VA Mortgage Calculator

Calculate your VA mortgage payment • 2026 rates

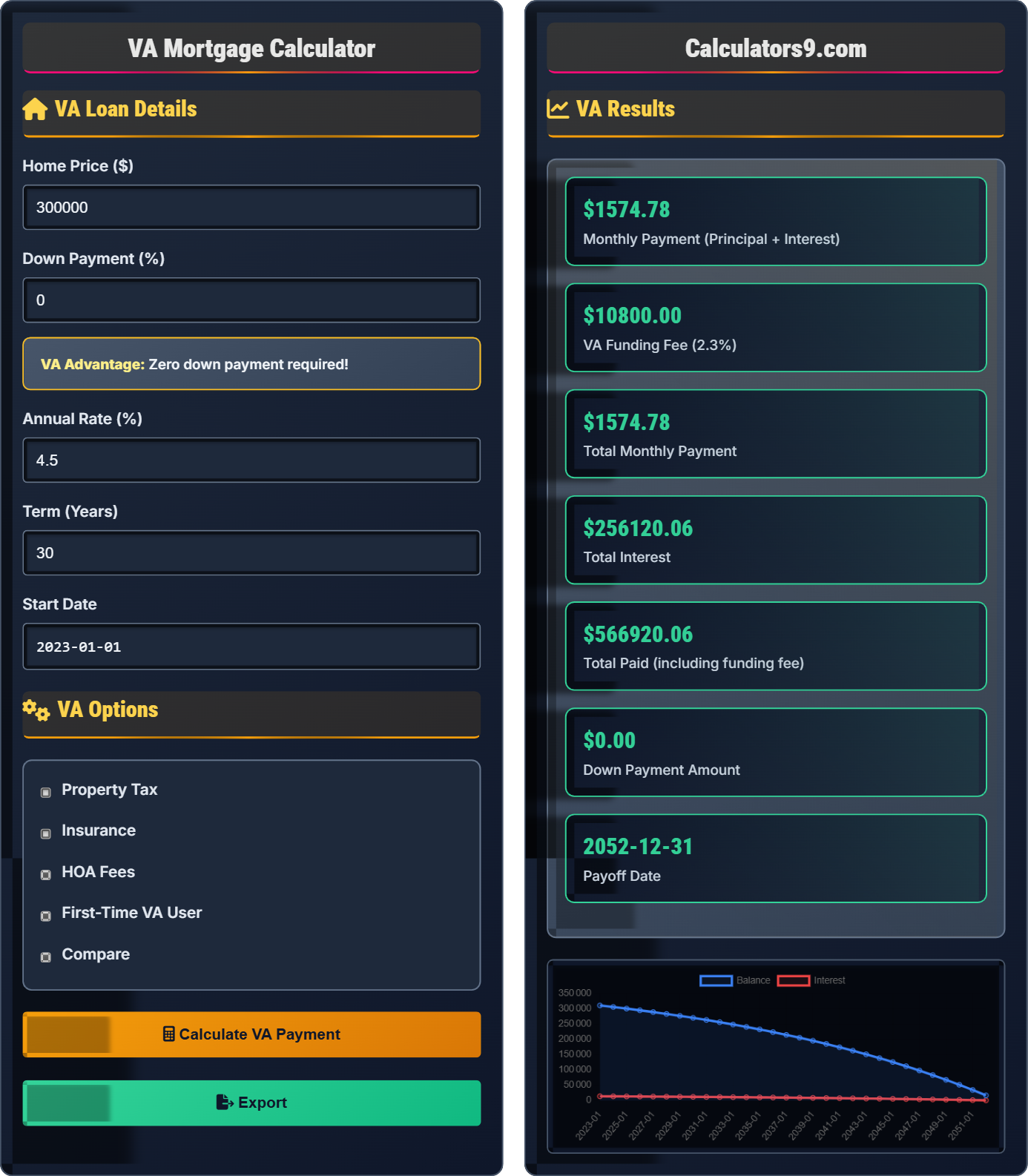

VA Loan Details

VA Options

VA Results

| Month | Payment | Principal | Interest | Balance |

|---|

| Year | Total | Principal | Interest | Balance |

|---|

Comprehensive VA Loan Guide

A VA loan is a mortgage guaranteed by the U.S. Department of Veterans Affairs (VA). These loans are available to eligible military service members, veterans, and surviving spouses. VA loans offer significant benefits including zero down payment requirements, no private mortgage insurance (PMI), and competitive interest rates.

