Bond Calculator

Fixed income • Yield analysis

Bond Valuation Formula:

Show the calculatorBond Price: \( BP = \sum_{t=1}^{n} \frac{C}{(1+r)^t} + \frac{F}{(1+r)^n} \)

Current Yield: \( CY = \frac{\text{Annual Coupon Payment}}{\text{Current Bond Price}} \)

Yield to Maturity: \( YTM \approx \frac{C + \frac{F-P}{n}}{\frac{F+P}{2}} \)

Where:

- \( BP \) = Bond Price

- \( C \) = Annual coupon payment

- \( r \) = Required yield (discount rate)

- \( F \) = Face value (par value)

- \( n \) = Number of years to maturity

- \( P \) = Current price

These formulas calculate various bond metrics including price, current yield, and yield to maturity. Bond pricing involves discounting future cash flows (coupon payments and face value) to present value using the market's required yield.

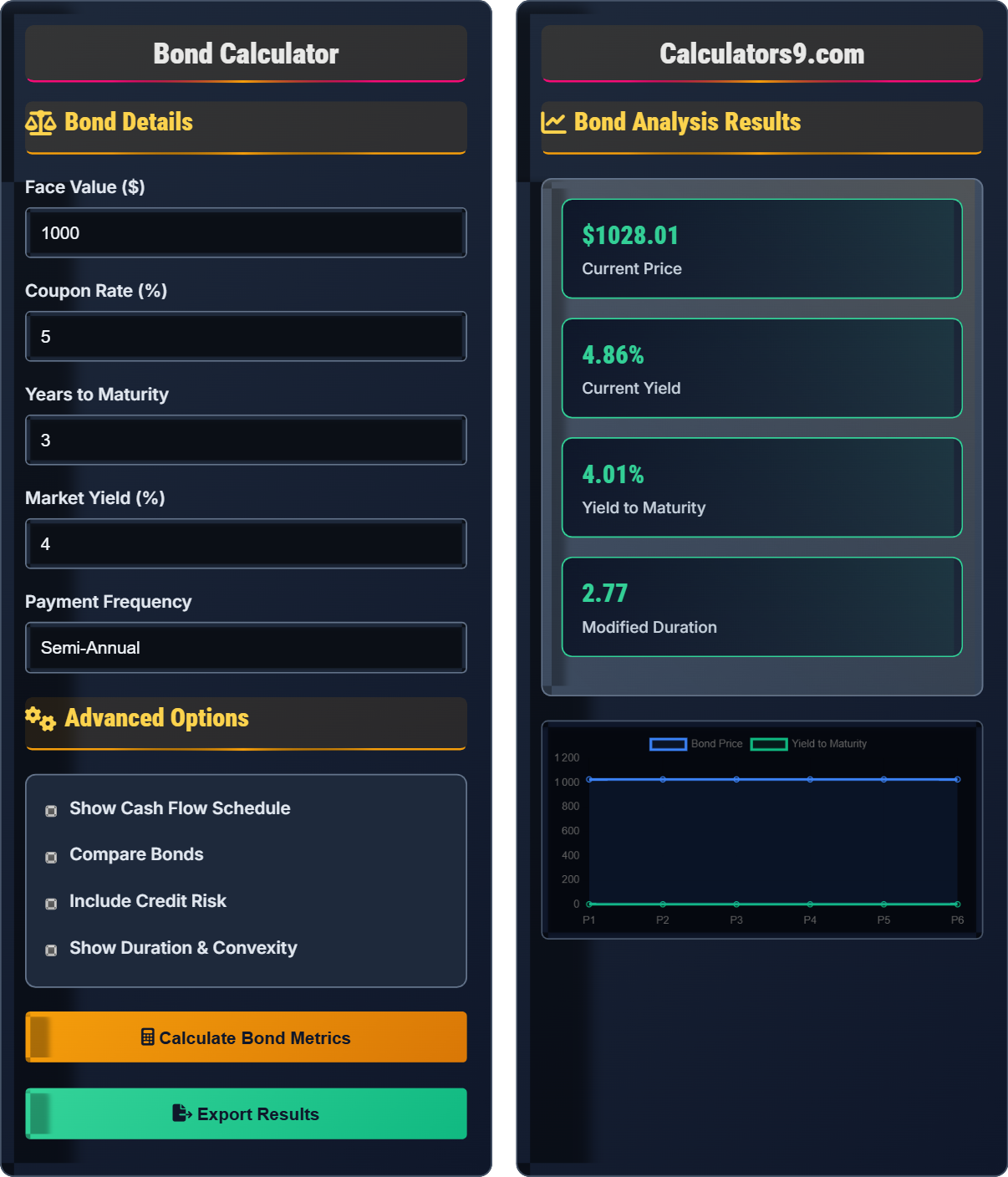

Example: For a bond with $1,000 face value, 5% annual coupon, 3 years to maturity, and market yield of 4%:

Coupon payment: $1,000 × 0.05 = $50

Bond Price: $50/(1.04) + $50/(1.04)² + $1,050/(1.04)³ ≈ $1,027.75

Thus, the bond trades at a premium of $1,027.75.

