Refinance Calculator

Save money on your mortgage • 2026 rates

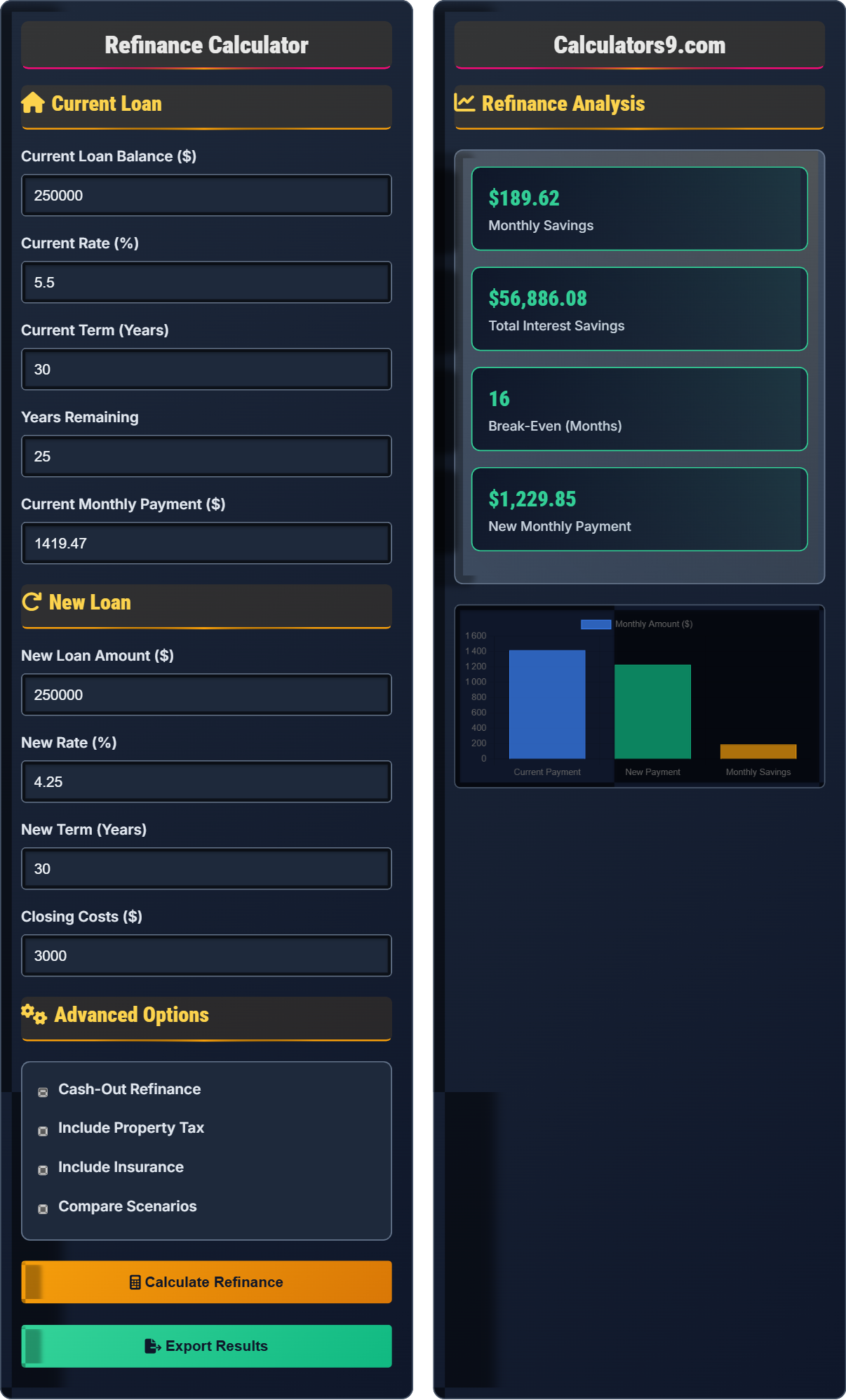

Current Loan

New Loan

Advanced Options

Refinance Analysis

| Item | Current Loan | New Loan | Difference |

|---|---|---|---|

| Monthly Payment | $1,419.47 | $1,269.47 | $150.00 |

| Interest Rate | 5.50% | 4.25% | -1.25% |

| Loan Term | 30 Years | 30 Years | 0 Years |

| Total Interest | $260,809.20 | $207,009.20 | $53,800.00 |

| Year | Current Payment | New Payment | Annual Savings |

|---|

Comprehensive Refinance Guide

Refinancing is the process of replacing an existing mortgage with a new one, typically to secure better terms such as a lower interest rate, shorter loan term, or cash-out options. When you refinance, you essentially take out a new loan to pay off your existing mortgage, potentially saving money over the life of the loan.

