Depreciation Calculator

Business asset depreciation & tax calculator • 2026

Depreciation Formulas:

Show the calculatorStraight-Line Method: \( \text{Annual Depreciation} = \frac{\text{Cost} - \text{Salvage Value}}{\text{Useful Life}} \)

Declining Balance: \( \text{Annual Depreciation} = \text{Book Value} \times \text{Rate} \)

Sum-of-Years Digits: \( \text{Annual Depreciation} = \frac{\text{Remaining Life}}{\text{Sum of Years}} \times (\text{Cost} - \text{Salvage Value}) \)

MACRS: \( \text{Annual Depreciation} = \text{Cost} \times \text{MACRS Rate} \)

Where:

- \( \text{Cost} \) = Initial cost of the asset

- \( \text{Salvage Value} \) = Estimated value at end of useful life

- \( \text{Useful Life} \) = Expected number of years of service

- \( \text{Book Value} \) = Asset value after accumulated depreciation

- \( \text{Rate} \) = Depreciation rate (typically 2x straight-line rate for DDB)

These formulas calculate the systematic allocation of an asset's cost over its useful life. Straight-line provides consistent annual deductions, declining balance accelerates deductions early, sum-of-years digits provides moderate acceleration, and MACRS is required for tax purposes. Each method affects cash flow and tax liability differently.

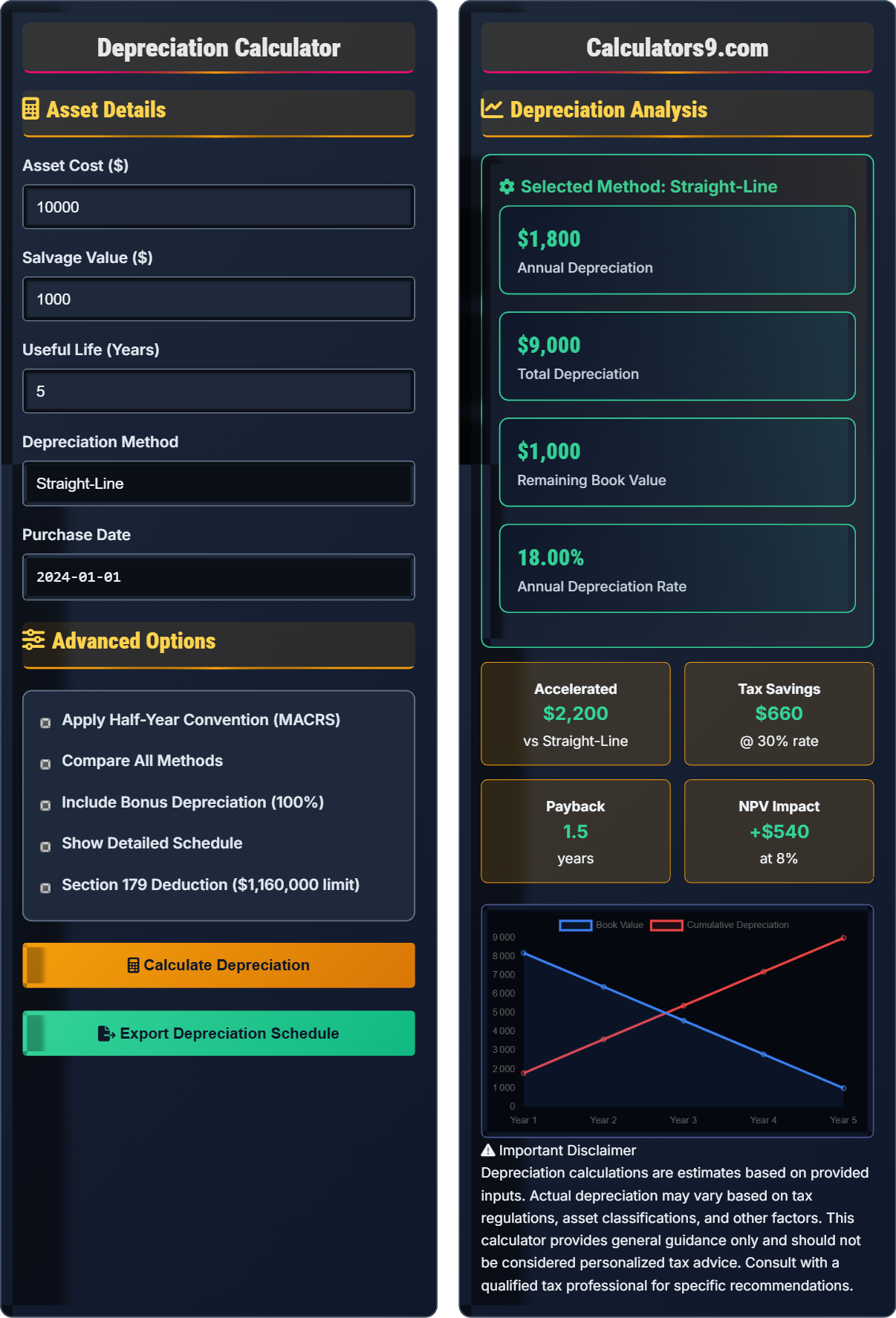

Example: For a $10,000 asset with $1,000 salvage value and 5-year life:

Straight-Line: ($10,000 - $1,000) ÷ 5 = $1,800 annually

Double Declining: 2 ÷ 5 = 40% rate; Year 1: $10,000 × 0.40 = $4,000

Sum-of-Years: Sum = 5+4+3+2+1 = 15; Year 1: (5÷15) × $9,000 = $3,000

Asset Details

Advanced Options

Depreciation Analysis

Accelerated

vs Straight-Line

Tax Savings

@ 30% rate

Payback

years

NPV Impact

at 8%

Depreciation calculations are estimates based on provided inputs. Actual depreciation may vary based on tax regulations, asset classifications, and other factors. This calculator provides general guidance only and should not be considered personalized tax advice. Consult with a qualified tax professional for specific recommendations.

Depreciation Fundamentals

Depreciation is the systematic allocation of an asset's cost over its useful life. It represents the decline in value due to wear and tear, obsolescence, or passage of time.

Straight-Line

Annual deductions

Double Declining

Early deductions

Sum-of-Years

Acceleration

MACRS

Method

- Cost Basis: Original purchase price plus improvements

- Useful Life: Estimated period of productive service

- Salvage Value: Estimated residual value at end of life

- Book Value: Asset value after accumulated depreciation

- Depreciable Base: Cost minus salvage value

Depreciation Methods

Different methods serve different business and tax objectives.

| Method | Formula | Best For | Advantage | Disadvantage |

|---|---|---|---|---|

| Straight-Line | (Cost - SV) ÷ Useful Life | Consistent assets | Simple, predictable | Slower tax benefits |

| Double Declining | 2 × (SL rate) × BV | Technology, vehicles | Fast tax savings | Complex, uneven |

| Sum-of-Years | (Remaining ÷ Sum) × DB | Moderate acceleration | Balanced approach | More complex |

| MACRS | Cost × Table rate | Tax compliance | Required method | No choice |

- Assets must have useful life > 1 year

- Depreciation stops at salvage value

- Methods must be consistently applied

- Changes require IRS approval

- Tax and book methods can differ

Tax Considerations

Companies often use different methods for tax and financial reporting.

Book Depreciation

Financial reporting

Tax Depreciation

Tax compliance

Bonus Depreciation

Temporary benefit

Section 179

Immediate expensing

- MACRS is required for tax purposes

- Bonus depreciation is temporary

- Section 179 has limits and phaseouts

- Depreciation recapture on sale

- Mid-quarter convention applies to some assets

Depreciation Calculation Learning Quiz

What is the annual depreciation for an asset costing $15,000 with $3,000 salvage value and 6-year useful life using straight-line method?

The answer is A) $2,000. Using the straight-line formula:

Annual Depreciation = (Cost - Salvage Value) ÷ Useful Life

Annual Depreciation = ($15,000 - $3,000) ÷ 6

Annual Depreciation = $12,000 ÷ 6 = $2,000

The straight-line method evenly distributes the depreciable base (cost minus salvage value) over the asset's useful life. This creates consistent annual deductions that are easy to calculate and predict. It's the simplest method and most commonly used for book purposes.

Depreciable Base: Cost minus salvage value

Useful Life: Estimated period of service

Salvage Value: Estimated residual value

• Divide depreciable base by useful life

• Consistent annual deductions

• Simplest calculation method

• Remember: (Cost - SV) ÷ Life

• Always subtract salvage value first

• Consistent deductions each year

• Forgetting to subtract salvage value

• Using cost instead of depreciable base

• Not dividing by useful life

Calculate the first year depreciation for a $20,000 asset with $2,000 salvage value and 5-year life using double declining balance method. Show your work.

Step 1: Calculate straight-line rate

SL Rate = 1 ÷ Useful Life = 1 ÷ 5 = 0.20 or 20%

Step 2: Calculate double declining rate

DD Rate = 2 × SL Rate = 2 × 0.20 = 0.40 or 40%

Step 3: Calculate first year depreciation

Year 1 Depreciation = Book Value × DD Rate

Year 1 Depreciation = $20,000 × 0.40 = $8,000

Therefore, the first year depreciation is $8,000.

The double declining balance method accelerates depreciation by using twice the straight-line rate applied to the current book value. This front-loads deductions, providing greater tax benefits in early years. The rate remains constant, but the base (book value) decreases each year.

Double Declining Rate: 2 × straight-line rate

Book Value: Asset value after accumulated depreciation

Accelerated Depreciation: Front-loaded deductions

• Rate is 2 × straight-line rate

• Apply to current book value

• Switch to straight-line if needed

• DDB Rate = 200% ÷ Useful Life

• Always apply to current book value

• Greater deductions in early years

• Using original cost instead of book value

• Forgetting to double the rate

• Not considering salvage value limitations

Calculate the first year depreciation for a $25,000 asset with $5,000 salvage value and 4-year life using sum-of-years digits method. Show your work.