Bond Details

Advanced Options

Bond Analysis Results

| Period | Payment | Discount Factor | Present Value |

|---|

| Metric | Value | Explanation |

|---|

Comprehensive Bond Investment Guide

A bond is a debt security where an investor loans money to an entity (corporate or governmental) that borrows the funds for a defined period at a fixed interest rate. Bonds are used by companies, municipalities, states, and sovereign governments to finance projects and operations. Owners of bonds are debtholders, or creditors, of the issuer.

The standard bond pricing calculation uses this formula:

Where:

- \(BP\) = Bond Price

- \(C\) = Annual coupon payment

- \(r\) = Required yield (discount rate)

- \(F\) = Face value (par value)

- \(n\) = Number of years to maturity

Key advantages of bond investments include:

- Predictable Income: Regular coupon payments provide steady cash flow

- Principal Protection: Face value returned at maturity (subject to credit risk)

- Portfolio Diversification: Bonds often move inversely to stocks

- Defensive Asset: Lower volatility than equities

- Income Generation: Suitable for income-focused investors

- Understand Duration: Longer duration bonds are more sensitive to interest rate changes

- Monitor Credit Ratings: Changes can affect bond prices significantly

- Consider Inflation: Fixed coupon payments lose purchasing power over time

- Check Call Provisions: Callable bonds may be redeemed early

- Diversify Maturity Dates: Reduce interest rate risk exposure

Bond Investment Fundamentals

Debt security representing a loan from investor to issuer.

\(BP = \sum_{t=1}^{n} \frac{C}{(1+r)^t} + \frac{F}{(1+r)^n}\)

Where BP=bond price, C=coupon payment, r=yield, F=face value, n=periods.

- Bond prices move inversely to interest rates

- Higher credit risk requires higher yield

- Longer maturity increases interest rate sensitivity

Strategies

Measure of bond price sensitivity to interest rate changes.

- Assess credit quality and rating

- Understand interest rate environment

- Match maturity to investment horizon

- Consider call provisions and special features

- Interest rate risk increases with maturity

- Credit risk varies by issuer

- Inflation risk affects fixed payments

- Liquidity varies by bond type

Bond Investment Learning Quiz

When market interest rates rise, what happens to existing bond prices?

The answer is B) Bond prices fall. When market interest rates rise, existing bonds with lower coupon rates become less attractive compared to new bonds offering higher rates. The bond pricing formula shows that as the discount rate (r) increases, the present value of future cash flows decreases, causing bond prices to fall.

This fundamental principle of bond investing is known as interest rate risk. Using the bond valuation formula \(BP = \sum_{t=1}^{n} \frac{C}{(1+r)^t} + \frac{F}{(1+r)^n}\), when r (market yield) increases, the denominator of each fraction increases, making each present value smaller, which reduces the total bond price.

Interest Rate Risk: Risk that bond prices will decline due to rising interest rates

Discount Rate: Market rate used to calculate present value of future cash flows

Bond Price Inverse Relationship: Bond prices move opposite to interest rates

• Bond prices and interest rates have inverse relationship

• Longer-term bonds are more sensitive to rate changes

• Higher coupon bonds are less sensitive to rate changes

• Monitor interest rate trends before investing in bonds

• Consider shorter-term bonds when rates are expected to rise

• Longer-duration bonds experience larger price swings

• Assuming bond prices move in the same direction as interest rates

• Not understanding the inverse relationship

• Ignoring interest rate risk in bond investments

Calculate the current yield for a bond with a face value of $1,000, a coupon rate of 6%, and a current market price of $950. Show your work.

Using the current yield formula: \(CY = \frac{\text{Annual Coupon Payment}}{\text{Current Bond Price}}\)

Step 1: Calculate annual coupon payment = $1,000 × 0.06 = $60

Step 2: Calculate current yield = $60 ÷ $950 = 0.0632 = 6.32%

Therefore, the current yield is 6.32%.

Current yield measures the annual income from a bond as a percentage of its current market price, not its face value. Since this bond is trading below par ($950 vs $1,000), the current yield (6.32%) is higher than the coupon rate (6%). This is because the investor pays less for the same $60 in annual income.

Current Yield: Annual coupon payment divided by current market price

Coupon Payment: Annual interest payment based on face value

Face Value: Amount returned at bond maturity

• Current yield = Annual coupon ÷ Current price

• Bonds trading at discount have higher current yield than coupon rate

• Bonds trading at premium have lower current yield than coupon rate

• Current yield doesn't account for capital gains or losses at maturity

• Compare current yield to yield to maturity for complete picture

• Discount bonds have higher current yields than coupon rate

• Dividing coupon by face value instead of current price

• Confusing current yield with yield to maturity

• Not accounting for premium/discount relationship

A bond has a face value of $1,000, a 5% annual coupon rate, and 5 years to maturity. If the market yield is 4%, will this bond trade at a premium or discount? Calculate the approximate price. (Hint: Compare coupon rate to market yield)

Since the coupon rate (5%) is higher than the market yield (4%), the bond will trade at a premium (above par value).

