RMD Calculator

Fast distribution calculator • 2026 rates

RMD Calculation Formula:

Show the calculator\( \text{RMD} = \frac{\text{Account Balance}}{\text{Life Expectancy Factor}} \)

Where:

- \( \text{RMD} \) = Required Minimum Distribution

- \( \text{Account Balance} \) = Balance as of December 31st of previous year

- \( \text{Life Expectancy Factor} \) = Based on Uniform Lifetime Table

This formula calculates the minimum amount that must be withdrawn annually from tax-deferred retirement accounts.

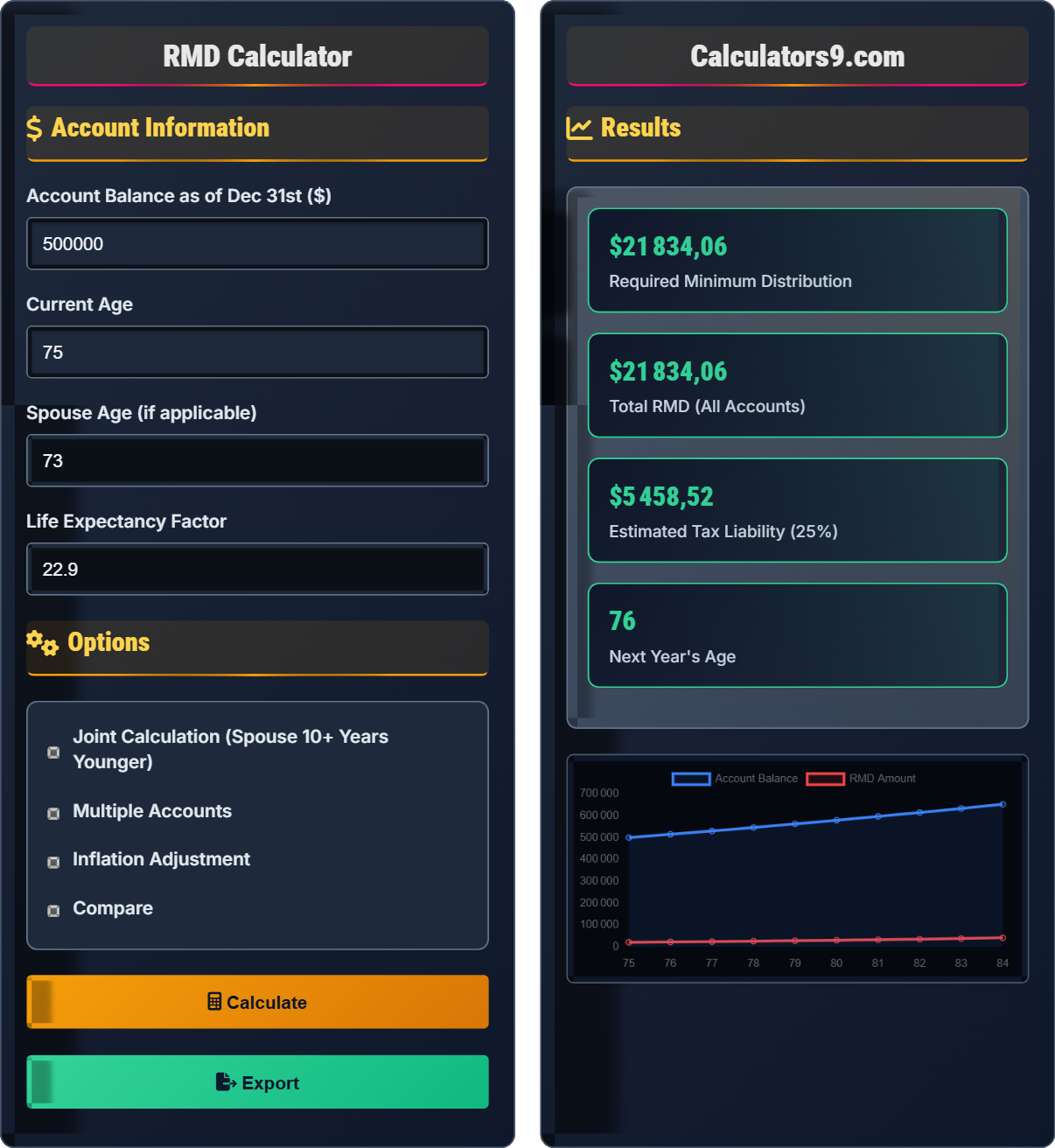

Example: For age 75 with account balance of \( \$500{,}000 \), life expectancy factor is 22.9:

\( \text{RMD} = \frac{\$500{,}000}{22.9} = \$21{,}834 \)

Thus, the account holder must withdraw at least $21,834 in the current year.

