Annuity Calculator

Financial planning • Investment returns

Annuity Formulas:

Show the calculatorFuture Value of Annuity: \( FV = PMT \times \frac{(1+r)^n - 1}{r} \)

Present Value of Annuity: \( PV = PMT \times \frac{1 - (1+r)^{-n}}{r} \)

Where:

- \( FV \) = Future Value

- \( PV \) = Present Value

- \( PMT \) = Payment amount

- \( r \) = Interest rate per period

- \( n \) = Number of periods

These formulas calculate the value of a series of equal payments made at regular intervals. The future value formula determines how much an annuity will be worth after a certain number of periods, while the present value formula calculates the current value of future annuity payments.

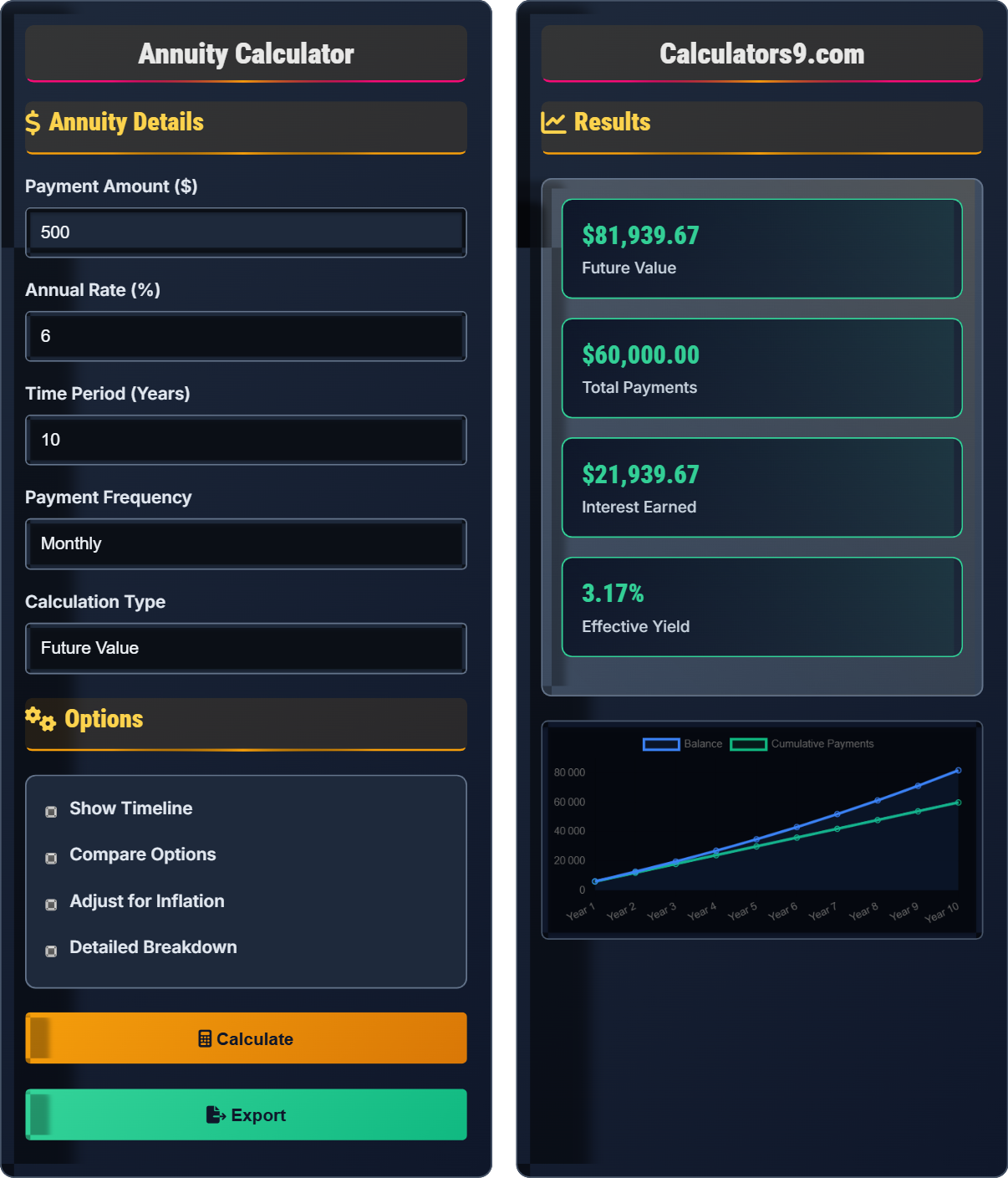

Example: For an annuity with monthly payments of $500 at an annual interest rate of 6% (0.5% monthly) for 10 years (120 months):

Future Value: \( FV = 500 \times \frac{(1+0.005)^{120} - 1}{0.005} \approx \$81,940 \)

Thus, the annuity will be worth approximately $81,940 after 10 years.

