CD Calculator

Certificate of deposit • Safe investment

CD Interest Formula:

Show the calculatorCompound Interest: \( FV = P \times (1 + \frac{r}{n})^{nt} \)

Simple Interest: \( FV = P \times (1 + rt) \)

Where:

- \( FV \) = Future Value (maturity amount)

- \( P \) = Principal (initial investment)

- \( r \) = Annual interest rate (decimal)

- \( n \) = Number of times interest is compounded per year

- \( t \) = Time in years

Certificates of deposit (CDs) typically use compound interest, with most banks compounding interest daily or monthly. Some promotional CDs may offer simple interest. The formula calculates the total amount at maturity including principal and interest earned.

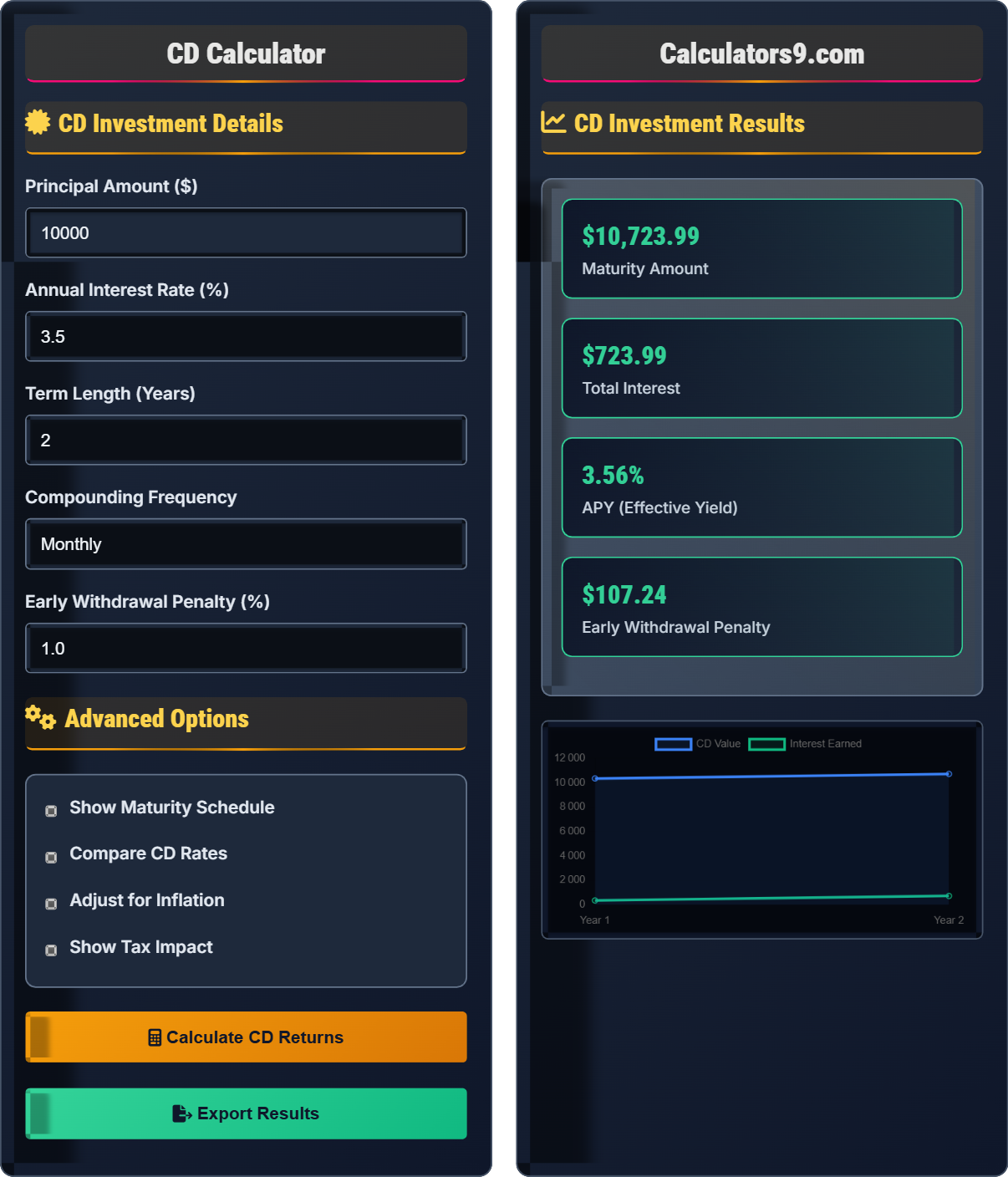

Example: For a $10,000 CD at 3.5% annual interest compounded daily for 2 years:

\( FV = 10,000 \times (1 + \frac{0.035}{365})^{365 \times 2} \)

\( FV = 10,000 \times (1.00009589)^{730} \approx \$10,725 \)

Thus, the CD would mature to approximately $10,725.

