Business Loan Calculator

Fast payment calculator • 2026 rates

Business Loan Payment Formula:

Show the calculator\( M = P \frac{r(1+r)^n}{(1+r)^n - 1} \)

Where:

- \( M \) = monthly payment

- \( P \) = loan principal (total loan amount)

- \( r \) = monthly interest rate (annual rate divided by 12, in decimal form)

- \( n \) = total number of monthly payments (loan term in years × 12)

This formula calculates the fixed monthly payment required to fully pay off a business loan over the loan term, taking into account compound interest.

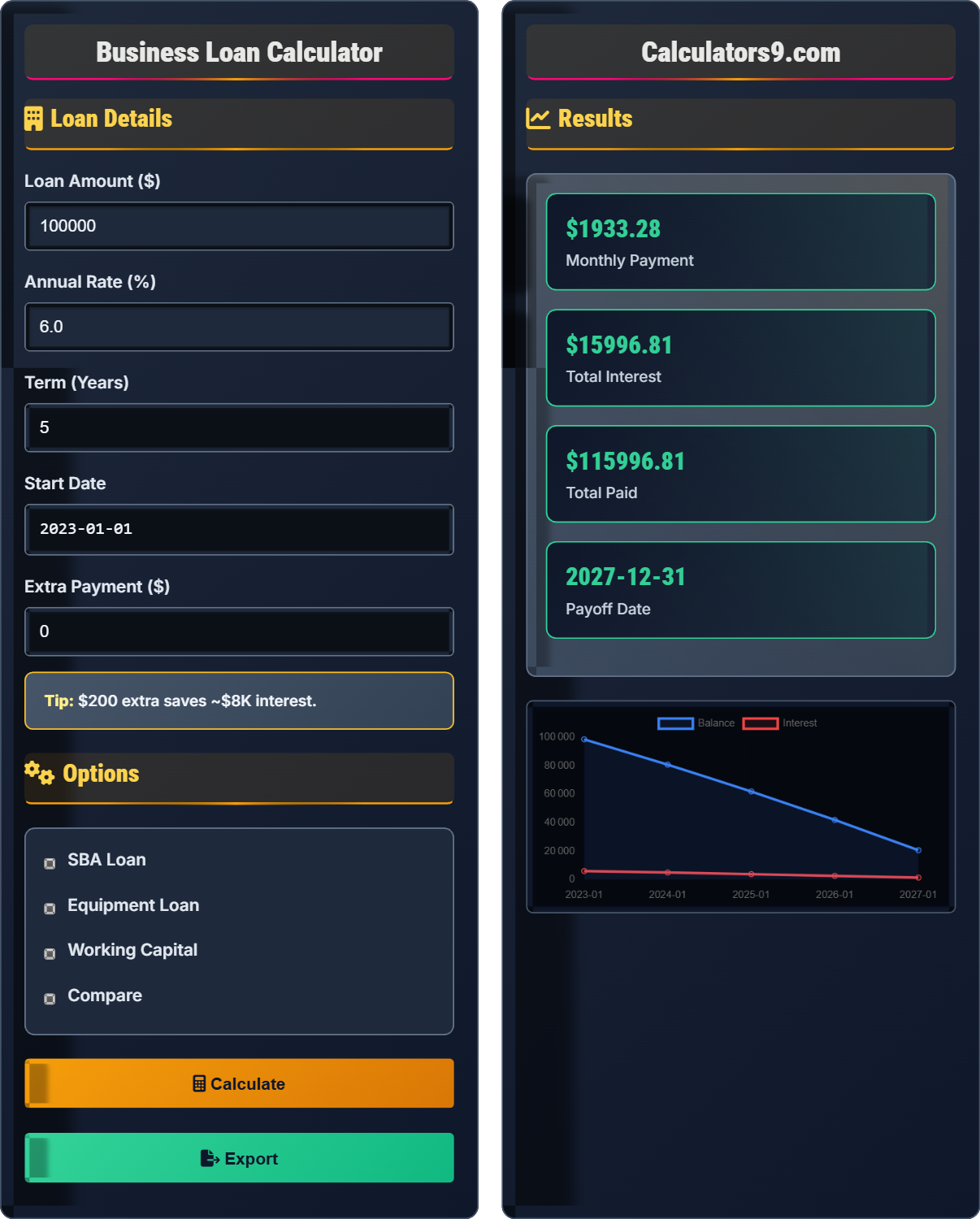

Example: For a loan of \( P = \$100{,}000 \) at an annual interest rate of 6.0% over 5 years:

Monthly interest rate: \( r = \frac{6.0\%}{12} = 0.005 \)

Total payments: \( n = 5 \times 12 = 60 \)

Monthly payment:

\( M = 100{,}000 \times \frac{0.005(1+0.005)^{60}}{(1+0.005)^{60} - 1} \approx \$1{,}933 \)

Thus, the borrower would pay approximately $1,933 per month for 5 years.

