Down Payment Calculator

Maximize your savings • 2026 rates

Home Purchase Details

Advanced Options

Down Payment Analysis

| Item | Value | Details |

|---|---|---|

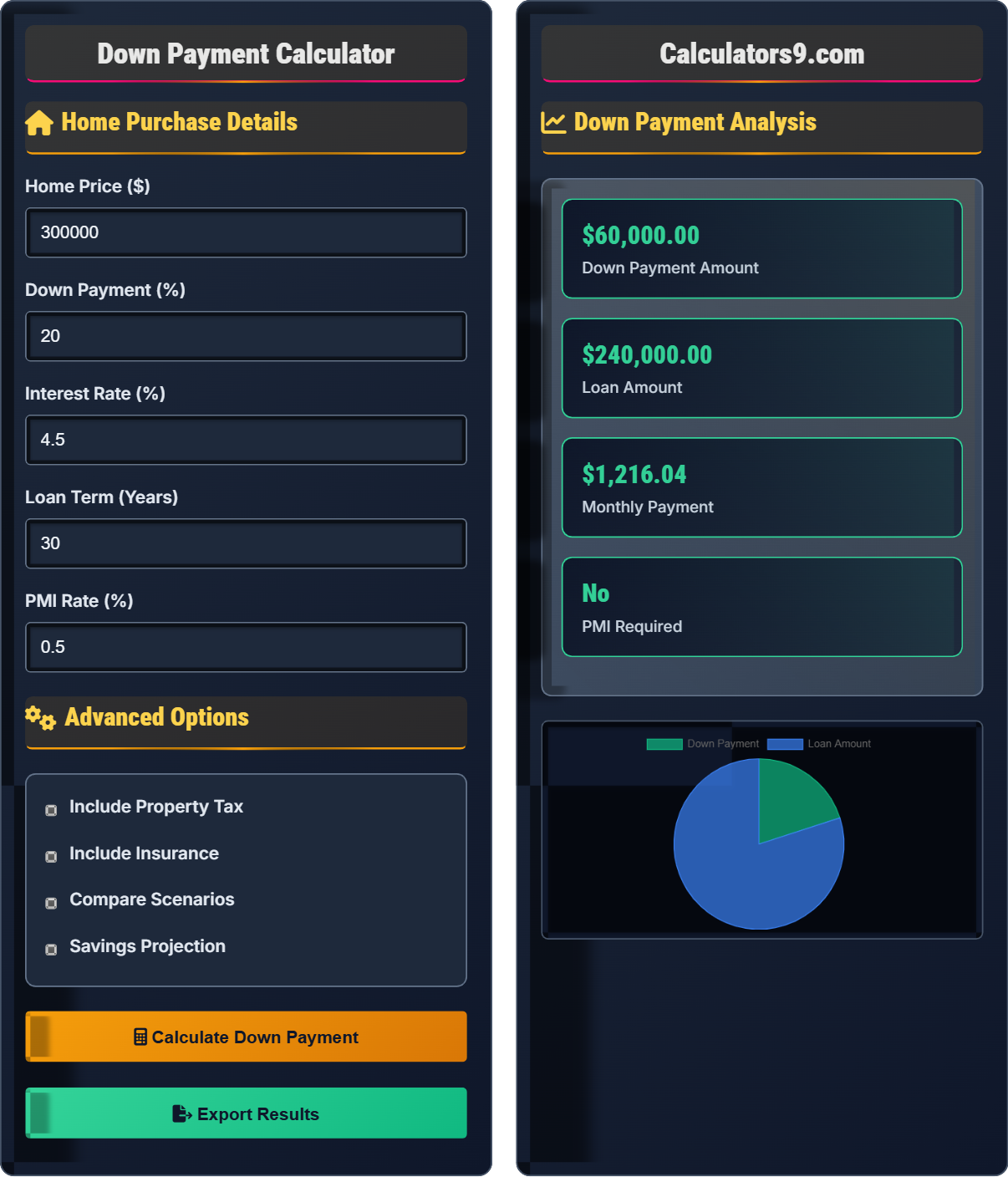

| Home Price | $300,000.00 | Base purchase price |

| Down Payment | $60,000.00 | 20.0% of home price |

| Loan Amount | $240,000.00 | Home price minus down payment |

| Monthly Payment | $1,216.04 | Principal + interest |

| PMI | $0.00 | Not required at 20% down |

| Down % | Down Amount | Loan Amount | Monthly Payment | PMI |

|---|

Comprehensive Down Payment Guide

A down payment is the portion of the home's purchase price that you pay upfront when obtaining a mortgage. It represents your initial investment in the property and affects your monthly payments, interest rate, and whether you need private mortgage insurance (PMI). The down payment is typically expressed as a percentage of the home's purchase price.