Account Information

Options

Results

| Year | Age | Balance | Factor | RMD |

|---|

Account Balance: $500,000

Life Expectancy Factor: 22.9

Calculation: $500,000 ÷ 22.9

RMD Amount: $21,834.06

Due Date: December 31, 2026

Penalty: 50% of unwithdrawn amount

First RMD Year: 2026

Calculation Method: Uniform Lifetime

Comprehensive RMD Guide

Required Minimum Distributions (RMDs) are mandatory withdrawals from tax-deferred retirement accounts that begin at age 73 (as of 2024). The purpose is to ensure that the government collects taxes on the tax-deferred money in these accounts. RMDs apply to Traditional IRAs, SEP IRAs, SIMPLE IRAs, and 401(k)s.

The standard RMD calculation uses the following formula:

Where:

- \( \text{Account Balance} \) = Balance as of December 31st of previous year

- \( \text{Life Expectancy Factor} \) = From the IRS Uniform Lifetime Table

The IRS provides life expectancy factors for RMD calculations:

- Age 70: Factor 27.4

- Age 75: Factor 22.9

- Age 80: Factor 18.7

- Age 85: Factor 14.8

- Age 90: Factor 11.4

Dec 31st Value

Investments

IRS Table

Age-Based

Taxable

Required

- Charitable Giving: Qualified Charitable Distributions (QCDs) can satisfy RMDs tax-free

- Tax Planning: Consider timing and tax bracket management

- Investment Selection: Hold tax-inefficient investments in tax-deferred accounts

- Roth Conversions: Convert Traditional to Roth to reduce future RMDs

- Withdrawal Timing: Take RMDs earlier in year to maximize tax planning

RMD Basics

Required withdrawals from tax-deferred retirement accounts.

\( \text{RMD} = \frac{\text{Account Balance}}{\text{Life Expectancy Factor}} \)

Where balance is as of Dec 31st previous year.

- Begin at age 73

- 50% penalty for missed RMDs

- Can aggregate from multiple accounts

Strategies

Strategies to minimize tax impact of RMDs.

- Consider Roth conversions

- Use QCDs for charitable giving

- Plan withdrawals strategically

- Manage tax brackets

- First RMD in year after turning 73

- Subsequent RMDs by Dec 31st

- Spousal exception available

- 401(k) rules may differ

RMD Learning Quiz

When must RMDs begin for someone who turns 73 in 2026?

The answer is B) April 1, 2027. According to the SECURE Act 2.0, RMDs must begin by April 1st of the year following the year you turn 73. For someone turning 73 in 2026, the first RMD is due by April 1, 2027. Subsequent RMDs must be taken by December 31st of each year.

Understanding RMD timing is crucial to avoid penalties. The first RMD has a special rule with a later deadline (April 1st), but this means you'll have two RMDs in the same tax year (the first one and the second one due by December 31st), which can impact your tax situation.

RMD: Required Minimum Distribution from tax-deferred accounts

SECURE Act: Legislation changing retirement rules

Excise Tax: 50% penalty for missed RMDs

• First RMD by April 1st following turning 73

• Subsequent RMDs by December 31st

• 50% penalty for missed RMDs

• Plan ahead for first RMD timing

• Set up automatic reminders

• Consider tax implications of two RMDs

• Confusing the timing of first RMD

• Forgetting about the two RMDs issue

• Missing deadlines leading to penalties

Calculate the RMD for a 75-year-old with a $600,000 IRA balance. Show your work.

Using the RMD formula: \( \text{RMD} = \frac{\text{Account Balance}}{\text{Life Expectancy Factor}} \)

From the Uniform Lifetime Table, age 75 has a factor of 22.9

Given:

- Account Balance = $600,000

- Life Expectancy Factor = 22.9

Step 1: Apply the formula

\( \text{RMD} = \frac{\$600{,}000}{22.9} = \$26{,}200.87 \)

This calculation shows how the IRS determines the minimum amount that must be withdrawn annually. The life expectancy factor decreases as you age, causing RMDs to increase over time. This ensures that the account is eventually depleted.

Life Expectancy Factor: From IRS Uniform Lifetime Table

Account Balance: As of December 31st of previous year

Uniform Lifetime Table: IRS table for RMD calculations

• Use previous year's December 31st balance

• Factor decreases with age

• RMDs increase as factor decreases

• Check IRS Publication 590-B for tables

• Calculate early in year

• Plan for tax implications

• Using current year's balance instead of previous year

• Using wrong life expectancy factor

• Forgetting about the spouse exception

Sarah has three Traditional IRAs with balances of $400,000, $300,000, and $200,000. She is 75 years old. Calculate her total RMD requirement. Can she take the entire amount from just one account?