CD Investment Details

Advanced Options

CD Investment Results

| Year | Balance | Interest Earned |

|---|

| Component | Amount | Percentage |

|---|

Comprehensive CD Investment Guide

A Certificate of Deposit (CD) is a time deposit offered by banks and credit unions that provides a fixed interest rate for a specified term. CDs are considered low-risk investments because they're FDIC-insured up to $250,000 per depositor, per institution. They offer higher interest rates than regular savings accounts in exchange for locking up funds for a predetermined period.

The standard CD calculation uses this compound interest formula:

Where:

- \(FV\) = Future Value (maturity amount)

- \(P\) = Principal (initial investment)

- \(r\) = Annual interest rate (decimal)

- \(n\) = Number of times interest is compounded per year

- \(t\) = Time in years

Key advantages of CD investments include:

- FDIC Insurance: Up to $250,000 is federally insured

- Fixed Returns: Predictable interest income

- Higher Rates: Better than typical savings accounts

- No Market Risk: Principal is protected

- Disciplined Saving: Forces you to save for the term

- Shop for Rates: Compare rates across multiple institutions

- Consider Jumbo CDs: Higher minimums often offer better rates

- Watch for Special Promotions: Banks often offer limited-time higher rates

- Plan for Liquidity Needs: Don't lock all funds in long-term CDs

- Understand Penalties: Know the cost of early withdrawal

CD Investment Fundamentals

Time deposit with fixed interest rate and maturity date.

\(FV = P \times (1 + \frac{r}{n})^{nt}\)

Where FV=maturity amount, P=principal, r=rate, n=frequency, t=time.

- Higher terms typically offer higher rates

- Early withdrawal incurs penalties

- FDIC insurance protects up to $250,000

Strategies

Staggering CD maturities for balanced liquidity and returns.

- Research current CD rates

- Determine appropriate term length

- Consider laddering strategy

- Understand early withdrawal penalties

- Interest rate environment affects returns

- Minimum deposit requirements vary

- Automatic renewal policies differ

- Tax implications on interest income

CD Investment Learning Quiz

Which statement about CD safety is TRUE?

The answer is B) CDs are insured up to $250,000 per depositor, per institution. This FDIC insurance protects the principal amount invested in CDs at participating banks, making them one of the safest investment options available. The insurance covers both the principal and any accrued interest up to the maximum limit.

This question addresses one of the key benefits of CDs: federal insurance protection. Understanding the FDIC insurance limit is crucial for CD investors to ensure their funds are fully protected. Investors with more than $250,000 should consider spreading deposits across multiple institutions to maintain full coverage.

FDIC Insurance: Federal deposit insurance protecting bank deposits up to $250,000

Principal Protection: Guarantee that initial investment amount will be returned

Deposit Insurance: Government-backed protection for bank deposits

• FDIC insurance covers up to $250,000 per depositor, per institution

• Coverage includes both principal and accrued interest

• Different ownership categories may qualify for separate coverage

• Verify that your bank is FDIC-insured before investing

• Keep deposits under $250,000 per institution for full coverage

• Use joint accounts to increase coverage limits

• Assuming all deposits at any bank are fully insured

• Not understanding the per-institution limit

• Depositing more than $250,000 at a single institution without realizing the risk

Calculate the maturity amount for a $5,000 CD at 4% annual interest compounded monthly for 3 years. Show your work.

Using the CD formula: \(FV = P \times (1 + \frac{r}{n})^{nt}\)

Given:

- P = $5,000

- r = 4% = 0.04

- n = 12 (monthly compounding)

- t = 3 years

Step 1: Calculate rate per period: r/n = 0.04/12 = 0.003333

Step 2: Calculate total periods: nt = 12 × 3 = 36

Step 3: Calculate (1 + r/n)^(nt) = (1.003333)^36 = 1.1273

Step 4: Calculate FV = $5,000 × 1.1273 = $5,636.50

Therefore, the maturity amount is $5,636.50.

This calculation demonstrates how to properly apply the CD interest formula. The key is to divide the annual rate by the number of compounding periods per year and multiply the number of years by the same factor. This ensures the formula accounts for the actual compounding frequency, which affects the final return.

Maturity Amount: Total value at the end of the CD term

Compounding Period: Interval at which interest is calculated

Principal: Initial amount invested

• Always adjust rate and time for compounding frequency

• Rate per period = Annual rate ÷ Compounding frequency

• Total periods = Years × Compounding frequency

• Remember: r/n and n*t adjustments

• Use a calculator for complex exponent calculations

• Double-check your rate and time adjustments

• Forgetting to adjust the rate for compounding frequency

• Using the wrong number of periods in calculations

• Applying annual rate directly without dividing by frequency

Sarah has $30,000 to invest in CDs. Instead of putting all money in a 5-year CD at 3.5%, she creates a ladder with $10,000 in each of a 1-year, 3-year, and 5-year CD. What are the advantages of this strategy compared to the single 5-year CD?

