Simple Interest Calculator

Financial growth • Linear returns

Simple Interest Formula:

Show the calculatorSimple Interest: \( SI = P \times r \times t \)

Future Value: \( FV = P + SI = P(1 + rt) \)

Where:

- \( SI \) = Simple Interest

- \( FV \) = Future Value

- \( P \) = Principal (initial amount)

- \( r \) = Annual interest rate (decimal)

- \( t \) = Time in years

This formula calculates interest based only on the original principal amount, without compounding. Simple interest grows linearly over time, unlike compound interest which grows exponentially. It's commonly used for short-term loans, certificates of deposit, and certain investment products.

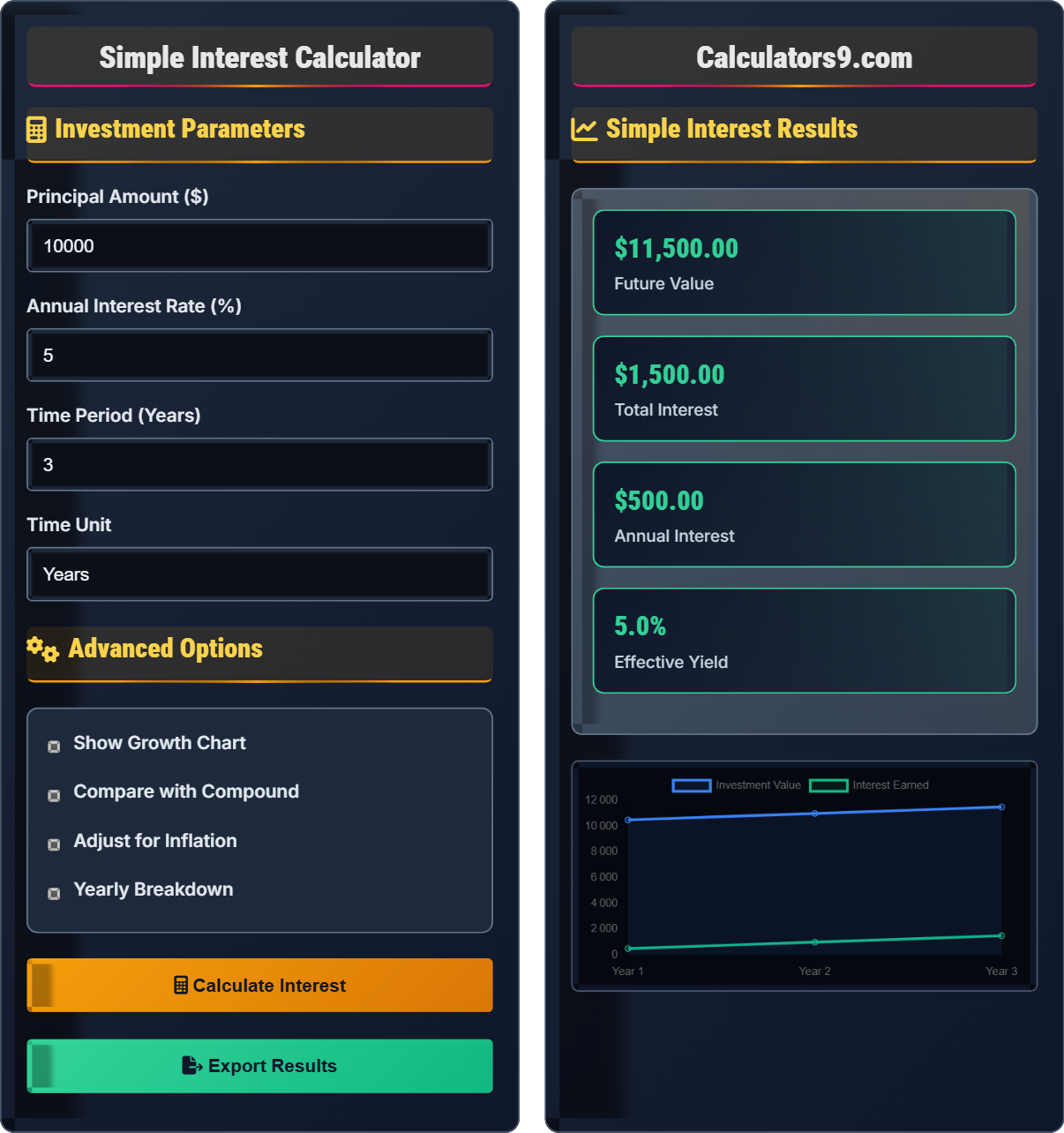

Example: For a principal of $10,000 at 5% annual interest for 3 years:

Simple Interest: \( SI = 10,000 \times 0.05 \times 3 = \$1,500 \)

Future Value: \( FV = 10,000 + 1,500 = \$11,500 \)

Thus, the investment would grow to $11,500 after 3 years.

