Savings Goal Calculator

Financial goal planner • 2026 finance standards

Savings Goal Formula:

Show the calculator\( \text{Future Value} = \text{PV} \times (1 + r)^n + \text{PMT} \times \frac{(1 + r)^n - 1}{r} \)

Where:

- \( \text{PV} \) = Present value (current savings)

- \( \text{PMT} \) = Periodic payment (monthly contribution)

- \( r \) = Periodic interest rate (annual rate ÷ 12)

- \( n \) = Number of periods (months)

This formula calculates the future value of a savings account with regular contributions and compound interest.

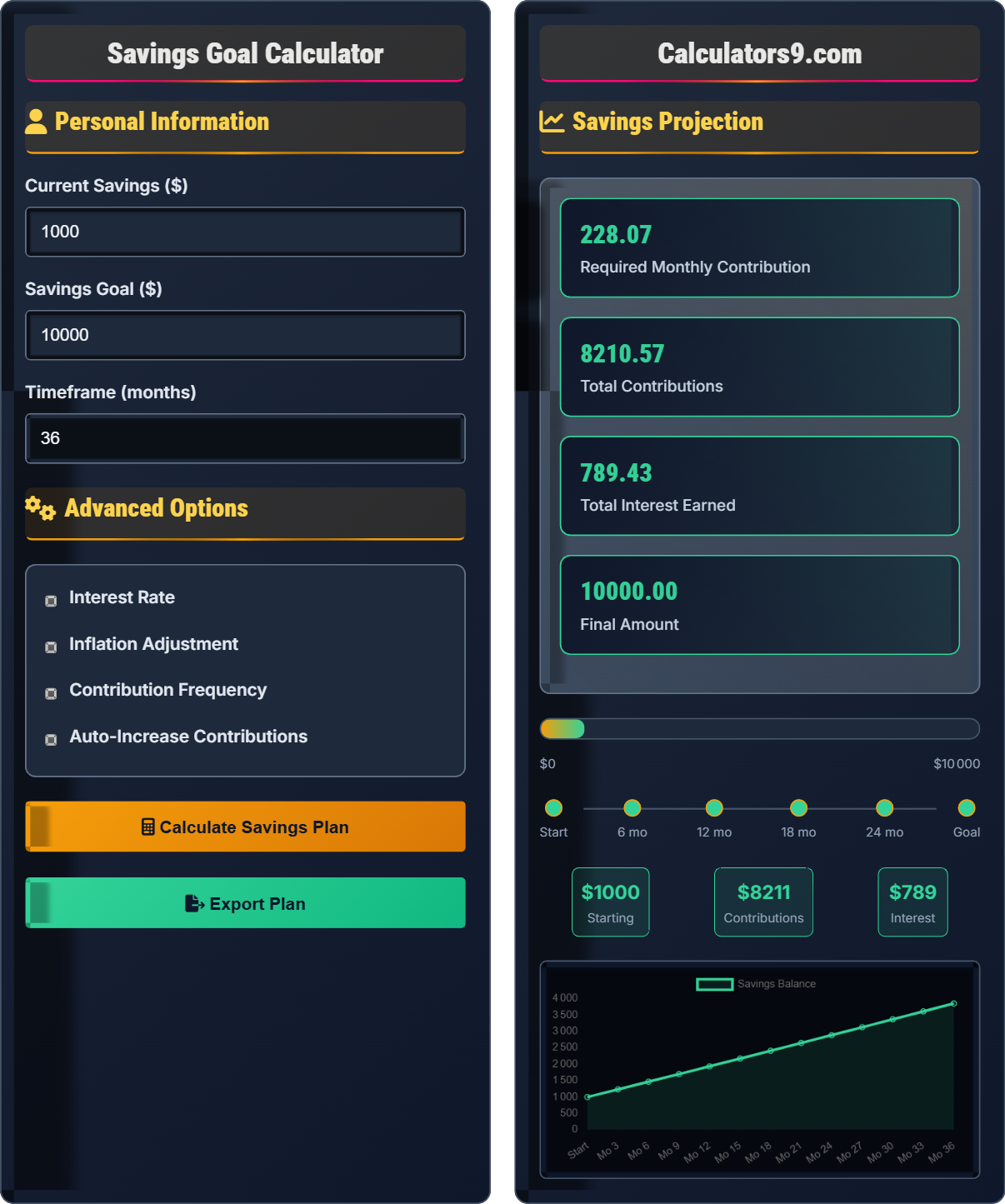

Example: Saving $10,000 goal with $1,000 current savings, $200 monthly contributions, 5% annual interest:

Monthly rate: \( r = 0.05 ÷ 12 = 0.004167 \)

For 36 months: \( \text{FV} = 1000 \times (1.004167)^{36} + 200 \times \frac{(1.004167)^{36} - 1}{0.004167} \)

\( \text{FV} = 1000 \times 1.1616 + 200 \times \frac{0.1616}{0.004167} = 1161.60 + 200 \times 38.78 = \$8,917.60 \)

After 36 months, you'll have approximately $8,917.60 saved.