Loan Details

Options

Results

| Month | Payment | Principal | Interest | Balance |

|---|

| Year | Total | Principal | Interest | Balance |

|---|

Comprehensive Business Loan Guide

A business loan is a financial product designed to provide funding for business operations, expansion, equipment purchases, inventory, or other business-related expenses. Unlike personal loans, business loans are typically secured by business assets or guaranteed by business owners, and come with specific terms tailored to business cash flow patterns.

The standard business loan payment calculation uses the following formula:

Where:

- \(M\) = Monthly payment

- \(P\) = Principal loan amount

- \(r\) = Monthly interest rate (annual rate divided by 12)

- \(n\) = Total number of payments (loan term in years multiplied by 12)

Your monthly business loan payment typically includes:

- Principal: Portion that reduces the outstanding loan balance

- Interest: Cost of borrowing money, paid to the lender

- SBA Guarantee Fee: For SBA loans, a fee for the government guarantee

- Collateral Insurance: Insurance on business assets securing the loan

Revenue

Cash Flow

Credit Score

Collateral

Monthly Payments

Business Growth

- Improve credit score: Higher scores qualify for better rates and terms

- Prepare documentation: Financial statements, tax returns, business plan

- Consider SBA programs: More favorable terms for qualifying businesses

- Match loan term to asset life: Equipment loans should match equipment lifespan

- Plan for seasonal fluctuations: Some lenders offer payment holidays

Business Loan Basics

Loan for business purposes with business as collateral.

\(M = P\frac{r(1+r)^n}{(1+r)^n-1}\)

Where M=monthly payment, P=loan amount, r=monthly rate, n=payments.

- Interest calculated on remaining balance

- Business cash flow affects approval

- SBA loans have special terms

Strategies

Align loan payments with business revenue cycles.

- Match payments to revenue cycles

- Consider seasonal adjustments

- Plan for growth financing

- Use excess cash for extra payments

- Personal guarantees often required

- Business tax deductibility

- Prepayment penalties vary

- APR vs interest rate matters

Business Loan Learning Quiz

Which of the following is NOT typically required for business loan approval?

The answer is C) College Degree. While a business plan, personal credit score, and financial statements are standard requirements for business loan approval, having a college degree is not typically required. Lenders focus on business viability, creditworthiness, and collateral rather than educational background.

Understanding loan requirements is crucial for business owners seeking financing. Lenders evaluate risk based on business performance, owner credit history, and available collateral. Educational credentials are not a standard factor in loan underwriting, though some business experience may be beneficial.

Business Plan: Document outlining business strategy, market analysis, and financial projections

Personal Credit Score: Credit rating of business owner affecting loan terms

Financial Statements: Documents showing business financial health (P&L, Balance Sheet)

• Business financial health is primary factor

• Personal credit affects terms significantly

• Collateral requirements vary by loan type

• Prepare comprehensive business plan

• Maintain good personal credit score

• Organize financial documents in advance

• Assuming education level affects approval

• Not preparing adequate documentation

• Neglecting personal credit maintenance

Calculate the monthly payment for a $150,000 business loan at 5.5% annual interest over 7 years. Show your work.

Using the business loan formula: \(M = P\frac{r(1+r)^n}{(1+r)^n-1}\)

Given:

- P = $150,000

- r = 0.055 ÷ 12 = 0.004583

- n = 7 × 12 = 84

Step 1: Calculate (1+r)^n = (1.004583)^84 = 1.4668

Step 2: Calculate numerator: r(1+r)^n = 0.004583 × 1.4668 = 0.006721

Step 3: Calculate denominator: (1+r)^n - 1 = 1.4668 - 1 = 0.4668

Step 4: Calculate M = P × (numerator/denominator) = $150,000 × (0.006721/0.4668) = $150,000 × 0.01440 = $2,160.00

This problem demonstrates the calculation of business loan payments using the standard amortization formula. The monthly payment remains constant over the loan term, but the proportion of principal versus interest changes each month. Early payments are mostly interest, while later payments are mostly principal.

Amortization: Gradual repayment of loan through regular payments

Monthly Rate: Annual interest rate divided by 12

Number of Payments: Loan term in years multiplied by 12

• Always convert annual rates to monthly rates for calculations

• Convert loan terms to months for accurate calculations

• The loan formula accounts for compound interest over time

• Remember: r = annual rate ÷ 12

• Remember: n = loan years × 12

• Use a calculator for complex exponent calculations

• Forgetting to convert annual rates to monthly rates

• Using the wrong number of payments (not converting years to months)

• Making calculation errors with large exponents

Mike takes out a 5-year business loan for $200,000 at an interest rate of 7.0%. His monthly payment is $3,957. What is the total interest he will pay over the life of the loan?

Step 1: Calculate total number of payments = 5 years × 12 months/year = 60 payments

Step 2: Calculate total amount paid = $3,957 × 60 = $237,420

Step 3: Calculate total interest = Total paid - Principal = $237,420 - $200,000 = $37,420

Therefore, Mike will pay $37,420 in interest over the life of his loan.

