Lease Calculator

Fast payment calculator • 2026 rates

Lease Payment Formula:

Show the calculator\( \text{Monthly Payment} = \frac{\text{Depreciation Fee} + \text{Finance Fee}}{12} \)

Where:

- \( \text{Depreciation Fee} = \frac{\text{MSRP} - \text{Residual Value}}{\text{Lease Term}} \)

- \( \text{Finance Fee} = (\text{MSRP} + \text{Residual Value}) \times \text{Money Factor} \)

- \( \text{Money Factor} = \frac{\text{Interest Rate}}{2400} \)

This formula calculates the monthly lease payment based on vehicle depreciation and financing costs.

Example: For a car with MSRP of \( \$35{,}000 \), residual value of \( \$21{,}000 \), and lease term of 36 months at 3.0% interest:

Money Factor: \( \frac{3.0}{2400} = 0.00125 \)

Depreciation: \( \frac{35{,}000 - 21{,}000}{36} = \$388.89 \)

Finance Fee: \( (35{,}000 + 21{,}000) \times 0.00125 = \$70 \)

Monthly Payment: \( \$388.89 + \$70 = \$458.89 \)

Thus, the lessee would pay approximately $458.89 per month for 36 months.

Vehicle Details

Options

Results

| Month | Payment | Depreciation | Financing | Remaining Value |

|---|

Residual Value: $21,000

Percentage of MSRP: 60%

Expected depreciation rate: 40%

Total Depreciation: $11,000

Monthly Depreciation: $388.89

Financing Cost: $70.00

Comprehensive Lease Guide

A lease is a contract allowing you to drive a vehicle for a specific period (typically 24-48 months) in exchange for monthly payments. Unlike buying, you don't own the vehicle at the end of the lease term. Leasing allows access to newer vehicles with lower monthly payments but comes with mileage limits and wear-and-tear responsibilities.

The standard lease payment calculation uses the following formula:

Where:

- \( \text{Depreciation Fee} = \frac{\text{Adjusted Capital Cost} - \text{Residual Value}}{\text{Lease Term}} \)

- \( \text{Finance Fee} = (\text{Adjusted Capital Cost} + \text{Residual Value}) \times \text{Money Factor} \)

- \( \text{Adjusted Capital Cost} = \text{Selling Price} - \text{Down Payment} + \text{Trade-in Value} \)

Low payments

New cars

No resale

Own asset

Higher payments

Equity build

- Negotiate the capitalized cost: Focus on getting the best selling price, not the lowest monthly payment

- Check residual values: Higher residuals mean lower depreciation costs

- Consider lease-end options: Purchase, lease another, or return

- Understand mileage limits: Typical allowance is 12,000-15,000 miles/year

- Maintain the vehicle: Keep within wear standards to avoid excess charges

Lease Basics

Rental agreement for vehicle use with monthly payments.

\( \text{Payment} = \frac{\text{Depreciation} + \text{Finance Fee}}{12} \)

Depreciation = (Capital Cost - Residual) ÷ Term, Finance = (Cost + Residual) × Money Factor

- Depreciation is biggest cost factor

- Higher residuals = lower payments

- Mileage limits apply

Strategies

Focus on capitalized cost, residual value, and money factor.

- Negotiate selling price

- Research residuals

- Shop money factors

- Consider lease specials

- Mileage restrictions

- Wear standards

- End-of-lease fees

- Early termination costs

Lease Learning Quiz

Which of the following is NOT a component of a typical monthly lease payment?

The answer is C) Insurance Premium. A typical lease payment consists of the depreciation fee (the portion that covers the vehicle's expected depreciation during the lease term) and the finance fee (the interest charge for borrowing the money). Insurance premiums are separate and not included in the monthly lease payment.

Understanding the components of a lease payment is crucial because many people confuse lease payments with total ownership costs. The monthly lease payment primarily covers depreciation and financing costs. Insurance, registration, and maintenance are additional expenses that are separate from the lease payment.

Depreciation Fee: The portion of the lease payment that covers the vehicle's expected loss in value during the lease term

Finance Fee: The interest charge for borrowing the money used to lease the vehicle

Money Factor: The financing rate used in lease calculations (multiply by 2400 to get APR)

• Lease payments = Depreciation + Finance Fee

• Insurance is typically a separate cost

• Sales tax may be included depending on location

• Remember: Lease payments cover depreciation and financing

• Use the mnemonic "DFI" - Depreciation, Finance, Insurance (separate)