Personal Information

Advanced Options

Savings Projection

| Period | Contribution | Interest | Balance |

|---|

| Month | Date | Amount | Running Total |

|---|

Comprehensive Savings Guide

Compound interest is the interest earned on both your principal and the accumulated interest. Albert Einstein allegedly called it the "eighth wonder of the world." The earlier you start saving, the more time compound interest has to work in your favor, creating exponential growth in your savings over time.

The formula for compound interest:

Where:

- A: Final amount

- P: Principal (initial investment)

- r: Annual interest rate (decimal)

- n: Number of times interest is compounded per year

- t: Time in years

Common savings vehicles and their characteristics:

- High-Yield Savings: Higher interest rates than traditional savings

- Certificates of Deposit (CDs): Fixed interest rates for set terms

- Money Market Accounts: Higher yields with limited transactions

- Government Bonds: Safe investments with moderate returns

- Stock Market Investments: Higher potential returns with more risk

- Pay Yourself First: Treat savings as a non-negotiable expense

- Round-Up Method: Automatically round purchases to the nearest dollar

- 52-Week Challenge: Save increasingly larger amounts each week

- Emergency Fund: Maintain 3-6 months of expenses

- Automate Transfers: Set up recurring transfers to savings

Savings Fundamentals

Interest earned on both principal and accumulated interest. The foundation of long-term wealth building.

\( \text{Future Value} = \text{Present Value} \times (1 + r)^n \)

Money grows over time with compound interest.

- Start saving early for maximum benefit

- Consistency beats timing

- Automate your savings

Planning Tips

3-6 months of expenses for unexpected events. Foundation of financial security.

- Specific savings target

- Measurable amount

- Achievable contribution

- Relevant to your needs

- Time-bound deadline

- Account for inflation

- Choose appropriate risk level

- Consider tax implications

- Review and adjust regularly

Finance Learning Quiz

What does the "power of compound interest" refer to?

The answer is B) Interest earned on both principal and accumulated interest. Compound interest means you earn interest not only on your initial investment (principal) but also on the interest that has already been added to your account. This creates exponential growth over time, as your money earns interest on interest, leading to accelerated growth in your savings.

Compound interest is one of the most powerful concepts in finance. Unlike simple interest, which is calculated only on the original principal, compound interest builds on itself. In the formula A = P(1 + r/n)^(nt), the exponent (nt) demonstrates how time amplifies the effect of compounding. This is why starting to save early has such a dramatic impact on long-term wealth accumulation.

Principal: The initial amount of money invested or saved

Compounding: The process of earning interest on interest

Exponential Growth: Growth that accelerates over time

• Interest is earned on previously earned interest

• The longer the time period, the greater the effect

• Frequency of compounding matters

• Start saving as early as possible

• Look for accounts with higher compounding frequency

• Reinvest dividends and interest

• Confusing compound interest with simple interest

• Underestimating the impact of time

• Not reinvesting earnings

Calculate the future value of $1,000 invested at 6% annual interest compounded monthly for 5 years.

Step 1: Identify the variables

P = $1,000 (principal)

r = 6% = 0.06 (annual interest rate)

n = 12 (compounded monthly)

t = 5 (years)

Step 2: Apply the compound interest formula

A = P(1 + r/n)^(nt)

A = 1000(1 + 0.06/12)^(12×5)

A = 1000(1 + 0.005)^60

A = 1000(1.005)^60

A = 1000 × 1.34885

A = $1,348.85

Therefore, the investment will grow to $1,348.85 after 5 years.

This calculation demonstrates the power of compound interest over time. The initial $1,000 grew to $1,348.85, earning $348.85 in interest over 5 years. Note that with simple interest, the same investment would only earn $300 ($1,000 × 0.06 × 5). The extra $48.85 comes from compounding - interest earned on previous interest.

Future Value: The value of an investment at a future date

Compounding Frequency: How often interest is calculated and added

Interest Rate: Percentage earned on the investment

• Adjust interest rate for compounding frequency

• Use the correct number of periods

• Convert percentage to decimal

• Convert annual rate to periodic rate

• Calculate total periods correctly

• Use parentheses to maintain order of operations

• Forgetting to adjust interest rate for compounding frequency

• Miscounting the number of periods

• Not converting percentage to decimal

Sarah wants to save $15,000 for a down payment in 3 years. She currently has $2,000 saved and expects to earn 4% annual interest. How much should she save monthly to reach her goal?

Step 1: Identify known values

FV = $15,000 (future value needed)

PV = $2,000 (present value/current savings)

r = 4% annually = 0.04/12 = 0.003333 monthly

n = 3 years × 12 months = 36 months

Step 2: Use the future value of annuity formula rearranged to solve for PMT

FV = PV(1+r)^n + PMT × [((1+r)^n - 1)/r]

15000 = 2000(1.003333)^36 + PMT × [((1.003333)^36 - 1)/0.003333]

15000 = 2000 × 1.1273 + PMT × [0.1273/0.003333]

15000 = 2254.60 + PMT × 38.19

15000 - 2254.60 = PMT × 38.19

12745.40 = PMT × 38.19

PMT = 12745.40 / 38.19 = $333.74

Sarah needs to save approximately $333.74 per month to reach her goal.

