Debt-to-Income Ratio Calculator

Fast DTI calculator • 2026 rates

DTI Ratio Formula:

Show the calculator\( \text{DTI Ratio} = \frac{\text{Total Monthly Debt Payments}}{\text{Gross Monthly Income}} \times 100\% \)

For DTI calculation:

- Total Monthly Debt: Includes mortgage, credit cards, auto loans, student loans, etc.

- Gross Monthly Income: Pre-tax income from all sources

- Front-End DTI: Housing costs ÷ Gross monthly income

- Back-End DTI: All debts ÷ Gross monthly income

This formula calculates the percentage of gross income used for debt payments.

Example: For $4,000 monthly income with $1,200 in debt payments:

DTI Ratio: \( \frac{1{,}200}{4{,}000} \times 100\% = 30\% \)

Thus, the borrower has a 30% DTI ratio.

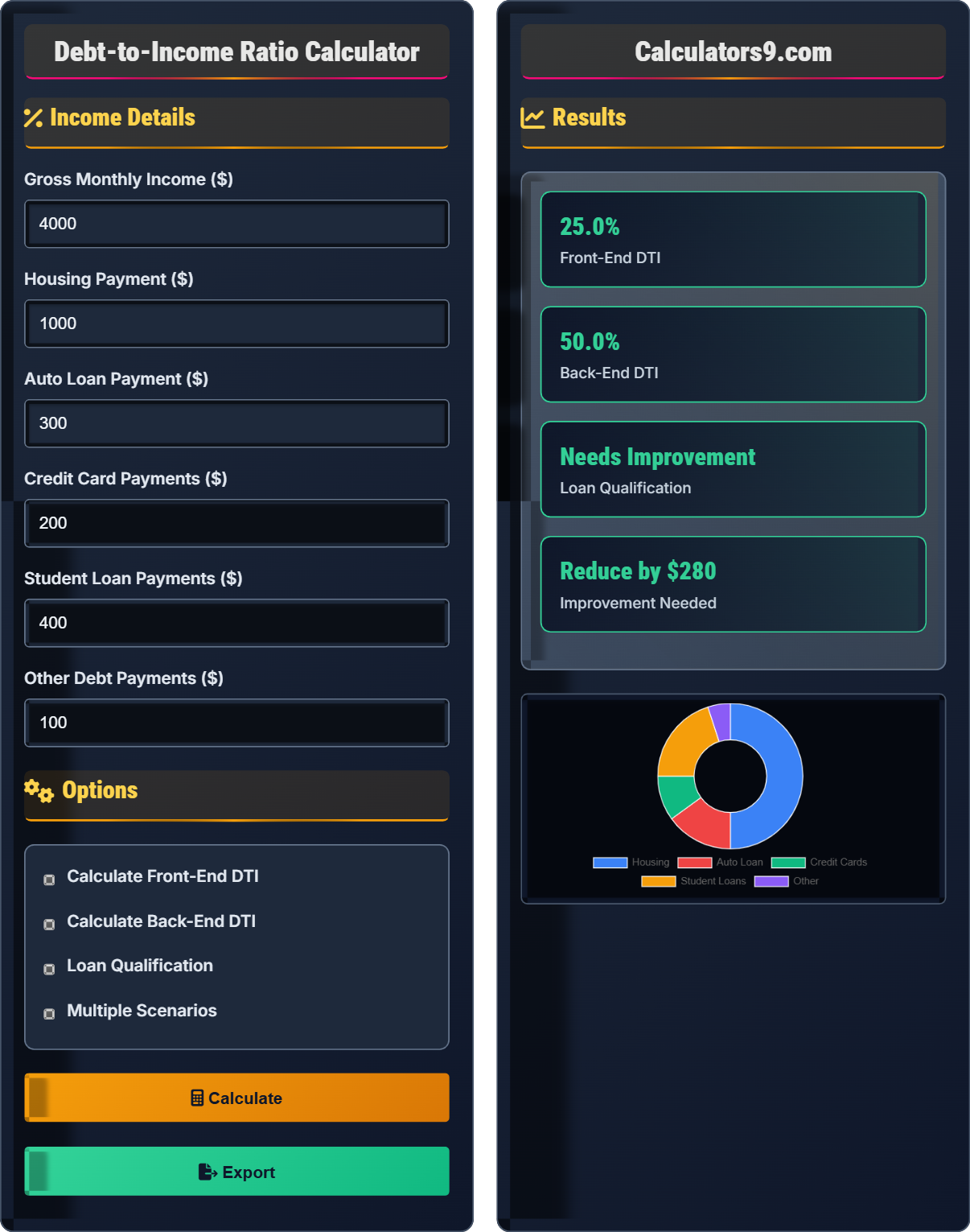

Income Details

Options

Results

| Debt Type | Monthly Payment | Percentage of Income |

|---|

Front-End DTI: 25.0%

Back-End DTI: 50.0%

Recommended Maximum: 43.0%

Acceptable Range: 36-43%

Loan Type: Conventional

Qualification: Conditional

Required Action: Reduce debt by $200/month

Comprehensive DTI Guide

The debt-to-income (DTI) ratio is a financial metric that compares your monthly debt payments to your gross monthly income. Lenders use this ratio to assess your ability to manage monthly payments and repay debts. A lower DTI ratio indicates better financial health and improves your chances of loan approval.