The VA mortgage payment calculation is straightforward since there's no PMI:

Note: There is a one-time VA Funding Fee (typically 2.3% for first-time users) that can be financed into the loan amount.

VA loans offer unique advantages compared to conventional loans:

- Zero Down Payment: No down payment required

- No PMI: No private mortgage insurance required

- Competitive Rates: Often lower interest rates than conventional loans

- Assumable: Can transfer loan to qualified buyer

- Refinancing Options: VA streamline refinance available

The VA funding fee varies based on service history and loan type:

- First-time users: 2.3% of loan amount

- Subsequent users: 3.6% of loan amount

- Disabled veterans: Exempt from funding fee

- Surviving spouses: May be exempt from funding fee

VA Loan Learning Quiz

What is the minimum down payment required for a VA loan?

The answer is A) 0%. VA loans require zero down payment for eligible veterans and service members. This is one of the primary benefits of the VA loan program, making homeownership more accessible to military families.

The zero down payment feature of VA loans is possible because the VA guarantees a portion of the loan to the lender, reducing their risk. This guarantee allows lenders to offer loans without requiring a down payment, unlike conventional loans which typically require 20% down to avoid PMI.

Down Payment: The percentage of the home's purchase price paid upfront

VA Guarantee: The VA's promise to repay a portion of the loan if the borrower defaults

Lender Risk: The possibility of losing money on a loan

• VA loans require 0% down payment

• No PMI required with VA loans

• VA guarantee protects lenders from losses

• Save for closing costs since no down payment is required

• Research all associated costs beyond down payment

• Verify your VA eligibility before house hunting

• Assuming no costs are required with VA loans

• Not budgeting for closing costs

• Confusing VA requirements with conventional loan requirements

Explain the VA funding fee and calculate it for a $250,000 loan for a first-time user.

The VA funding fee is a one-time charge that helps offset the cost of the VA loan program. For first-time users, the funding fee is 2.3% of the loan amount.

Calculation: $250,000 × 2.3% = $5,750

The funding fee can be financed into the loan amount, increasing the total loan amount and monthly payment.

The funding fee compensates the government for the risk it takes by guaranteeing VA loans. First-time users pay 2.3%, while subsequent users pay 3.6%. Disabled veterans and surviving spouses may be exempt from this fee entirely.

VA Funding Fee: One-time fee charged by the VA to fund the loan program

First-Time User: Someone who has never used VA loan benefits before

Financed Fee: Adding the fee to the loan amount instead of paying upfront

• First-time users: 2.3% funding fee

• Subsequent users: 3.6% funding fee

• Disabled veterans: Exempt from funding fee

• Consider financing the fee to preserve cash flow

• Verify exemption status if disabled veteran

• Factor funding fee into total loan amount

• Forgetting to account for the funding fee

• Assuming all veterans are exempt from funding fee

• Not comparing total costs including funding fee

Michael is a first-time VA loan user with an honorable discharge after serving 181 days on active duty during peacetime. He wants to buy a $320,000 home with zero down payment. What is his total funding fee, and what would his monthly payment be at a 4.5% interest rate?

Step 1: Calculate funding fee = $320,000 × 2.3% = $7,360

Step 2: Calculate loan amount including funding fee = $320,000 + $7,360 = $327,360

Step 3: Calculate monthly payment for 30-year loan at 4.5% = $1,659.52

Therefore, Michael's total funding fee is $7,360 and his monthly payment would be $1,659.52.

