power.

This problem demonstrates the importance of salary growth keeping pace with inflation. Even with raises, if they don't match inflation, purchasing power decreases. John's 3% raises fall short of the 3.5% inflation, resulting in a 2.4% decrease in purchasing power. This shows why "keeping up with inflation" is crucial for maintaining living standards.

Real Salary: Salary adjusted for inflation

Nominal Salary: Salary in current dollars

Purchasing Power: Effective buying capacity

• Salary raises must exceed inflation to gain

• Equal to inflation = Maintains status quo

• Below inflation = Losing ground

• Negotiate raises above inflation rate

• Consider inflation when evaluating offers

• Plan career growth to stay ahead

• Accepting raises below inflation

• Not considering inflation in negotiations

• Assuming any raise is good

Which of the following best describes the long-term impact of 2% annual inflation over 20 years?

The answer is B) Money loses about 33% of its purchasing power. Using the formula:

Future Value = Present Value × (1 + r)^n

Future Value = $100 × (1.02)^20 = $100 × 1.4859 = $148.59

Purchasing Power = $100 ÷ $148.59 = 0.673 or 67% of original

Loss = 100% - 67% = 33%

After 20 years of 2% inflation, money retains only 67% of its original purchasing power.

This example shows how even low inflation rates have significant long-term effects. A seemingly modest 2% annual inflation compounds to a 33% loss in purchasing power over 20 years. This demonstrates why long-term financial planning must account for inflation, even when rates appear low. The effect is exponential due to compounding.

Compounding Effect: Exponential impact of repeated increases

Long-term Impact: Cumulative effect over many years

Purchasing Power Decay: Gradual reduction over time

• Even low rates matter over long periods

• Effects are exponential, not linear

• 20-year horizon shows significant impact

• Use 72 rule: 72 ÷ inflation rate ≈ doubling time

• Plan for inflation in long-term goals

• Consider this for retirement planning

• Underestimating long-term effects

• Thinking low inflation is negligible

• Not planning for inflation in retirement

FAQ

Q: How do I calculate the real value of my money after inflation?

A: The formula to calculate purchasing power after inflation is:

\( \text{Purchasing Power} = \frac{\text{Present Value}}{(1 + r)^n} \)

Where r is the inflation rate and n is the number of years. For example, with $1,000, 3% inflation, and 10 years:

Purchasing Power = $1,000 ÷ (1.03)^10 = $1,000 ÷ 1.344 = $744

This means your $1,000 will have the buying power of only $744 in today's dollars after 10 years.

Q: How does inflation affect my retirement planning?

A: Inflation significantly impacts retirement planning. If you need $50,000 annually today and expect 3% inflation over 20 years until retirement:

\( \text{Future Need} = \$50,000 \times (1.03)^{20} = \$50,000 \times 1.806 = \$90,300 \)

You'll need $90,300 in 20 years to maintain the same lifestyle that $50,000 provides today. This is why retirement planning must account for inflation-adjusted income needs.