The standard DTI calculation uses the following formula:

Where:

- \( \text{DTI} \) = Debt-to-income ratio as a percentage

- \( \text{Total Monthly Debt Payments} \) = Sum of all monthly debt obligations

- \( \text{Gross Monthly Income} \) = Pre-tax income from all sources

Your DTI ratio includes these key components:

- Monthly Debt Payments: Mortgage, rent, auto loans, credit cards, student loans, child support, alimony

- Gross Monthly Income: Salary, wages, bonuses, rental income, investment income, Social Security

- Housing Costs: Principal, interest, taxes, insurance, HOA fees

- Other Obligations: Any recurring monthly debt obligations

Salary

Wages

Mortgage

Credit Cards

Percentage

Approval

- Reduce debt payments: Pay down credit cards, refinance loans, consolidate debt

- Increase income: Seek raises, side jobs, or additional income streams

- Postpone large purchases: Avoid taking on new debt before applying for loans

- Pay off loans: Eliminate installment loans before applying for new credit

- Delay major purchases: Wait until after loan approval for large expenses

DTI Ratio Basics

Percentage of income used for debt payments.

\( \text{DTI} = \frac{\text{Total Monthly Debt Payments}}{\text{Gross Monthly Income}} \times 100\% \)

Where Debt Payments include all recurring obligations

- Lower DTI ratios indicate better financial health

- Most lenders prefer DTI under 43%

- Front-end DTI typically under 28%

Strategies

Methods to lower your debt-to-income ratio.

- Pay down existing debt

- Increase gross income

- Consolidate high-interest debt

- Refinance for lower payments

- Conventional loans: Max 43% DTI

- FHA loans: Max 50% DTI

- VA loans: No official DTI limit

- USDA loans: Max 41% DTI

DTI Ratio Learning Quiz

Which of the following is NOT included in the calculation of back-end DTI ratio?

The answer is D) Retirement contributions. The back-end DTI ratio includes all monthly debt obligations, such as mortgage, rent, auto loans, credit card minimum payments, student loans, child support, and alimony. However, retirement contributions are not considered debt obligations and are not included in DTI calculations.

Understanding what constitutes debt obligations is crucial for accurate DTI calculations. DTI ratios measure your ability to manage debt payments, not your total monthly expenses. Items like retirement contributions, while important for financial planning, are not debt payments and don't affect your DTI ratio.

Back-End DTI: Total monthly debt payments divided by gross monthly income

Debt Obligation: Recurring monthly payment required by contract

Retirement Contributions: Voluntary savings, not debt payments

• DTI only includes debt obligations

• Retirement contributions not included

• Includes recurring monthly payments only

• List all debt payments separately

• Exclude non-debt obligations

• Include all recurring obligations

• Including retirement contributions in DTI

• Forgetting to include all debt payments

• Including variable expenses like groceries

Calculate the DTI ratio for someone with $5,000 monthly gross income and $1,800 in total monthly debt payments. Show your work.

Using the DTI formula: \( \text{DTI} = \frac{\text{Total Monthly Debt Payments}}{\text{Gross Monthly Income}} \times 100\% \)

Given:

- Total Monthly Debt Payments = $1,800

- Gross Monthly Income = $5,000

Step 1: Divide total debt by income = $1,800 ÷ $5,000 = 0.36

Step 2: Convert to percentage = 0.36 × 100% = 36%

Therefore, the DTI ratio is 36%.

This calculation shows the straightforward division required for DTI calculation. The result indicates that 36% of the person's gross monthly income is committed to debt payments. This is generally considered acceptable for most lending criteria, which typically prefer DTI ratios under 43%.

DTI Ratio: Percentage of income used for debt payments

Gross Income: Pre-tax income from all sources

Monthly Debt: Recurring debt obligations

• Use gross (pre-tax) income

• Include all recurring debt payments

• Result is expressed as a percentage

• Always use gross income

• Include all debt obligations

• Round to one decimal place

• Using net (after-tax) income instead of gross

• Forgetting to include all debt payments

• Not multiplying by 100 to get percentage

Sarah has a gross monthly income of $6,000. Her housing costs (mortgage, taxes, insurance) total $1,500 per month. Her total monthly debt payments (including housing) are $2,400. Calculate both her front-end and back-end DTI ratios.

Step 1: Calculate Front-End DTI (Housing Ratio)

Front-End DTI = (Housing Costs ÷ Gross Income) × 100%

Front-End DTI = ($1,500 ÷ $6,000) × 100% = 0.25 × 100% = 25%

Step 2: Calculate Back-End DTI (Total Debt Ratio)

Back-End DTI = (Total Monthly Debt ÷ Gross Income) × 100%

Back-End DTI = ($2,400 ÷ $6,000) × 100% = 0.40 × 100% = 40%

Therefore, Sarah's front-end DTI is 25% and her back-end DTI is 40%.

