Compound Interest Calculator

Wealth building • Exponential growth

Compound Interest Formula:

Show the calculatorFuture Value: \( FV = PV \times (1 + \frac{r}{n})^{nt} \)

Where:

- \( FV \) = Future Value

- \( PV \) = Present Value (initial investment)

- \( r \) = Annual interest rate (decimal)

- \( n \) = Number of times interest is compounded per year

- \( t \) = Number of years

This formula calculates the future value of an investment when interest is compounded multiple times per year. The more frequent the compounding, the greater the growth due to interest being earned on previously earned interest.

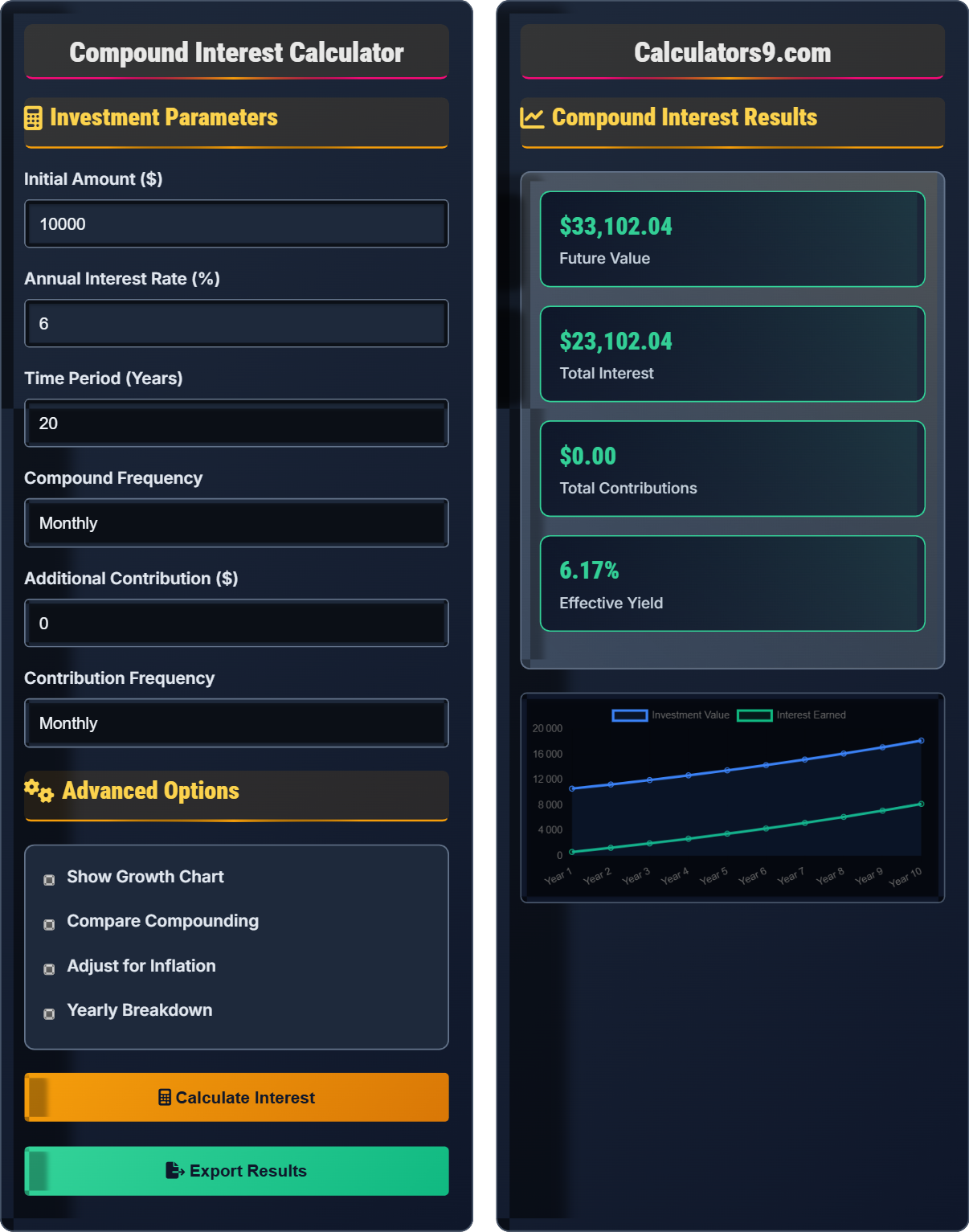

Example: For an initial investment of $10,000 at 6% annual interest compounded monthly over 20 years:

\( FV = 10,000 \times (1 + \frac{0.06}{12})^{12 \times 20} \)

\( FV = 10,000 \times (1.005)^{240} \approx \$33,102 \)

Thus, the investment would grow to approximately $33,102 after 20 years.