Using the simplified YTM approximation formula: \(YTM \approx \frac{C + \frac{F-P}{n}}{\frac{F+P}{2}}\)

Given that YTM = 4%, C = $50, F = $1,000, n = 5, solving for P:

0.04 ≈ (50 + (1000-P)/5) / ((1000+P)/2)

Solving this equation gives an approximate price of $1,045.

Therefore, the bond trades at a premium of $1,045.

When a bond's coupon rate exceeds the market yield, it offers higher returns than newly issued bonds, making it more attractive. Investors are willing to pay more than face value (premium) to secure the higher coupon payments. Conversely, if the coupon rate is below market yield, the bond trades at a discount.

Bond Premium: Bond trading above face value due to higher coupon rate

Bond Discount: Bond trading below face value due to lower coupon rate

Par Value: Face value of the bond ($1,000 in most cases)

• Coupon rate > Market yield = Bond trades at premium

• Coupon rate < Market yield = Bond trades at discount

• Coupon rate = Market yield = Bond trades at par

• Higher coupon rate means premium price

• Lower coupon rate means discount price

• Equal rates mean par price

• Confusing the relationship between coupon rate and market yield

• Assuming higher coupon always means better investment

• Not understanding why premium/discount occurs

You own two bonds: Bond A with 2 years to maturity and Bond B with 10 years to maturity, both with identical coupon rates and yields. If interest rates increase by 1%, which bond will experience a larger percentage price change? Explain why. (Hint: Consider interest rate sensitivity)

Bond B with 10 years to maturity will experience a larger percentage price change. This is because longer-term bonds have higher duration and are more sensitive to interest rate changes.

Using the modified duration concept: % Change in Price ≈ -Duration × Change in Yield

Since Bond B has a longer time to maturity, it has a higher duration value. When interest rates rise by 1%, Bond B's price will fall more significantly than Bond A's price because it has more future cash flows that are discounted at the higher rate.

Therefore, Bond B experiences greater price volatility due to its longer duration.

This demonstrates the fundamental relationship between bond maturity and interest rate sensitivity. The longer the time to maturity, the more sensitive the bond's price is to interest rate changes. This is because longer-term bonds have more future cash flows that are affected by changes in the discount rate, leading to larger price swings.

Duration: Measure of bond price sensitivity to interest rate changes

Interest Rate Sensitivity: How much bond price changes with interest rate movement

Price Volatility: Degree of price fluctuation due to market changes

• Longer maturity = Higher interest rate sensitivity

• Higher duration = Greater price volatility

• Zero-coupon bonds have duration equal to maturity

• Match bond duration to your investment time horizon

• Consider shorter-term bonds in rising rate environments

• Longer-term bonds are riskier in volatile rate markets

• Assuming all bonds react equally to interest rate changes

• Not considering maturity when assessing risk

• Ignoring duration in bond selection

Which type of bond typically offers the highest yield to compensate for credit risk?

The answer is D) High-yield (junk) bonds. These bonds have lower credit ratings (typically BB or below) and offer higher yields to compensate investors for the increased risk of default. The yield premium over risk-free Treasury bonds is called the credit spread.

There is a direct relationship between credit risk and required yield. Treasury bonds are considered risk-free and offer the lowest yields. As credit risk increases, investors demand higher compensation, resulting in higher yields. High-yield bonds, also called junk bonds, carry significant default risk, which is reflected in their higher yields compared to investment-grade bonds.

High-Yield Bonds: Bonds with speculative credit ratings offering higher yields

Credit Risk: Risk that the issuer will default on payments

Credit Spread: Yield premium over risk-free rate for credit risk

• Higher credit risk = Higher required yield

• Treasury bonds set the risk-free baseline

• Credit spreads widen during economic stress

• Review credit ratings before investing in corporate bonds

• Higher yields indicate higher risk

• Diversify across credit qualities

• Assuming high yields always mean better investments

• Not understanding the relationship between risk and return

• Ignoring credit quality in pursuit of high yields

FAQ

Q: What's the difference between coupon rate and yield to maturity?

A: The coupon rate is the fixed annual interest rate paid by the bond issuer based on the bond's face value. The yield to maturity (YTM) is the total return anticipated on a bond if held until maturity, accounting for the current market price.

For example, using the formula \( BP = \sum_{t=1}^{n} \frac{C}{(1+r)^t} + \frac{F}{(1+r)^n} \), if a bond with a 5% coupon ($50 annual payment) and $1,000 face value trades at $950, the coupon rate remains 5%, but the YTM will be higher than 5% because the investor gets the full $1,000 face value back at maturity while paying only $950 initially.

Q: How do interest rates affect bond prices?

A: Bond prices and interest rates have an inverse relationship, as shown in the bond pricing formula: \( BP = \sum_{t=1}^{n} \frac{C}{(1+r)^t} + \frac{F}{(1+r)^n} \).

When market rates (r) increase, the denominator of each fraction increases, making the present value of future cash flows smaller. This causes bond prices to fall. Conversely, when rates decrease, bond prices rise.

For example, if you hold a 5% coupon bond and new bonds are issued at 6%, your bond becomes less attractive, causing its price to drop in the secondary market.