• Including insurance in lease payment calculations

• Forgetting that sales tax varies by location

• Confusing lease payments with total ownership costs

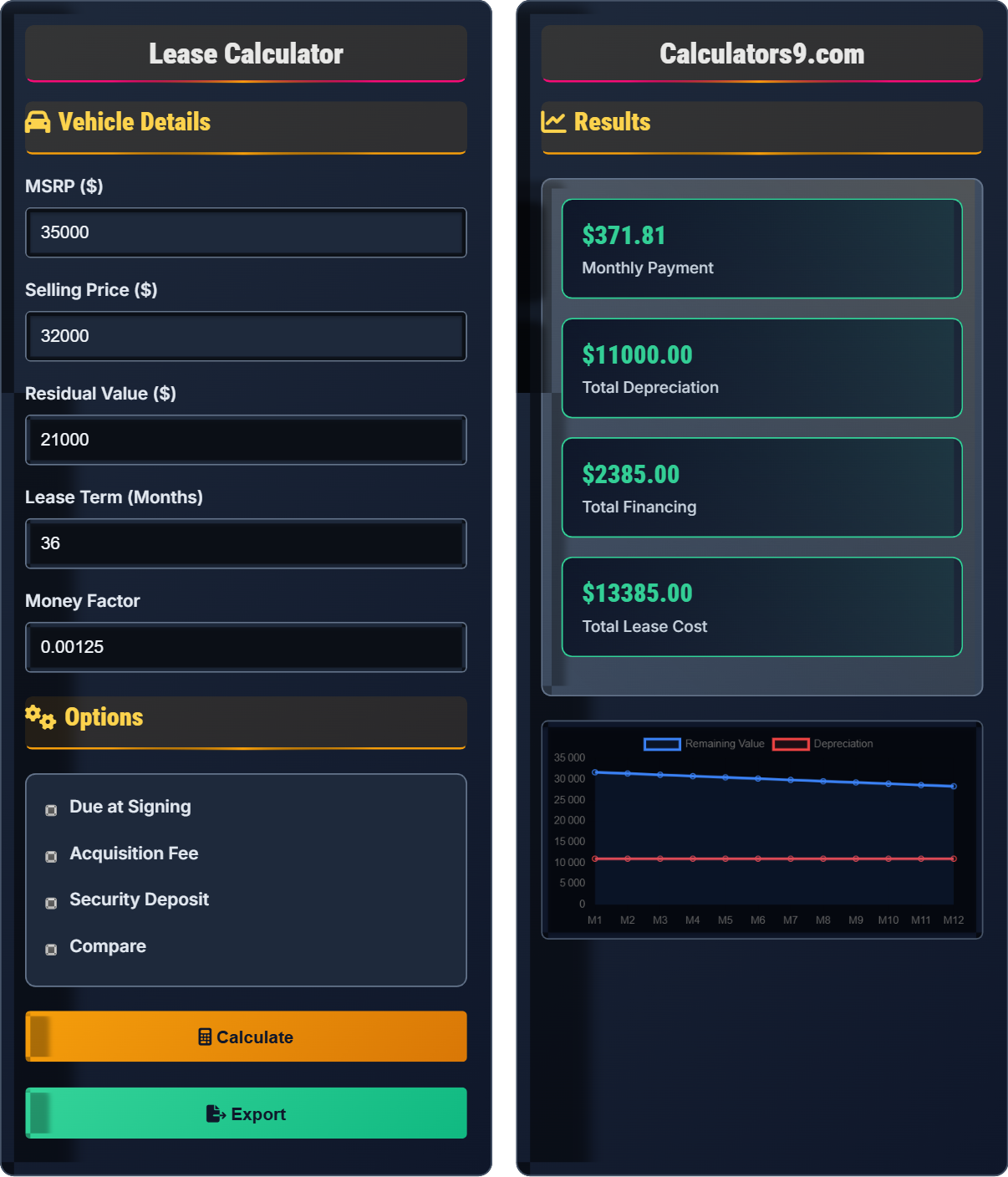

Calculate the monthly lease payment for a vehicle with MSRP of $35,000, selling price of $32,000, residual value of $21,000, lease term of 36 months, and money factor of 0.00125. Show your work.

Step 1: Calculate Depreciation Fee = (Selling Price - Residual Value) ÷ Lease Term

Depreciation Fee = ($32,000 - $21,000) ÷ 36 = $11,000 ÷ 36 = $305.56

Step 2: Calculate Finance Fee = (Selling Price + Residual Value) × Money Factor

Finance Fee = ($32,000 + $21,000) × 0.00125 = $53,000 × 0.00125 = $66.25

Step 3: Calculate Monthly Payment = Depreciation Fee + Finance Fee

Monthly Payment = $305.56 + $66.25 = $371.81

This problem demonstrates how lease payments are calculated based on vehicle depreciation and financing costs. The depreciation fee represents the cost of using the vehicle during the lease term, while the finance fee represents the interest on the money borrowed. Higher residual values result in lower monthly payments since the vehicle is expected to retain more value.

Residual Value: The estimated value of the vehicle at the end of the lease term

Money Factor: The financing rate used in lease calculations

Depreciation: The decrease in vehicle value over time

• Depreciation = (Capital Cost - Residual) ÷ Term

• Finance Fee = (Capital Cost + Residual) × Money Factor

• Higher residuals = lower payments

• Remember: Depreciation is (High - Low) ÷ Time

• Finance Fee uses addition: (High + Low) × Factor

• Research residuals before leasing

• Using MSRP instead of selling price in calculations

• Adding rather than subtracting for depreciation

• Forgetting to divide by lease term

Sarah leases a car for 36 months with a monthly payment of $420. She also pays $2,500 due at signing, including the first month's payment. If she returns the car at the end of the lease term, what is her total cost for the lease?