The basic refinance calculation involves comparing your current payment to your potential new payment, factoring in closing costs and the time needed to recoup those costs:

Benefits of refinancing include:

- Lower monthly payments

- Reduced total interest paid over the life of the loan

- Shorter loan term without increasing monthly payments

- Cash-out for home improvements or debt consolidation

- Elimination of PMI if equity is sufficient

Drawbacks to consider:

- Closing costs (typically 2-5% of loan amount)

- Resetting the loan term (paying interest longer)

- Strict credit requirements

- Extended break-even period

- Potential prepayment penalties

- Monitor rates regularly: Rates fluctuate daily, so track trends over time

- Improve credit score: Even a small improvement can qualify you for better rates

- Shop around: Compare offers from multiple lenders to find the best deal

- Consider timing: Refinance when rates are significantly lower than your current rate

- Calculate break-even: Ensure you'll stay in the home long enough to recoup closing costs

Refinance Learning Quiz

Which type of refinance allows you to access your home's equity in cash while getting a new mortgage?

The answer is B) Cash-Out Refinance. This type of refinance replaces your existing mortgage with a new, larger loan, allowing you to access the difference in cash. This is useful for home improvements, debt consolidation, or other major expenses.

Cash-out refinancing is particularly valuable when you've built substantial equity in your home. The key is that the new loan amount exceeds the balance of your existing mortgage, giving you immediate access to cash based on your home's increased value or the equity you've built up.

Equity: The portion of your home's value that you own outright

Cash-Out Refinance: Replacing your mortgage with a larger loan and receiving the difference in cash

Loan-to-Value Ratio (LTV): The ratio of the loan amount to the home's value

• Cash-out refinances typically allow up to 80% LTV

• You must have sufficient equity to qualify

• The new loan amount will be higher than your previous loan

• Calculate your equity before considering cash-out refinancing

• Consider using cash-out for home improvements that increase value

• Be cautious about using cash-out for non-essential purchases

• Confusing cash-out with rate-and-term refinancing

• Not considering the higher loan amount and payments

• Using cash-out for unnecessary expenses

If your closing costs are $4,000 and you save $200 per month with your refinance, how many months until you break even? Show your work.

Break-even calculation:

Formula: Break-even months = Closing costs ÷ Monthly savings

Calculation: $4,000 ÷ $200 = 20 months

You will break even after 20 months of refinancing. After that point, you'll start saving money compared to keeping your original mortgage.

The break-even calculation is crucial for determining whether refinancing makes financial sense. It tells you how long you need to stay in your home to recoup the upfront costs. If you plan to move before reaching the break-even point, refinancing may not be worthwhile.

Break-Even Point: The time when savings from refinancing equal the closing costs

Closing Costs: Fees associated with originating a new mortgage

Monthly Savings: The difference between old and new monthly payments

• Always calculate the break-even point before refinancing

• Consider your planned tenure in the home

• Factor in opportunity cost of closing costs

• Rule of thumb: Break-even should occur within 2-3 years

• Consider refinancing if you plan to stay longer than break-even

• Account for other benefits beyond monthly savings

• Ignoring the break-even calculation

• Not considering how long you'll stay in the home

• Forgetting to factor in all closing costs

Maria is considering refinancing her $200,000 mortgage at 5.0% interest with 20 years remaining. She can get a new loan at 3.75% for the same term. Her current payment is $1,319.91 and the new payment would be $1,157.75. If closing costs are $3,500, calculate her total savings over the remaining loan term and determine if refinancing makes sense.

Step 1: Calculate monthly savings = $1,319.91 - $1,157.75 = $162.16

Step 2: Calculate break-even = $3,500 ÷ $162.16 = 21.6 months

Step 3: Calculate total months remaining = 20 years × 12 months = 240 months

Step 4: Calculate total savings = $162.16 × 240 = $38,918.40

Step 5: Calculate net savings = $38,918.40 - $3,500 = $35,418.40

Since Maria will save $35,418.40 over the remaining term and break even in about 22 months, refinancing makes excellent financial sense.