Annuity Details

Options

Results

| Year | Balance | Payments | Interest |

|---|

| Component | Amount | Percentage |

|---|

Comprehensive Annuity Guide

An annuity is a financial product that provides regular payments to an individual, typically used as an income stream for retirees. It's a contract between an individual and an insurance company where the individual makes a lump-sum payment or series of payments in exchange for regular disbursements beginning immediately or at some point in the future.

The standard annuity calculations use these formulas:

\(PV = PMT \times \frac{1 - (1+r)^{-n}}{r}\)

Where:

- \(FV\) = Future Value of Annuity

- \(PV\) = Present Value of Annuity

- \(PMT\) = Payment amount per period

- \(r\) = Interest rate per period

- \(n\) = Number of periods

Key advantages of annuities include:

- Guaranteed Income: Provides steady payments for life or specified period

- Tax Deferral: Growth is tax-deferred until withdrawal

- Estate Protection: Can provide benefits to beneficiaries

- Inflation Protection: Some offer inflation-adjusted payments

- Professional Management: Expert oversight of investments

- Start Early: Take advantage of compound interest over longer periods

- Consistent Contributions: Regular payments maximize growth potential

- Match Time Horizon: Align annuity type with retirement timeline

- Consider Fees: Understand all associated costs and charges

- Diversify: Use annuities as part of a broader portfolio strategy

Annuity Basics

Financial product providing regular payments over time.

\(FV = PMT \times \frac{(1+r)^n - 1}{r}\)

Where FV=future value, PMT=payment, r=rate, n=periods.

- Higher rates = higher future values

- Longer periods = exponential growth

- More frequent payments = greater growth

Strategies

Early contributions generate interest on interest over time.

- Start contributing early

- Increase contributions regularly

- Choose appropriate payment frequency

- Select optimal interest rate environment

- Liquidity restrictions

- Penalty fees

- Tax implications

- Inflation impact

Annuity Learning Quiz

Which of the following factors does NOT directly affect the future value of an ordinary annuity?

The answer is D) Current stock market prices. The future value of an ordinary annuity is determined by the payment amount (PMT), interest rate (r), and number of periods (n) according to the formula: \(FV = PMT \times \frac{(1+r)^n - 1}{r}\). Stock market prices are not a factor in this calculation.

This question tests understanding of the fundamental variables that determine annuity values. The future value formula only includes the payment amount, interest rate, and time periods. While stock market performance might indirectly influence interest rates, it's not a direct component of the annuity calculation itself.

Ordinary Annuity: Payments made at the end of each period

Future Value: The value of an asset or cash at a specified date in the future

Compounding: Interest earned on both principal and previously earned interest

• Future value increases with higher payment amounts

• Higher interest rates lead to greater future values

• More periods result in exponential growth due to compounding

• Remember: FV = PMT × [(1+r)^n - 1]/r

• The interest rate and number of periods are exponentially related

• Small changes in rate can have large impacts over time

• Including irrelevant economic indicators in annuity calculations

• Forgetting to adjust interest rates for payment frequency

• Confusing present value with future value calculations

Calculate the future value of an ordinary annuity with monthly payments of $1,000 for 20 years at an annual interest rate of 5%. Show your work.

Using the future value of annuity formula: \(FV = PMT \times \frac{(1+r)^n - 1}{r}\)

Given:

- PMT = $1,000

- r = 0.05 ÷ 12 = 0.004167

- n = 20 × 12 = 240

Step 1: Calculate (1+r)^n = (1.004167)^240 = 2.7126

Step 2: Calculate numerator: (1+r)^n - 1 = 2.7126 - 1 = 1.7126

Step 3: Calculate FV = $1,000 × (1.7126/0.004167) = $1,000 × 411.00 = $411,000

Therefore, the future value is approximately $411,000.

This calculation demonstrates the power of compound interest over time. The investor contributes $240,000 ($1,000 × 240 months), but ends up with $411,000 due to compound interest. The key insight is that early contributions earn interest for longer periods, creating exponential growth.

Compound Interest: Interest calculated on both principal and accumulated interest

Monthly Rate: Annual interest rate divided by 12

Number of Periods: Total number of payment periods

• Always convert annual rates to periodic rates for calculations

• Convert time periods to match payment frequency

• The formula accounts for compound interest over all periods

• Remember: r = annual rate ÷ payment frequency

• Remember: n = years × payment frequency

• Use a calculator for complex exponent calculations

• Forgetting to convert annual rates to monthly rates

• Using the wrong number of periods (not adjusting for frequency)

• Making calculation errors with large exponents

Jennifer wants to retire in 30 years and needs $1,000,000 in her retirement account. If she can earn 6% annually on her investments, how much must she invest each month to reach her goal? Assume monthly compounding.

We need to solve for PMT in the future value formula: \(FV = PMT \times \frac{(1+r)^n - 1}{r}\)

Rearranging: \(PMT = \frac{FV \times r}{(1+r)^n - 1}\)

Given:

- FV = $1,000,000

- r = 0.06 ÷ 12 = 0.005

- n = 30 × 12 = 360

Step 1: Calculate (1+r)^n = (1.005)^360 = 6.0226

Step 2: Calculate numerator: FV × r = $1,000,000 × 0.005 = $5,000

Step 3: Calculate denominator: (1+r)^n - 1 = 6.0226 - 1 = 5.0226

Step 4: Calculate PMT = $5,000 ÷ 5.0226 = $995.50

Therefore, Jennifer must invest approximately $995.50 per month to reach her goal.