The basic down payment calculation is straightforward:

The loan amount is then calculated as:

Benefits of larger down payments include:

- Lower monthly payments

- Smaller loan amount

- No PMI requirement (at 20%+)

- Better interest rates

- Immediate equity in your home

- Stronger negotiating position

Drawbacks of large down payments:

- Reduced liquidity

- Opportunity cost of invested funds

- Longer saving period

- Missed investment opportunities

- Gift funds: Accept gifts from family members (up to 100% for some loan types)

- First-time buyer programs: State and local assistance programs

- Down payment savings plan: Set aside a fixed amount monthly

- Side hustles: Additional income streams for faster saving

- Windfalls: Tax refunds, bonuses, inheritance for down payment

Down Payment Learning Quiz

What is the minimum down payment required for a conventional loan if you're not a first-time buyer?

The answer is B) 5%. Conventional loans require a minimum of 3% down for first-time buyers and 5% for repeat buyers. However, putting 20% down eliminates the need for private mortgage insurance (PMI).

It's important to distinguish between minimum down payment requirements and optimal down payment amounts. While you can get a conventional loan with just 5% down, you'll typically need to pay PMI until your loan-to-value ratio drops below 80%.

Loan-to-Value Ratio (LTV): The ratio of the loan amount to the home's value

Private Mortgage Insurance (PMI): Insurance required when down payment is less than 20%

First-Time Buyer: Someone who hasn't owned a home in the past three years

• Minimum 3% down for first-time conventional buyers

• Minimum 5% down for repeat conventional buyers

• 20% down eliminates PMI requirement

• Consider first-time buyer programs if eligible

• Calculate PMI costs to determine optimal down payment

• Save extra to reach 20% threshold if possible

• Confusing minimum requirements with optimal amounts

• Not considering PMI costs when calculating expenses

• Assuming all loan types have the same requirements

If a home costs $400,000 and you plan to put down 15%, calculate the down payment amount and the loan amount. Show your work.

Down Payment Calculation:

Down Payment = Home Price × Down Payment %

Down Payment = $400,000 × 0.15 = $60,000

Loan Amount Calculation:

Loan Amount = Home Price - Down Payment

Loan Amount = $400,000 - $60,000 = $340,000

Your down payment would be $60,000 and your loan amount would be $340,000.

This simple calculation forms the foundation of all mortgage planning. Understanding the relationship between down payment percentage and loan amount helps buyers determine how much house they can afford and how much they need to save.

Down Payment: Initial payment made when purchasing property

Loan Amount: The portion of the purchase price financed by the lender

Principal: The original loan amount (excluding interest)

• Down payment = Home price × Down payment percentage

• Loan amount = Home price - Down payment

• Higher down payment = Lower loan amount

• Use 10% as a benchmark for conventional loans

• Calculate different scenarios to find optimal balance

• Consider opportunity cost of large down payments

• Forgetting to convert percentage to decimal

• Confusing down payment with closing costs

• Not considering the impact on monthly payments

Sarah is buying a $350,000 home and considering two down payment options: 10% or 20%. If the PMI rate is 0.5% of the loan amount annually, calculate the difference in total monthly payments including PMI. Assume the same interest rate and loan term for both scenarios.

Scenario 1 (10% down):

Down Payment = $350,000 × 0.10 = $35,000

Loan Amount = $350,000 - $35,000 = $315,000

PMI = $315,000 × 0.005 = $1,575 annually = $131.25 monthly

Scenario 2 (20% down):

Down Payment = $350,000 × 0.20 = $70,000

Loan Amount = $350,000 - $70,000 = $280,000

PMI = $0 (not required at 20% down)

Monthly payment difference (without PMI):

At 4.5% interest over 30 years: $1,591.66 (10%) vs $1,418.72 (20%) = $172.94 difference

Total monthly payment with PMI:

10% down: $1,591.66 + $131.25 = $1,722.91

20% down: $1,418.72 + $0 = $1,418.72

Difference: $1,722.91 - $1,418.72 = $304.19 monthly

By putting 20% down instead of 10%, Sarah saves $304.19 monthly.