The CD laddering strategy provides several advantages:

1. Liquidity: Every year, $10,000 becomes available for withdrawal or reinvestment at potentially higher rates

2. Rate Flexibility: As shorter-term CDs mature, they can be reinvested at higher prevailing rates if interest rates rise

3. Reduced Interest Rate Risk: Not all funds are locked in at potentially lower rates for the entire 5-year period

4. Steady Returns: Provides a balance between short-term access and long-term higher rates

While the single 5-year CD might offer slightly higher returns if rates remain stable, the ladder provides more flexibility and potential for capturing rising rates.

CD laddering is a strategic approach that balances the competing needs for liquidity and higher returns. By staggering maturity dates, investors can benefit from both short-term flexibility and long-term higher rates. This strategy is particularly valuable in uncertain interest rate environments.

CD Laddering: Strategy of investing in multiple CDs with different maturity dates

Interest Rate Risk: Risk that interest rates will change, affecting investment returns

Liquidity: Ease of converting investment to cash

• CD ladders provide both liquidity and higher rate potential

• More frequent maturities allow for rate adjustments

• Strategy works well in rising rate environments

• Spread investments across multiple maturity dates

• Consider 1-2-3-5 year ladders for good balance

• Reinvest maturing CDs at current market rates

• Putting all money in the longest-term CD for highest rate

• Not considering interest rate trends

• Ignoring the need for liquidity

You invested $20,000 in a 3-year CD at 4% annual interest. The early withdrawal penalty is 6 months of interest. If you withdraw after 1 year, how much will you lose in penalties, and what will be your net return? (Hint: Calculate 6 months of interest on the principal)

Step 1: Calculate 6 months of interest penalty

Annual interest = $20,000 × 0.04 = $800

6-month interest penalty = $800 ÷ 2 = $400

Step 2: Calculate interest earned in 1 year

Interest earned = $20,000 × 0.04 = $800

Step 3: Calculate net return after penalty

Net return = Interest earned - Penalty = $800 - $400 = $400

Step 4: Calculate total amount received

Total = Principal - Penalty = $20,000 - $400 = $19,600

Therefore, you lose $400 in penalties and have a net return of $400.

This example demonstrates the significant cost of early withdrawal penalties. The penalty equals 6 months of interest, which in this case is $400. While the investment earned $800 in interest during the year, the penalty reduces the effective return to $400. This highlights the importance of ensuring you won't need the funds before the CD matures.

Early Withdrawal Penalty: Fee charged for withdrawing CD funds before maturity

Interest Rate Risk: Risk of losing potential interest through early withdrawal

Opportunity Cost: Lost interest from early withdrawal

• Early withdrawal penalties can be substantial

• Penalties often equal several months of interest

• Consider penalties before investing in long-term CDs

• Only invest money you won't need before maturity

• Understand the penalty structure before investing

• Consider no-penalty CDs for more flexibility

• Not reading the fine print about penalties

• Assuming all CDs have the same penalty structure

• Investing emergency funds in long-term CDs

What is the difference between the stated interest rate and APY (Annual Percentage Yield) for a CD?

The answer is A) APY includes the effect of compounding, while the interest rate does not. The stated interest rate (also called nominal rate) is the annual rate without considering compounding. APY reflects the actual return taking into account how often interest is compounded during the year.

This distinction is crucial for comparing CD returns. For example, a CD with a 4% stated rate compounded monthly has an APY of approximately 4.07%. The more frequent the compounding, the higher the APY will be compared to the stated rate. APY provides a standardized way to compare different CDs.

APY (Annual Percentage Yield): Effective annual rate including compounding

Stated Interest Rate: Nominal annual rate without compounding effect

Compounding Effect: Additional interest earned on previously earned interest

• APY is always equal to or higher than the stated rate

• More frequent compounding increases the APY difference

• Use APY to compare different CD offerings

• Always compare CDs using APY, not just stated rate

• Daily compounding typically offers the highest APY

• APY gives you the true annual return

• Comparing CDs using only stated interest rates

• Not understanding how compounding affects returns

• Assuming all CDs with the same stated rate are equivalent

FAQ

Q: What's the difference between simple and compound interest in CDs?

A: Most CDs use compound interest, calculated using the formula: \( FV = P \times (1 + \frac{r}{n})^{nt} \). This means interest is earned on both the principal and previously earned interest.

Simple interest uses: \( FV = P \times (1 + rt) \), where interest is only calculated on the principal amount.

For example, with $10,000 at 4% for 3 years:

- Compound interest (monthly): $10,000 × (1.003333)^36 = $11,273

- Simple interest: $10,000 × (1 + 0.04×3) = $11,200

Compound interest yields $73 more due to earning interest on interest.

Q: Should I choose a longer-term CD for higher returns?

A: Longer-term CDs typically offer higher interest rates, but consider your financial needs. Using the CD formula \( FV = P \times (1 + \frac{r}{n})^{nt} \), a 5-year CD at 4.0% would yield more than a 1-year CD at 3.0%.

However, longer terms come with:

- Less liquidity

- Higher early withdrawal penalties

- Risk of missing higher rates if interest rates rise

Consider CD laddering to balance higher returns with liquidity needs.