Step 1: Calculate depreciable base

Depreciable Base = Cost - Salvage Value

Depreciable Base = $25,000 - $5,000 = $20,000

Step 2: Calculate sum of years digits

Sum = 4 + 3 + 2 + 1 = 10

Step 3: Calculate first year fraction

Year 1 Fraction = Remaining Life ÷ Sum of Years

Year 1 Fraction = 4 ÷ 10 = 0.40

Step 4: Calculate first year depreciation

Year 1 Depreciation = Depreciable Base × Year 1 Fraction

Year 1 Depreciation = $20,000 × 0.40 = $8,000

Therefore, the first year depreciation is $8,000.

The sum-of-years digits method accelerates depreciation by assigning higher fractions to earlier years. The sum of years digits for an n-year asset is n(n+1)/2. Each year's fraction is the remaining useful life divided by this sum. This creates a decreasing pattern of deductions.

Sum of Years Digits: 1+2+3+...+n

Depreciable Base: Cost minus salvage value

Remaining Life: Years left in useful life

• Calculate sum of years digits first

• Fraction = Remaining life ÷ Sum

• Apply to depreciable base

• Sum = n(n+1)÷2

• First year = n÷sum

• Last year = 1÷sum

• Calculating sum incorrectly

• Using cost instead of depreciable base

• Mixing up remaining life order

A company purchases $50,000 of office equipment (5-year property). Using MACRS, what is the depreciation in Year 1 if the half-year convention applies? (5-year rates: 20%, 32%, 19.2%, 11.52%, 11.52%, 5.76%)

Step 1: Identify MACRS rate for 5-year property in Year 1

Standard Year 1 rate = 20%

Step 2: Apply half-year convention

With half-year convention, only 6 months of depreciation in Year 1

Adjusted Year 1 rate = 20% × 0.5 = 10%

Step 3: Calculate depreciation

Year 1 Depreciation = Cost × Adjusted Rate

Year 1 Depreciation = $50,000 × 0.10 = $5,000

Therefore, the Year 1 MACRS depreciation is $5,000.

MACRS (Modified Accelerated Cost Recovery System) is the tax depreciation method required by the IRS. The half-year convention assumes all property is placed in service mid-year, resulting in only half a year's depreciation in the first year. This convention applies to most property types.

MACRS: Modified Accelerated Cost Recovery System

Half-Year Convention: Mid-year placement assumption

Recovery Period: Asset classification period

• Required for tax purposes

• Uses predetermined tables

• Know recovery periods for asset types

• Understand convention rules

• Use IRS tables for rates

• Forgetting convention adjustments

• Using wrong recovery period

• Not following IRS tables

Which depreciation method provides the greatest tax benefit in the early years?

The answer is B) Double Declining Balance. The double declining balance method provides the greatest acceleration of depreciation deductions in the early years. It applies a rate that is twice the straight-line rate to the current book value, resulting in the highest first-year deduction among the traditional methods.

Double declining balance provides maximum front-loading of depreciation deductions, which is beneficial for tax purposes due to the time value of money. The higher deductions in early years provide greater tax savings when the present value of those savings is considered. However, MACRS is required for tax purposes.

Acceleration: Front-loading of deductions

Tax Benefit: Reduced tax liability

Time Value of Money: Present value of future benefits

• DDB provides maximum acceleration

• Greater early-year benefits

• Higher deductions initially

• DDB: 200% of straight-line rate

• 150% DB is also available

• Consider switch to straight-line

• Confusing acceleration levels

• Not considering salvage value

• Forgetting rate calculations

FAQ

Q: Can I use different depreciation methods for book and tax purposes?

A: Yes, companies can use different depreciation methods for book (GAAP) and tax (MACRS) purposes:

- Book Purposes: Companies often use straight-line for consistency

- Tax Purposes: MACRS is required by IRS

- Temporary Differences: Create book-tax differences

- Deferred Taxes: Result from timing differences

For example, you might depreciate an asset over 7 years straight-line for book purposes but use MACRS 5-year property for tax purposes. This creates temporary differences that require deferred tax accounting. The tax method typically provides faster deductions.

Q: What is bonus depreciation and how does it work?

A: Bonus depreciation allows immediate deduction of a percentage of asset cost in the year placed in service:

- Current Rate: 100% for qualified property (through 2022)

- Phaseout: Reduces by 20% annually starting in 2023

- Eligible Property: New, depreciable property with recovery period of 20 years or less

- Limitations: Cannot exceed business income

For example, if you purchase $100,000 of qualifying equipment in 2022, you could deduct the entire $100,000 in that year. This provides immediate tax benefits, unlike traditional depreciation which spreads deductions over years.