This example demonstrates the hidden cost of low down payments. While the 10% down payment saves $35,000 upfront, Sarah pays an additional $304.19 monthly due to PMI. Over the life of a 30-year loan, this amounts to $110,000 in additional payments.

Private Mortgage Insurance (PMI): Insurance protecting the lender against default

Loan-to-Value Ratio (LTV): Loan amount divided by property value

Amortization: Gradual repayment of loan principal and interest

• PMI required when down payment is less than 20%

• PMI can be canceled when LTV reaches 80%

• PMI costs vary by loan type and credit score

• Calculate total cost including PMI when comparing scenarios

• Consider refinancing to remove PMI when equity builds

• Some lenders offer lender-paid PMI options

• Ignoring PMI costs in budget planning

• Not understanding when PMI can be removed

• Assuming PMI is permanent

Mike wants to buy a $275,000 home and aims for a 20% down payment. He currently has $15,000 saved and can save $800 per month. How many months will it take him to reach his down payment goal? What would his loan amount be?

Step 1: Calculate target down payment

Target Down Payment = $275,000 × 0.20 = $55,000

Step 2: Calculate amount still needed

Amount Needed = $55,000 - $15,000 = $40,000

Step 3: Calculate time needed to save

Time (months) = $40,000 ÷ $800 = 50 months

Step 4: Calculate loan amount

Loan Amount = $275,000 - $55,000 = $220,000

Mike will need 50 months (about 4 years) to save enough for a 20% down payment. His loan amount will be $220,000.

This problem demonstrates the practical aspect of down payment planning. It shows how to work backward from a goal to determine the timeline and how to calculate the resulting loan amount. This helps buyers set realistic expectations for their homebuying timeline.

Savings Timeline: The period required to accumulate necessary funds

Monthly Savings Rate: The amount saved per month toward a goal

Down Payment Goal: Target amount for initial home purchase payment

• Time = (Goal - Current) ÷ Monthly Savings

• Down payment goals should be realistic

• Consider adjusting timeline or goal based on savings capacity

• Increase monthly savings to shorten timeline

• Consider temporary side jobs to boost savings

• Look into down payment assistance programs

• Setting unrealistic savings timelines

• Not accounting for closing costs separately

• Forgetting about emergency fund needs

Which of the following is a valid consideration when deciding between investing excess funds or using them for a larger down payment?

The answer is D) All of the above. When deciding between investing excess funds or using them for a larger down payment, you should consider: A) Potential returns from investments - if investments return more than your mortgage rate, investing might be better; B) Interest rate on the mortgage - higher rates make paying down more attractive; C) Tax deductions for mortgage interest - these reduce the effective cost of borrowing.

This question highlights the complex decision-making involved in down payment planning. It's not just about maximizing the down payment, but finding the optimal balance between home equity, investment opportunities, and tax advantages. The decision depends on individual financial circumstances and market conditions.

Opportunity Cost: The potential return lost by choosing one option over another

Effective Interest Rate: Interest rate adjusted for tax benefits

Risk Tolerance: Willingness to accept uncertainty in investment returns

• Compare expected investment returns to mortgage rate

• Consider tax implications of both options

• Factor in personal risk tolerance

• If mortgage rate is higher than expected investment return, increase down payment

• Consider your time horizon for both investments and homeownership

• Factor in liquidity needs and emergency funds

• Only considering one factor in the decision

• Not accounting for tax benefits of homeownership

• Overlooking the impact of risk in investment comparisons

Down Payment Basics

Upfront payment when purchasing a home, typically 3-20% of purchase price.

Down Payment = Home Price × Down Payment %

Loan Amount = Home Price - Down Payment

- 20% down avoids PMI requirement

- Minimum 3-5% for conventional loans

- Higher down payments = lower monthly payments

Strategies

Set aside a fixed percentage of income monthly toward your down payment goal.

- Calculate target down payment

- Set monthly savings goal

- Research assistance programs

- Track progress regularly

- Keep emergency fund separate

- Consider opportunity cost

- Factor in closing costs

- Account for PMI if down <20%

FAQ

Q: Do I need 20% down to buy a house?

A: No, you can buy with as little as 3% down for conventional loans. But 20% avoids PMI, saving ~$100+/month on average.

Q: Should I invest or save for down payment?

A: Compare your mortgage rate to expected investment returns. If mortgage rate is 4.5% and you expect 6% investment return, invest. Otherwise, increase down payment.