Investment Parameters

Advanced Options

Compound Interest Results

| Year | Balance | Interest Earned |

|---|

| Component | Amount | Percentage |

|---|

Comprehensive Compound Interest Guide

Compound interest is the interest calculated on the initial principal and also on the accumulated interest of previous periods. It's often called "interest on interest" and can cause wealth to grow exponentially over time. This is the fundamental principle behind long-term investment growth and retirement planning.

The standard compound interest calculation uses this formula:

Where:

- \(FV\) = Future Value

- \(PV\) = Present Value (initial investment)

- \(r\) = Annual interest rate (decimal)

- \(n\) = Number of times interest is compounded per year

- \(t\) = Number of years

Key advantages of compound interest include:

- Exponential Growth: Accelerates over time, generating increasingly larger returns

- Passive Income: Earnings generate more earnings without additional effort

- Wealth Building: Transforms modest investments into substantial sums over time

- Retirement Security: Creates substantial nest eggs for long-term financial security

- Financial Freedom: Enables achievement of long-term financial goals

- Take Advantage of Time: Start investing as early as possible to maximize compounding

- Reinvest Everything: Never withdraw interest earned; let it compound

- Choose Compounding Accounts: Select investments that compound interest frequently

- Make Regular Contributions: Add to investments consistently over time

- Stay Disciplined: Maintain long-term perspective and avoid premature withdrawals

Compound Interest Fundamentals

Interest earned on both principal and previously earned interest.

\(FV = PV \times (1 + \frac{r}{n})^{nt}\)

Where FV=future value, PV=initial investment, r=rate, n=frequency, t=time.

- Time is the most important factor in compound growth

- More frequent compounding increases returns

- Higher rates accelerate growth exponentially

Strategies

Money available today is worth more than the same amount later.

- Start investing as early as possible

- Choose investments with frequent compounding

- Reinvest all earnings automatically

- Make consistent contributions over time

- Compounding frequency matters

- Tax implications affect net returns

- Market volatility is normal

- Emergency fund is important

Compound Interest Learning Quiz

Which compounding frequency will result in the highest final amount for a $10,000 investment at 5% annual interest over 10 years?

The answer is D) Daily. The more frequent the compounding, the higher the final amount due to interest being calculated and added to the principal more often. Using the formula \(FV = PV \times (1 + \frac{r}{n})^{nt}\): - Daily: $10,000 × (1 + 0.05/365)^(365×10) = $16,486.65 - Quarterly: $10,000 × (1 + 0.05/4)^(4×10) = $16,436.19 - Semi-annually: $10,000 × (1 + 0.05/2)^(2×10) = $16,386.16 - Annually: $10,000 × (1 + 0.05/1)^(1×10) = $16,288.95

This demonstrates how compounding frequency affects growth. With daily compounding, interest is calculated and added to the principal every day, allowing that interest to earn more interest for the remaining days of the year. More frequent compounding creates more opportunities for interest to earn interest.

Compounding Frequency: How often interest is calculated and added to principal

Effective Annual Rate: Actual return earned when compounding is considered

Simple Interest: Interest calculated only on principal amount

• More frequent compounding results in higher returns

• The effect is more pronounced with higher rates and longer periods

• Daily compounding approaches continuous compounding mathematically

• Choose investments with higher compounding frequencies

• The difference between monthly and daily compounding is minimal

• Focus on rate and time more than frequency for significant gains

• Assuming annual compounding is equivalent to more frequent compounding

• Not considering compounding frequency when comparing investments

• Overestimating the impact of very frequent compounding

Calculate the future value of $5,000 invested at 4% annual interest compounded quarterly for 15 years. Show your work.

Using the compound interest formula: \(FV = PV \times (1 + \frac{r}{n})^{nt}\)

Given:

- PV = $5,000

- r = 0.04

- n = 4 (quarterly)

- t = 15

Step 1: Calculate rate per period: r/n = 0.04/4 = 0.01

Step 2: Calculate total periods: nt = 4 × 15 = 60

Step 3: Calculate (1 + r/n)^(nt) = (1.01)^60 = 1.8167

Step 4: Calculate FV = $5,000 × 1.8167 = $9,083.50

Therefore, the future value is approximately $9,083.50.

This calculation demonstrates how to properly apply the compound interest formula. The key is to divide the annual rate by the number of compounding periods per year and multiply the number of years by the same factor. This ensures the formula accounts for the actual compounding frequency.

Principal: Initial amount invested

Compounding Period: Interval at which interest is calculated

Future Value: Value of investment at a future date

• Always adjust rate and time for compounding frequency

• Rate per period = Annual rate ÷ Compounding frequency

• Total periods = Years × Compounding frequency

• Remember: r/n and n*t adjustments

• Use a calculator for complex exponent calculations

• Double-check your rate and time adjustments

• Forgetting to adjust the rate for compounding frequency

• Using the wrong number of periods in calculations

• Applying annual rate directly without dividing by frequency

Alex starts investing $1,000 at age 25 with a 7% annual return compounded annually. Jordan starts investing the same amount at age 35 with the same return. How much more will Alex have than Jordan at age 65? Show your calculations.