Step 1: Calculate RMD for each account

For age 75, life expectancy factor = 22.9

Account 1 RMD: $400,000 ÷ 22.9 = $17,467.25

Account 2 RMD: $300,000 ÷ 22.9 = $13,100.44

Account 3 RMD: $200,000 ÷ 22.9 = $8,733.62

Step 2: Calculate total RMD

Total RMD: $17,467.25 + $13,100.44 + $8,733.62 = $39,301.31

Step 3: Determine withdrawal strategy

Yes, Sarah can take the total RMD amount of $39,301.31 from just one account, or any combination that equals the total. However, she must calculate the RMD for each account separately.

Therefore, Sarah's total RMD requirement is $39,301.31, and she can take it from any one account or combination of accounts.

This demonstrates the aggregation rule for Traditional IRAs. While RMDs must be calculated separately for each account, they can be taken from any one account or combination of accounts. This provides flexibility in tax planning and investment management.

Aggregation Rule: Ability to combine RMDs from multiple accounts

Separate Calculation: Each account requires individual RMD calculation

Flexibility: Can withdraw total from any account

• Calculate separately for each account

• Can aggregate withdrawals

• Does not apply to 401(k)s

• Withdraw from less volatile accounts

• Consider tax implications

• Track RMDs for each account

• Not understanding aggregation rules

• Confusing with 401(k) rules

• Failing to calculate separately

John is 78 years old with an IRA balance of $750,000. His spouse Mary is 66 years old and is the sole beneficiary. Calculate John's RMD using both the Uniform Lifetime Table and the Joint Life Expectancy Table. Which method results in a lower RMD?

Step 1: Calculate RMD using Uniform Lifetime Table

For age 78, life expectancy factor = 20.3

Uniform RMD: $750,000 ÷ 20.3 = $36,945.81

Step 2: Calculate RMD using Joint Life Expectancy Table

For age 78 with spouse age 66, joint factor = 25.5

Joint RMD: $750,000 ÷ 25.5 = $29,411.76

Step 3: Compare results

Difference: $36,945.81 - $29,411.76 = $7,534.05

Therefore, using the Joint Life Expectancy Table results in a lower RMD of $29,411.76, saving $7,534.05 compared to the Uniform Lifetime Table.

This demonstrates the spousal exception for RMDs. When your spouse is more than 10 years younger and is the sole beneficiary, you can use the Joint Life Expectancy Table, which typically results in lower RMDs. This recognizes the longer period over which the account will likely be distributed.

Spousal Exception: Special rule for younger spouses

Joint Life Table: Used when spouse is 10+ years younger

Sole Beneficiary: Only spouse named as beneficiary

• Spouse must be 10+ years younger

• Must be sole beneficiary

• Results in lower RMDs

• Check if spouse qualifies for exception

• Consider beneficiary designations

• Calculate both methods

• Not checking for spousal exception

• Forgetting about beneficiary requirements

• Using wrong table when eligible for exception

What is the penalty for failing to take a required minimum distribution?

The answer is C) 50% excise tax on the unwithdrawn amount. The penalty for failing to take an RMD is extremely severe - 50% of the amount that should have been withdrawn. This is one of the harshest penalties in the tax code, which is why it's crucial to understand and comply with RMD requirements.

The severe penalty for missed RMDs underscores their importance. The 50% excise tax is applied to the amount that should have been withdrawn but wasn't. This penalty can be waived if you can show reasonable cause for the failure, but it's better to avoid the situation entirely.

Excise Tax: Penalty tax for violations

Reasonable Cause: Justification for penalty waiver

Unwithdrawn Amount: RMD that was not taken

• 50% penalty on unwithdrawn amount

• Can be waived for reasonable cause

• Extremely harsh penalty

• Set up automatic reminders

• Calculate early in year

• Contact tax professional if missed

• Underestimating penalty severity

• Forgetting about RMD requirements

• Not tracking multiple accounts

FAQ

Q: How do I calculate RMDs for multiple retirement accounts?

A: For Traditional IRAs, SEP IRAs, and SIMPLE IRAs, you calculate RMDs separately for each account but can take the total from any one account or combination of accounts. Using the formula: \( \text{RMD} = \frac{\text{Balance}}{\text{Factor}} \), if you have $500,000 in one IRA and $300,000 in another (total $800,000) at age 75 (factor 22.9):

Individual RMDs: $500,000 ÷ 22.9 = $21,834; $300,000 ÷ 22.9 = $13,100

Total RMD: $21,834 + $13,100 = $34,934 (can be taken from any account)

For 401(k)s, RMDs must be taken from each plan separately.

Q: Can I use Qualified Charitable Distributions (QCDs) to satisfy my RMD?

A: Yes! QCDs allow you to transfer up to $100,000 per year directly from your IRA to a qualified charity, and this can count toward satisfying your RMD. The benefit is that the distribution is tax-free, unlike a regular RMD which is fully taxable as ordinary income. For example, if your RMD is $25,000 and you make a $25,000 QCD, you fulfill your RMD requirement tax-free. This is especially valuable for those who don't need the RMD income.