This example demonstrates how the funding fee increases the total loan amount, which in turn affects the monthly payment. Michael qualifies for the first-time user rate of 2.3% funding fee based on his service record.

Loan Amount: The amount borrowed after down payment

Qualification: Meeting the lender's requirements for approval

Active Duty: Full-time military service

• Zero down payment allowed with VA loans

• Funding fee can be financed into loan

• First-time users pay 2.3% funding fee

• Consider financing funding fee to preserve cash

• Compare total costs including funding fee

• Verify service requirements for eligibility

• Only considering down payment and forgetting funding fee

• Not accounting for total loan amount with funded fee

• Confusing service requirements with eligibility

Sarah is considering a VA loan versus a conventional loan for a $300,000 home. With VA, she can put 0% down and pay a 2.3% funding fee ($6,900). With conventional, she would need 20% down ($60,000) but no PMI. Both loans have 4.5% interest rates. Compare the upfront costs and monthly payments. Which option might be better?

VA Loan:

- Down payment: $0

- Funding fee: $6,900

- Loan amount: $306,900

- Monthly payment: $1,552

- Upfront cost: $6,900

Conventional Loan:

- Down payment: $60,000

- Loan amount: $240,000

- Monthly payment: $1,216

- Upfront cost: $60,000

Sarah saves $336 monthly with VA but pays $53,100 less upfront with conventional. The choice depends on her cash availability and long-term plans.

This comparison highlights the trade-offs between VA and conventional loans. VA loans offer lower upfront costs but potentially higher monthly payments due to the funded fee. Conventional loans require larger down payments but have lower monthly payments. The decision depends on the borrower's financial situation and preferences.

Trade-off: Balancing different benefits and costs

PMI (Private Mortgage Insurance): Required for conventional loans with less than 20% down

Cash Flow: Monthly income vs expenses

• Lower upfront costs = higher ongoing costs

• Higher upfront costs = lower monthly payments

• Consider total cost over loan term

• Use VA for limited cash situations

• Choose conventional if you have 20% down

• Calculate total cost difference over time

• Focusing only on monthly payment and ignoring upfront costs

• Not considering total loan costs over time

• Assuming VA is always cheaper than conventional

Which of the following is NOT a limitation of VA loans?

The answer is B) Require mandatory mortgage insurance. VA loans do NOT require mortgage insurance (PMI). This is actually one of the key benefits of VA loans - they offer zero down payment without requiring mortgage insurance, unlike conventional loans.

VA loans eliminate the need for PMI because the VA guarantee provides protection for the lender. This is a significant advantage over conventional loans, which require PMI for loans with less than 20% down payment.

PMI (Private Mortgage Insurance): Insurance required on conventional loans with less than 20% down

VA Guarantee: Government guarantee replacing need for PMI

Loan Limits: Maximum loan amounts allowed by program

• VA loans are for primary residences only

• No PMI required with VA loans

• County-specific loan limits apply

• Limited to eligible military personnel

• Verify VA eligibility before applying

• Check local VA loan limits

• Compare VA benefits to other loan types

• Assuming VA loans require PMI like conventional loans

• Expecting higher loan limits than conventional

• Not verifying property meets VA requirements

VA Loan Basics

Department of Veterans Affairs-guaranteed loan with zero down payment.

\(\text{Total Payment} = \text{Principal + Interest}\)

No PMI required with VA loans!

- Zero down payment required

- No private mortgage insurance

- Primary residence only

VA Strategies

2.3% for first-time users, can be financed into loan amount.

- Verify disability status for fee exemption

- Consider USDA loans for rural areas

- Look for state veterans programs

- Explore VA streamline refinance options

- Eligibility requirements apply

- One-time funding fee applies

- Only for primary residences

- County loan limits apply

FAQ

Q: Do I need to pay PMI with a VA loan?

A: No, VA loans do not require private mortgage insurance (PMI). This is one of the key benefits of VA loans.

Q: Can I use VA for investment property?

A: No, VA loans are for primary residences only. Investment properties require conventional financing.