This example shows how interest adds significantly to the total cost of a business loan. In this case, Mike will pay almost 19% more than the original loan amount due to interest charges. This demonstrates why it's important to consider both monthly payments and total interest costs when evaluating loan options.

Total Interest: The sum of all interest payments over the life of the loan

Loan Term: The length of time to repay the loan

Principal: The original loan amount

• Total interest = (Monthly payment × Number of payments) - Principal

• Longer loan terms result in more total interest paid

• Higher interest rates increase total interest significantly

• Remember: Total paid = Monthly payment × Total number of payments

• Total interest is always Total paid minus Principal

• Use this calculation to compare different loan scenarios

• Forgetting to multiply monthly payment by total number of payments

• Subtracting the wrong amounts when calculating interest

• Confusing monthly interest with total interest over the loan term

Sarah is comparing a conventional business loan at 8.0% interest with an SBA loan at 6.5% interest. Both are for $250,000 over 10 years. How much will she save in interest with the SBA loan? (Calculate both monthly payments and total interest)

Step 1: Conventional loan (8.0%)

Monthly rate: 0.08 ÷ 12 = 0.006667, n = 120

Monthly payment: $250,000 × [0.006667(1.006667)^120]/[(1.006667)^120 - 1] = $3,037

Total interest: $3,037 × 120 - $250,000 = $114,440

Step 2: SBA loan (6.5%)

Monthly rate: 0.065 ÷ 12 = 0.005417, n = 120

Monthly payment: $250,000 × [0.005417(1.005417)^120]/[(1.005417)^120 - 1] = $2,855

Total interest: $2,855 × 120 - $250,000 = $92,600

Step 3: Interest savings: $114,440 - $92,600 = $21,840

Therefore, Sarah saves $21,840 in interest with the SBA loan.

This demonstrates the significant impact of interest rates on business loan costs. Even a 1.5% difference in interest rate results in over $20,000 in savings over the life of the loan. SBA loans often provide these favorable rates due to government backing, making them attractive for qualifying businesses.

SBA Loan: Government-guaranteed loan with favorable terms for small businesses

Interest Rate Differential: Difference between two interest rates

Government Guarantee: Federal backing that reduces lender risk

• Small rate differences compound significantly over long terms

• SBA loans often have lower rates than conventional loans

• Qualification requirements apply to SBA programs

• Always compare APRs when evaluating loan options

• Consider SBA programs for favorable terms

• Calculate total interest, not just monthly payments

• Focusing only on monthly payments instead of total cost

• Not researching SBA loan eligibility

• Ignoring the impact of small rate differences

Which of the following statements about equipment financing is TRUE?

The answer is B) The equipment serves as collateral for the loan. Equipment financing is a type of secured loan where the purchased equipment itself serves as collateral. This typically results in lower interest rates compared to unsecured loans because the lender has recourse to the equipment if the borrower defaults.

Equipment financing is a specialized loan product where the financed asset (equipment) secures the loan. This arrangement benefits both parties: the borrower gets favorable terms due to the security provided, and the lender has recourse to the equipment in case of default. The loan term often matches the useful life of the equipment.

Secured Loan: Loan backed by collateral

Equipment Financing: Loan specifically for purchasing business equipment

Collateral: Asset pledged as security for a loan

• Equipment serves as collateral in equipment financing

• Loan terms often match equipment useful life

• Generally offers lower rates than unsecured loans

• Match loan term to equipment useful life

• Consider depreciation schedules for tax planning

• Evaluate lease vs. buy options

• Confusing equipment financing with general business loans

• Not considering the equipment as collateral

• Ignoring tax implications of equipment financing

FAQ

Q: How do personal credit scores affect business loan terms?

A: Personal credit scores significantly impact business loan terms, especially for small businesses and startups. Most business lenders require personal guarantees, making the owner's credit history a critical factor.

For example, with a personal credit score above 750, a business might qualify for a loan at 6.0% interest. However, with a score below 650, the same business might face rates of 12-15% or be denied altogether.

Mathematically, if \( R_1 \) is the rate for excellent credit and \( R_2 \) is the rate for poor credit:

\( \text{Interest Differential} = P \times (R_2 - R_1) \times T \)

Where \( P \) is the principal and \( T \) is the term. For a $100,000 loan over 5 years, the difference between 6% and 12% is $30,000 in additional interest.

Q: Should I choose an SBA loan or conventional business loan?

A: The choice between SBA and conventional loans depends on your business profile and needs.

- SBA loans: Lower down payments (as low as 10%), longer terms (up to 25 years), competitive rates. Example: For a $200,000 loan at 6.5%, total interest is approximately \( \$73{,}000 \) over 10 years.

- Conventional loans: Faster approval, potentially higher amounts, but stricter requirements. Example: Same loan at 7.5% results in about \( \$83{,}000 \) total interest.

SBA loans typically save money over time but require more documentation and take longer to approve. Conventional loans may be suitable for established businesses with strong credit.