Investment Parameters

Advanced Options

Simple Interest Results

| Year | Principal | Interest Earned | Total Value |

|---|

| Component | Amount | Percentage |

|---|

Comprehensive Simple Interest Guide

Simple interest is a method of calculating interest where the interest is computed only on the original principal amount. Unlike compound interest, simple interest does not earn interest on previously earned interest. It follows a linear growth pattern, making it easier to calculate and predict.

The standard simple interest calculation uses this formula:

Where:

- \(SI\) = Simple Interest

- \(P\) = Principal (initial amount)

- \(r\) = Annual interest rate (decimal)

- \(t\) = Time in years

Key differences between simple and compound interest:

- Growth Pattern: Simple interest grows linearly; compound grows exponentially

- Calculation: Simple uses only principal; compound uses principal + accumulated interest

- Benefit: Simple interest benefits borrowers; compound benefits investors

- Time Effect: Simple interest increases linearly with time; compound increases exponentially

- Complexity: Simple is easier to calculate and predict

- Short-term Goals: Simple interest may be suitable for short-term objectives

- Predictability: Simple interest offers more predictable returns

- Transparency: Easier to understand and verify calculations

- Early Payoff: Beneficial for loans with potential early payoff

- Comparison: Always compare with compound alternatives

Simple Interest Fundamentals

Interest calculated only on the original principal amount.

\(SI = P \times r \times t\)

Where SI=simple interest, P=principal, r=rate, t=time.

- Interest is calculated only on the principal

- Growth is linear over time

- Same amount of interest earned each period

Strategies

Consistent interest earned each period based only on principal.

- Understand when simple interest applies

- Compare with compound alternatives

- Consider short-term investment needs

- Verify calculation methods with institutions

- Lower returns than compound interest over time

- Good for short-term goals

- Easier to calculate and predict

- Beneficial for early loan payoffs

Simple Interest Learning Quiz

Which statement about simple interest is TRUE compared to compound interest?

The answer is C) Simple interest grows linearly over time. Simple interest is calculated only on the principal amount using the formula \(SI = P \times r \times t\), which results in a linear relationship between time and interest earned. For example, $1,000 at 5% simple interest earns $50 each year regardless of how many years pass.

This question distinguishes between simple and compound interest. Simple interest produces a straight-line growth pattern because the same amount of interest is earned each period. Compound interest, on the other hand, creates an exponential curve because interest is earned on both principal and previously earned interest.

Simple Interest: Interest calculated only on the original principal

Linear Growth: Consistent increase at a constant rate

Exponential Growth: Increasing rate of growth over time

• Simple interest = Principal × Rate × Time

• Interest is earned only on the original principal

• Growth rate remains constant over time

• Simple interest is easier to calculate than compound interest

• Use simple interest for short-term calculations

• Compound interest is better for long-term investments

• Confusing simple interest with compound interest calculations

• Assuming simple interest grows exponentially

• Thinking interest is calculated on previously earned interest

Calculate the simple interest and future value for $8,000 invested at 4.5% annual interest for 5 years. Show your work.

Using the simple interest formula: \(SI = P \times r \times t\)

Given:

- P = $8,000

- r = 4.5% = 0.045

- t = 5 years

Step 1: Calculate simple interest: SI = $8,000 × 0.045 × 5 = $1,800

Step 2: Calculate future value: FV = P + SI = $8,000 + $1,800 = $9,800

Therefore, the simple interest is $1,800 and the future value is $9,800.

This calculation demonstrates the straightforward nature of simple interest. Each year, $8,000 × 0.045 = $360 in interest is earned. Over 5 years, this totals $360 × 5 = $1,800. The simplicity of this calculation makes simple interest predictable and easy to verify.

Principal: Initial amount invested

Future Value: Value of investment at maturity

Annual Interest Rate: Rate of return per year

• Always convert percentage to decimal for calculations

• Simple interest is calculated only on the principal

• Future value equals principal plus interest earned

• Convert percentage to decimal: 4.5% = 0.045

• Simple interest per year = Principal × Rate

• Total simple interest = Annual interest × Number of years

• Forgetting to convert percentage to decimal

• Calculating interest on previously earned interest

• Adding interest to interest instead of principal

A car loan of $25,000 has a simple interest rate of 6% annually and a term of 4 years. What is the total amount to be repaid? How much interest will be paid?