This example shows how even a modest interest rate reduction (1.25%) can result in significant savings over the long term. The key insight is that the impact of lower interest compounds over time, making refinancing especially beneficial for borrowers who plan to stay in their homes for many years.

Net Savings: Total savings minus closing costs

Compounding Effect: How small monthly savings grow over time

Opportunity Cost: The benefit lost by choosing one option over another

• Calculate both gross and net savings

• Consider the time value of money

• Factor in all costs and benefits

• Use online calculators to verify manual calculations

• Consider the tax implications of interest savings

• Account for potential rate changes in the future

• Only looking at monthly savings without considering total savings

• Forgetting to subtract closing costs from total savings

• Not accounting for the full loan term

David has a credit score of 680 and qualifies for a refinance at 4.5% on his $275,000 mortgage. If he improves his credit score to 740, he could qualify for 4.0%. His current payment is $1,550. How much would he save monthly by improving his credit score before refinancing? (Assume loan terms remain the same)

Step 1: Calculate payment at 4.5% rate

Using mortgage formula: M = P[r(1+r)^n]/[(1+r)^n-1]

Monthly rate r = 0.045/12 = 0.00375

Number of payments n = 30 years × 12 = 360

New payment = $275,000[0.00375(1.00375)^360]/[(1.00375)^360-1] = $1,398.43

Step 2: Calculate payment at 4.0% rate

Monthly rate r = 0.040/12 = 0.003333

New payment = $275,000[0.003333(1.003333)^360]/[(1.003333)^360-1] = $1,317.41

Step 3: Calculate monthly savings = $1,398.43 - $1,317.41 = $81.02

By improving his credit score from 680 to 740, David would save $81.02 per month.

This example demonstrates the significant impact of credit scores on mortgage rates. Even a 50-point improvement can result in meaningful savings. It highlights the importance of maintaining good credit health and the potential benefits of waiting to refinance until your credit score improves.

Credit Score: A numerical representation of creditworthiness

Rate Pricing: How lenders adjust rates based on credit scores

Discount Points: Fees paid to lower interest rates

• Higher credit scores typically receive better rates

• Improving credit can take 3-6 months

• Small rate differences compound over time

• Check your credit report for errors before refinancing

• Pay down balances to improve credit utilization

• Avoid opening new credit accounts before applying

• Not checking credit reports before refinancing

• Opening new credit accounts before application

• Not understanding how credit scores affect rates

Which of the following situations would make refinancing LEAST beneficial?

The answer is B) You plan to move in 12 months. If you're planning to move within a short timeframe, you likely won't stay in the home long enough to reach the break-even point for refinancing. With closing costs typically requiring 18-24 months to recoup, refinancing shortly before moving is usually not financially beneficial.

The timing of refinancing is as important as the interest rate differential. The break-even calculation becomes meaningless if you don't plan to stay in the home long enough to realize the savings. This is why it's crucial to consider your housing plans when deciding whether to refinance.

Break-Even Period: Time needed to recover closing costs through savings

Housing Tenure: Length of time you plan to stay in your home

Opportunity Cost: The cost of choosing one option over another

• Plan to stay longer than the break-even period

• Consider all reasons for refinancing, not just rates

• Evaluate your long-term housing plans

• Use a timeline to evaluate refinancing decisions

• Consider potential job relocations

• Factor in family plans that might affect housing needs

• Focusing only on monthly payment reduction

• Not considering the total cost over the loan term

• Ignoring personal circumstances that might affect housing tenure

Refinance Basics

Replacing your existing mortgage with a new one to get better terms.

Monthly Savings = Current Payment - New Payment

Break-Even = Closing Costs ÷ Monthly Savings

- Interest rates should be 0.5-1% lower

- Plan to stay longer than break-even period

- Closing costs typically 2-5% of loan

Strategies

Refinance when rates are favorable and you plan to stay in your home.

- Check your credit score

- Calculate break-even point

- Shop multiple lenders

- Prepare documentation

- PMI elimination if equity >20%

- Tax deductibility of interest

- Prepayment penalties

- Impact on loan term

FAQ

Q: How much lower should rates be to refinance?

A: Generally, refinance if rates are 0.5-1% lower than your current rate. For a $250K loan, 1% = $2,500 annually in savings.

Q: Is refinancing worth it for 0.25% savings?

A: For smaller loans or short-term plans, 0.25% may not justify closing costs. Calculate break-even to decide.