For Alex (40 years): FV = $1,000 × (1.07)^40 = $1,000 × 14.9745 = $14,974.50

For Jordan (30 years): FV = $1,000 × (1.07)^30 = $1,000 × 7.6123 = $7,612.30

Difference: $14,974.50 - $7,612.30 = $7,362.20

Therefore, Alex will have $7,362.20 more than Jordan despite investing the same amount.

This example vividly demonstrates the exponential power of compound interest over time. The 10 additional years of compounding resulted in Alex having nearly twice as much money as Jordan. This shows why starting early is often more important than investing larger amounts later.

Time Advantage: Extra years of compounding that benefit early investors

Exponential Growth: Growth that accelerates over time due to compounding

Investment Duration: Length of time money is invested

• Time has exponential impact on compound growth

• Starting early beats starting big in the long run

• Each additional year of compounding increases returns

• Start investing as soon as possible, even with small amounts

• The difference between starting at 25 vs 35 is significant by retirement

• Time compensates for lower returns in the long run

• Underestimating the impact of compound interest over time

• Believing that starting with a large amount is better than starting early

• Delaying investments in favor of other goals

You invest $10,000 at 6% annual interest compounded monthly for 20 years. If inflation averages 3% annually, what is the real value of your investment in today's dollars? (Hint: Calculate the future value, then adjust for inflation)

Step 1: Calculate future value with compound interest

FV = $10,000 × (1 + 0.06/12)^(12×20) = $10,000 × (1.005)^240 = $33,102

Step 2: Calculate the effect of inflation over 20 years

Inflation factor = (1.03)^20 = 1.8061

Step 3: Calculate real value in today's dollars

Real value = $33,102 ÷ 1.8061 = $18,334

Therefore, the real value of your investment in today's dollars is $18,334.

This example shows how inflation erodes purchasing power over time. While your investment grows to $33,102 in nominal terms, the real value (adjusted for inflation) is significantly lower at $18,334. This demonstrates why it's important to consider inflation when planning long-term investments and retirement goals.

Nominal Value: Value in current dollars without inflation adjustment

Real Value: Value adjusted for inflation

Purchasing Power: Amount of goods/services that can be bought with currency

• Nominal returns don't reflect actual purchasing power

• Real returns account for inflation impact

• High inflation can significantly reduce real returns

• Consider inflation when evaluating investment returns

• Aim for returns that exceed inflation rates

• Use inflation-protected securities for long-term planning

• Confusing nominal returns with real returns

• Not accounting for inflation in long-term projections

• Assuming that high nominal returns are always beneficial

According to the Rule of 72, how long will it take for an investment to double at 8% annual interest?

The answer is C) 9 years. The Rule of 72 states that the number of years to double an investment is approximately 72 divided by the annual interest rate. So 72 ÷ 8 = 9 years. This is a quick estimation method for compound interest calculations.

The Rule of 72 is a handy shortcut for estimating how long it takes for an investment to double. It's derived from the natural logarithm and works well for interest rates between 6% and 10%. For our example, using the exact formula: $1,000 × (1.08)^9 = $1,999, which is very close to doubling.

Rule of 72: Quick estimation method to calculate time to double investment

Approximation: Close estimate that simplifies complex calculations

Exponential Function: Mathematical function with variable in exponent

• Rule of 72 = 72 ÷ Interest Rate = Years to Double

• Most accurate for rates between 6% and 10%

• For lower rates, use Rule of 70; for higher rates, use Rule of 69

• Use Rule of 72 for quick mental calculations

• For 6% return: 72÷6 = 12 years to double

• For 9% return: 72÷9 = 8 years to double

• Applying Rule of 72 to extremely high or low interest rates

• Forgetting that it's an approximation, not exact

• Not understanding when to use Rule of 70 or 69

FAQ

Q: How does compound interest differ from simple interest?

A: Simple interest is calculated only on the principal amount, using the formula: \( SI = P \times r \times t \). Compound interest, however, is calculated on both the principal and accumulated interest, using the formula: \( FV = PV \times (1 + \frac{r}{n})^{nt} \).

For example, with $10,000 at 5% for 3 years:

- Simple interest: $10,000 × 0.05 × 3 = $1,500 total interest

- Compound interest: $10,000 × (1.05)^3 - $10,000 = $1,576.25 total interest

Compound interest generates higher returns because you earn interest on previously earned interest.

Q: How much difference does compounding frequency make?

A: Using the compound interest formula \( FV = PV \times (1 + \frac{r}{n})^{nt} \), let's examine a $10,000 investment at 6% over 20 years:

- Annually (n=1): $10,000 × (1.06)^20 = $32,071

- Monthly (n=12): $10,000 × (1.005)^240 = $33,102

- Daily (n=365): $10,000 × (1.000164)^7300 = $33,195

The difference between annual and monthly compounding is $1,031, while the difference between monthly and daily is only $93. More frequent compounding helps, but the impact diminishes at very high frequencies.