This example demonstrates the difference between front-end and back-end DTI ratios. The front-end ratio (25%) shows housing costs as a percentage of income, which is within the typical 28% threshold for most lenders. The back-end ratio (40%) includes all debts and is also within the common 43% threshold, indicating good financial health.

Front-End DTI: Housing costs divided by gross income

Back-End DTI: All debt payments divided by gross income

Housing Ratio: Another term for front-end DTI

• Front-end DTI typically under 28%

• Back-end DTI typically under 43%

• Both ratios used by lenders

• Calculate both ratios for complete picture

• Front-end for housing loans

• Back-end for all loan types

• Confusing front-end with back-end DTI

• Including non-housing expenses in front-end

• Forgetting to include all debts in back-end

John wants to apply for a conventional mortgage. He earns $7,000 per month gross and has $2,800 in total monthly debt payments. The lender requires a back-end DTI of 43% or less. What is John's current DTI ratio, and does he qualify? If not, how much would he need to reduce his debt payments to qualify?

Step 1: Calculate John's current DTI ratio

DTI = (Total Debt ÷ Gross Income) × 100%

DTI = ($2,800 ÷ $7,000) × 100% = 0.40 × 100% = 40%

Step 2: Determine qualification status

Current DTI: 40%

Maximum allowed: 43%

Conclusion: John qualifies for the conventional mortgage since 40% < 43%

Step 3: Calculate maximum allowable debt for 43% DTI

Maximum debt = Gross Income × 43%

Maximum debt = $7,000 × 0.43 = $3,010

Step 4: Calculate how much more debt John could take on

Additional debt capacity = $3,010 - $2,800 = $210

Therefore, John's current DTI is 40%, and he qualifies for the conventional mortgage. He could take on up to $210 more in monthly debt payments while staying within the 43% threshold.

This demonstrates how DTI ratios are used in loan qualification decisions. John's 40% DTI is below the 43% threshold, so he qualifies. The calculation also shows how close he is to the limit and how much additional debt he could theoretically take on while still qualifying.

Loan Qualification: Meeting lender's criteria for approval

Conventional Loan: Standard mortgage not government-backed

DTI Threshold: Maximum acceptable DTI ratio

• Conventional loans typically max 43% DTI

• FHA loans may allow up to 50% DTI

• VA loans have no official DTI limit

• Know your loan type requirements

• Calculate DTI before applying

• Improve ratio if close to limit

• Not knowing loan-specific DTI requirements

• Calculating DTI after applying

• Assuming all loans have same limits

Which of the following is the most effective strategy for reducing your DTI ratio?

The answer is C) Both decreasing debt payments and increasing income. Since DTI is calculated as debt payments divided by income, reducing the numerator (debt) or increasing the denominator (income) will both lower the ratio. Combining both strategies is most effective. Simply changing payment timing does not affect the monthly debt obligations used in the calculation.

Understanding the mathematical relationship in the DTI formula reveals that both reducing debt payments and increasing income can lower your DTI ratio. The most effective approach combines both strategies, though this may take time. Short-term improvements typically focus on reducing debt payments through consolidation, refinancing, or paying down balances.

DTI Improvement: Lowering the debt-to-income ratio

Debt Reduction: Decreasing monthly debt obligations

Income Enhancement: Increasing gross monthly income

• Both debt reduction and income increase lower DTI

• Debt reduction often more immediate

• Income increase provides ongoing benefit

• Focus on debt reduction first

• Pursue income enhancement long-term

• Combine strategies for maximum impact

• Thinking only one strategy works

• Not considering both approaches

• Assuming timing changes affect DTI

FAQ

Q: What is an acceptable DTI ratio for mortgage approval?

A: The acceptable DTI ratio varies by loan type:

- Conventional loans: Maximum 43% DTI, ideally under 36%

- FHA loans: Up to 50% DTI in some cases

- VA loans: No official DTI limit, but lenders typically prefer under 41%

- USDA loans: Maximum 41% DTI

Using the formula: \( \text{DTI} = \frac{\text{Debt}}{\text{Income}} \times 100\% \), if you have \( \$4{,}000 \) monthly income and want a conventional loan, your maximum monthly debt should be \( \$4{,}000 \times 0.43 = \$1{,}720 \).

Q: How can I improve my DTI ratio before applying for a loan?

A: There are two primary ways to improve your DTI ratio:

- Reduce debt payments: Pay down credit cards, consolidate high-interest debt, or refinance existing loans to lower monthly payments

- Increase income: Seek raises, side jobs, or additional income streams

For example, if your DTI is 50% with \( \$5{,}000 \) income and \( \$2{,}500 \) in debt payments, reducing debt to \( \$2{,}000 \) would lower your DTI to 40% (\( \frac{2{,}000}{5{,}000} \times 100\% \)). Alternatively, increasing income to \( \$6{,}250 \) would achieve the same result.