This problem shows how consistent monthly contributions can grow to substantial amounts over long periods. Jennifer will contribute $358,380 ($995.50 × 360 months) but will earn $641,620 in interest. This demonstrates the importance of starting early and maintaining consistent contributions.

Retirement Planning: Setting financial goals and strategies for post-work income

Monthly Investment: Regular contributions to build wealth over time

Compound Growth: Exponential increase due to earning returns on returns

• Longer time horizons allow smaller monthly contributions

• Higher interest rates reduce required contributions

• Consistent contributions are key to reaching goals

• Set up automatic monthly transfers to stay consistent

• Increase contributions when receiving raises or bonuses

• Use online calculators to model different scenarios

• Underestimating the time needed to reach retirement goals

• Overestimating expected returns and under-saving

• Not accounting for inflation in long-term planning

David has an annuity that will pay him $2,000 per month for 20 years starting today. If inflation averages 3% annually, what is the present value of these payments in today's dollars? (Assume a discount rate of 3% to account for inflation)

We need to calculate the present value of an annuity with adjustments for inflation. Using the present value formula: \(PV = PMT \times \frac{1 - (1+r)^{-n}}{r}\)

Given:

- PMT = $2,000

- r = 0.03 ÷ 12 = 0.0025

- n = 20 × 12 = 240

Step 1: Calculate (1+r)^-n = (1.0025)^-240 = 0.5492

Step 2: Calculate numerator: 1 - (1+r)^-n = 1 - 0.5492 = 0.4508

Step 3: Calculate PV = $2,000 × (0.4508/0.0025) = $2,000 × 180.32 = $360,640

Therefore, the present value of David's annuity payments in today's dollars is approximately $360,640.

This example demonstrates how inflation erodes purchasing power over time. While David will receive $480,000 in nominal terms ($2,000 × 240), the real value adjusted for inflation is only $360,640 in today's dollars. This illustrates why it's important to consider inflation when planning for long-term financial needs.

Inflation: General increase in prices and fall in purchasing value of money

Present Value: Current value of future payments discounted for time value of money

Purchasing Power: Amount of goods or services that can be bought with a unit of currency

• Inflation reduces the real value of future payments

• Discount rates account for the time value of money

• Higher inflation rates significantly reduce present value

• Adjust annuity calculations for inflation when planning long-term

• Consider inflation-protected securities for retirement

• Factor inflation into retirement income projections

• Ignoring inflation when calculating future values

• Not adjusting discount rates for inflation expectations

• Confusing nominal and real values in financial planning

Which of the following statements about payment frequency is TRUE for an ordinary annuity?

The answer is C) More frequent payments result in higher future values. When payments are made more frequently, each payment earns interest for a longer period before the next payment is made. For example, a monthly payment begins earning interest immediately, while with annual payments, the first payment earns interest for the entire year before the next payment is added.

This demonstrates the time value of money principle. More frequent payments mean more money is earning interest at any given time. Monthly payments allow for more compounding periods within a year, leading to higher overall returns compared to annual payments with the same total contribution amount.

Compounding Frequency: How often interest is calculated and added to principal

Time Value of Money: Concept that money available now is worth more than the same amount later

Effective Annual Rate: Actual return on investment after accounting for compounding

• More frequent payments allow for more compounding opportunities

• Monthly payments generally yield higher returns than annual payments

• Payment frequency must match interest compounding frequency in calculations

• Make payments as early as possible in the period

• Choose investments with more frequent compounding

• Consider monthly contributions over annual lump sums

• Assuming all payment frequencies produce equal returns

• Not adjusting interest rates for different payment frequencies

• Forgetting that timing affects compounding benefits

FAQ

Q: How do annuities differ from other investment vehicles?

A: Annuities are unique because they provide guaranteed income streams, unlike stocks or bonds which have variable returns. The key difference lies in the payment structure:

For an ordinary annuity, the future value formula is: \( FV = PMT \times \frac{(1+r)^n - 1}{r} \)

This formula shows that annuities convert a series of payments into a future value through compound interest. Unlike individual investments, annuities provide systematic withdrawals or deposits with predictable outcomes. While stocks might average 7-10% returns, annuities offer stability with typically 3-6% returns depending on the type.

Q: Should I choose immediate or deferred annuities?

A: The choice depends on your age and income needs:

- Immediate Annuities: Payments start right away, ideal for those ready to retire. For example, a $100,000 investment at age 65 might provide $500-700/month for life.

- Deferred Annuities: Accumulate value over time, perfect for retirement planning. Using the future value formula: \( FV = PMT \times \frac{(1+r)^n - 1}{r} \), a 40-year-old investing $500/month at 5% for 25 years would accumulate approximately $293,000.

Deferred annuities allow your money to grow tax-deferred before you start receiving payments, maximizing the eventual income stream.