Step 1: Calculate total monthly payments = $420 × 36 = $15,120

Step 2: Subtract first month's payment from due at signing = $2,500 - $420 = $2,080

Step 3: Calculate total lease cost = Monthly payments + Due at signing adjustment

Total Lease Cost = $15,120 + $2,080 = $17,200

Therefore, Sarah's total cost for the lease is $17,200.

This example shows the importance of understanding what's included in "due at signing." Typically, this includes the first month's payment, security deposit, acquisition fee, and other charges. To calculate the true total cost, we need to separate the first payment from other upfront costs to avoid double counting.

Due at Signing: Upfront costs paid when signing the lease agreement

Total Lease Cost: Sum of all payments made during the lease term

Acquisition Fee: One-time fee charged by the leasing company

• Due at signing often includes first month's payment

• Total cost = Monthly payments + Adjusted due at signing

• Always verify what's included in due at signing

• Always ask what's included in due at signing

• Calculate total cost separately from monthly payment

• Budget for potential excess wear fees

• Double counting the first month's payment

• Forgetting to include due at signing costs

• Not accounting for potential end-of-lease fees

John leases a car for 36 months with a mileage allowance of 12,000 miles per year (36,000 total). His lease charges $0.25 per mile over the limit. If John drives 42,000 miles during the lease, how much will he owe for excess mileage at lease end?

Step 1: Calculate excess miles = Total miles driven - Allowed miles

Excess Miles = 42,000 - 36,000 = 6,000 miles

Step 2: Calculate excess mileage fee = Excess miles × Per-mile charge

Excess Mileage Fee = 6,000 × $0.25 = $1,500

Step 3: Add to total lease cost if calculating overall expense

Therefore, John will owe $1,500 for excess mileage at lease end.

This demonstrates how mileage limits can significantly impact lease costs. Lease agreements specify an annual mileage allowance, typically 12,000-15,000 miles per year. Driving beyond these limits incurs additional charges that can add up quickly. It's important to estimate your driving needs accurately when selecting a lease.

Mileage Allowance: Maximum number of miles permitted during the lease term

Excess Mileage Fee: Charge for driving beyond the allowed mileage

Wear-and-Tear Policy: Standards for acceptable vehicle condition

• Typical allowance is 12,000-15,000 miles/year

• Excess mileage fees range from $0.15-$0.30/mile

• Costs can be substantial if exceeded significantly

• Estimate annual mileage before leasing

• Consider negotiating higher allowance if needed

• Track mileage during lease term

• Underestimating annual mileage needs

• Forgetting to track mileage during lease

• Not budgeting for potential excess fees

Which of the following statements about leasing versus buying is TRUE?

The answer is B) Buying builds equity in the vehicle. When you buy a car, you own it and build equity as you pay down the loan and the vehicle depreciates. In contrast, leasing is essentially renting the vehicle, so you don't build equity. Leasing typically offers lower monthly payments, but comes with mileage restrictions and no ownership at the end.

Understanding the fundamental differences between leasing and buying is essential for making an informed decision. Buying creates an asset (the vehicle) that you own, while leasing provides temporary use of the vehicle. Equity represents the portion of the vehicle's value that you actually own, which increases as you pay down the loan.

Equity: The portion of the vehicle's value that you own

Depreciation: The decrease in vehicle value over time

Ownership: Having legal title to the vehicle

• Buying builds equity, leasing does not

• Leasing typically has lower monthly payments

• Leasing has mileage and wear restrictions

• Consider your driving needs when choosing

• Think about keeping the car long-term

• Factor in maintenance and repair costs

• Focusing only on monthly payments

• Not considering total cost of ownership

• Forgetting about lease-end restrictions

FAQ

Q: How does the residual value affect my lease payments?

A: The residual value is critical in determining your lease payment because it represents the vehicle's expected value at lease end. A higher residual value means the vehicle is expected to retain more of its value, which reduces the depreciation you pay for.

Using the formula: \( \text{Depreciation Fee} = \frac{\text{Capital Cost} - \text{Residual Value}}{\text{Lease Term}} \)

For example, if a car has a capital cost of \( \$30{,}000 \) and a 36-month lease:

With 60% residual (\( \$18{,}000 \)): Depreciation = \( \frac{30{,}000 - 18{,}000}{36} = \$333.33 \)

With 50% residual (\( \$15{,}000 \)): Depreciation = \( \frac{30{,}000 - 15{,}000}{36} = \$416.67 \)

Higher residuals result in significantly lower monthly payments.

Q: Should I lease or buy a luxury car?

A: Luxury cars often make sense to lease due to their rapid depreciation and high purchase prices.

Leasing benefits:

- Lower monthly payments (luxury cars have high MSRP but good residuals)

- Access to latest models and technology

- Warranty coverage during lease term

- Typical lease: 24-36 months, 10,000-15,000 miles/year

Buying benefits:

- Build equity in expensive asset

- No mileage restrictions

- Keep car long-term

For example, a $60,000 luxury sedan might lease for $700-900/month versus $1,200-1,500/month loan payment.