This problem combines both present value and future value of annuity calculations. Sarah's current savings will grow with compound interest, but she also needs to make regular contributions. The calculation shows how both components work together to reach the target. The monthly contribution of $333.74 will accumulate to about $12,014.64 in contributions plus interest, combined with the growth of her initial $2,000 to $2,254.60.

Present Value: Current worth of future sum

Future Value: Value of investment at future date

Annuity: Series of equal payments at regular intervals

• Account for both current savings and future contributions

• Convert annual rates to periodic rates

• Calculate total number of periods correctly

• Separate current savings from future contributions

• Use financial calculator or spreadsheet for complex calculations

• Round up monthly contributions to be conservative

• Forgetting to account for current savings

• Not adjusting for compounding frequency

• Incorrectly calculating the number of periods

Compare two savers: Alex starts saving $200/month at age 25 for 10 years, then stops. Jamie starts saving $200/month at age 35 for 30 years. Both earn 7% annually. Who has more money at age 65?

Step 1: Calculate Alex's savings

Phase 1: 10 years of contributions (age 25-35)

PMT = $200, r = 0.07/12, n = 120 months

FV after 10 years = $200 × [((1.005833)^120 - 1)/0.005833] = $34,848.96

Phase 2: 30 years of compound growth (age 35-65)

PV = $34,848.96, r = 0.07/12, n = 360 months

FV at age 65 = $34,848.96 × (1.005833)^360 = $34,848.96 × 8.1235 = $283,087.34

Step 2: Calculate Jamie's savings

30 years of contributions (age 35-65)

PMT = $200, r = 0.07/12, n = 360 months

FV = $200 × [((1.005833)^360 - 1)/0.005833] = $200 × 1,219.97 = $243,994.00

Alex has $283,087.34 while Jamie has $243,994.00. Alex wins despite saving for only 10 years!

This classic example demonstrates the incredible power of starting early. Alex contributed only $24,000 total ($200 × 120 months) but ended with $283,087 due to 30 years of compound growth. Jamie contributed $72,000 total ($200 × 360 months) but only had 30 years of growth for each contribution. The early years of compounding make the biggest difference in long-term wealth accumulation.

Time Value of Money: Money available now is worth more than same amount later

Compounding Effect: Exponential growth from interest on interest

Early Advantage: Greater benefit from starting young

• Time is more valuable than money in investing

• Even small amounts early have huge impact

• Compounding accelerates over time

• Start saving immediately, even if small amounts

• Take advantage of employer matching

• Automate savings to maintain consistency

• Believing you can start saving later

• Underestimating the impact of time

• Delaying investments for "better" opportunities

How does inflation affect your savings goal?

The answer is B) It reduces the purchasing power of your future savings. Inflation is the rate at which prices for goods and services rise over time. If you save $10,000 today but inflation averages 3% annually for 20 years, that same $10,000 will have the purchasing power of only about $5,537 in today's dollars. This means you'll need to save more to maintain the same purchasing power in the future.

Inflation erodes the value of money over time. The real return on your savings is the nominal return minus inflation. If your savings account earns 2% annually but inflation is 3%, your real purchasing power is actually decreasing by 1% annually. This is why it's important to consider inflation when setting long-term savings goals and to choose investments that can outpace inflation.

Inflation: Increase in price level of goods and services

Purchasing Power: Amount of goods/services money can buy

Real Return: Nominal return adjusted for inflation

• Inflation reduces future purchasing power

• Real return = Nominal return - Inflation

• Consider inflation in long-term planning

• Factor inflation into long-term goals

• Choose investments that outpace inflation

• Consider Treasury Inflation-Protected Securities (TIPS)

• Ignoring inflation in savings calculations

• Assuming current prices will remain the same

• Not adjusting goals for purchasing power

FAQ

Q: How much should I save for an emergency fund?

A: The standard recommendation is 3-6 months of essential expenses. Calculate this as:

\( \text{Emergency Fund} = \text{Monthly Essential Expenses} \times 3-6 \)

Essential expenses include housing, utilities, food, transportation, insurance, and minimum debt payments. For example, if your essential monthly expenses are $3,000:

- Conservative approach: $3,000 × 6 = $18,000

- Moderate approach: $3,000 × 4.5 = $13,500

- Aggressive approach: $3,000 × 3 = $9,000

The appropriate amount depends on job stability, family situation, and health considerations.

Q: Should I prioritize paying off debt or saving?

A: The decision depends on interest rates and tax implications:

Mathematical approach:

If Debt Interest Rate > Investment Return Potential → Pay debt first

If Investment Return Potential > Debt Interest Rate → Invest first

However, consider these priorities:

- Build minimal emergency fund ($1,000-$2,000)

- Maximize employer 401(k) match

- Pay high-interest debt (credit cards, >8%)

- Continue emergency fund to 3-6 months

- Save for other goals

- Pay medium-interest debt (4-8%)