Using the simple interest formula: \(SI = P \times r \times t\)

Given:

- P = $25,000

- r = 6% = 0.06

- t = 4 years

Step 1: Calculate simple interest: SI = $25,000 × 0.06 × 4 = $6,000

Step 2: Calculate total repayment: Total = Principal + Interest = $25,000 + $6,000 = $31,000

Therefore, the total amount to be repaid is $31,000, with $6,000 in interest.

This example shows how simple interest applies to loans. The borrower pays interest only on the original loan amount, not on accumulated interest. This makes simple interest loans more predictable for both borrowers and lenders, especially if the loan is paid off early.

Loan Principal: Original amount borrowed

Total Repayment: Principal plus all interest

Simple Interest Loan: Loan where interest is calculated only on principal

• Simple interest loans have predictable payment structures

• Simple interest loans benefit from early repayment

• Interest is calculated daily on the remaining principal

• Verify loan terms to confirm interest calculation method

• Assuming all loans use compound interest

• Not understanding how early payments affect interest

• Confusing simple interest with compound interest in loans

You have $10,000 to invest for 3 years. Option A offers 6% simple interest annually. Option B offers 5.5% compound interest annually. Which option provides a higher return? Show your calculations.

For Option A (Simple Interest):

SI = $10,000 × 0.06 × 3 = $1,800

FV = $10,000 + $1,800 = $11,800

For Option B (Compound Interest):

FV = $10,000 × (1.055)^3 = $10,000 × 1.1742 = $11,742

Difference: $11,800 - $11,742 = $58

Therefore, Option A with simple interest provides a higher return of $58.

This example shows that for short-term investments, simple interest with a slightly higher rate can sometimes outperform compound interest with a lower rate. However, as the time period extends, compound interest typically surpasses simple interest due to exponential growth.

Investment Return: Profit earned from an investment

Rate Comparison: Evaluating different investment options

Time Factor: Impact of investment duration on returns

• Higher simple interest rate can beat lower compound rate in short term

• Compound interest typically wins in long-term investments

• Always compare total returns, not just interest rates

• For short-term investments, higher simple interest rate may be better

• For long-term investments, compound interest usually wins

• Always calculate total returns when comparing options

• Assuming compound interest always beats simple interest

• Not considering the time factor in comparisons

• Focusing only on rates instead of total returns

If you invest $5,000 at 4% simple interest and want to earn $1,000 in interest, how long will it take?

Using the simple interest formula rearranged to solve for time: \(t = \frac{SI}{P \times r}\)

Given:

- SI = $1,000

- P = $5,000

- r = 4% = 0.04

Step 1: Calculate time: t = $1,000 / ($5,000 × 0.04) = $1,000 / $200 = 5 years

Therefore, it will take 5 years to earn $1,000 in interest.

This problem demonstrates how to rearrange the simple interest formula to solve for different variables. Since simple interest grows linearly, the relationship between time and interest earned is directly proportional. If you know three of the four variables (P, r, t, SI), you can always solve for the fourth.

Formula Rearrangement: Solving for different variables in equations

Proportional Relationship: Direct correlation between variables

Linear Relationship: Constant rate of change

• Simple interest formula can be rearranged to solve for any variable

• Time and interest have a direct proportional relationship

• The relationship remains linear regardless of variable values

• To find time: t = SI/(P×r)

• To find rate: r = SI/(P×t)

• To find principal: P = SI/(r×t)

• Incorrectly rearranging the simple interest formula

• Forgetting to convert percentages to decimals

• Misapplying compound interest formulas to simple interest problems

FAQ

Q: When is simple interest used instead of compound interest?

A: Simple interest is commonly used for short-term financial products where the compounding effect would be minimal. Examples include some certificates of deposit (CDs), car loans, personal loans, and promissory notes. The formula \( SI = P \times r \times t \) makes calculations straightforward and predictable.

For example, a $10,000 loan at 5% simple interest for 3 years would incur exactly $1,500 in interest ($10,000 × 0.05 × 3). This is easier to calculate and verify than compound interest, making it suitable for short-term obligations where transparency is valued.

Q: Is simple interest better than compound interest for investments?

A: Generally, compound interest is better for long-term investments due to exponential growth. Using the formulas:

- Simple Interest: \( FV = P(1 + rt) \)

- Compound Interest: \( FV = P(1 + r)^t \)

For example, $10,000 at 6% for 10 years:

- Simple: $10,000(1 + 0.06×10) = $16,000

- Compound: $10,000(1.06)^10 = $17,908

Compound interest yields $1,908 more. However, for very short-term investments, simple interest with a higher rate might be advantageous.