Pension Calculator

Retirement planning • 2026 projections

Pension Formula:

Show the calculator\( FV = PV \times (1 + r)^n + PMT \times \left(\frac{(1 + r)^n - 1}{r}\right) \)

Where:

- \( FV \) = Future Value (retirement savings at retirement)

- \( PV \) = Present Value (current retirement savings)

- \( r \) = Annual rate of return (as decimal)

- \( n \) = Number of years until retirement

- \( PMT \) = Annual contribution amount

This formula calculates the total retirement savings by combining the growth of current savings and the growth of regular contributions.

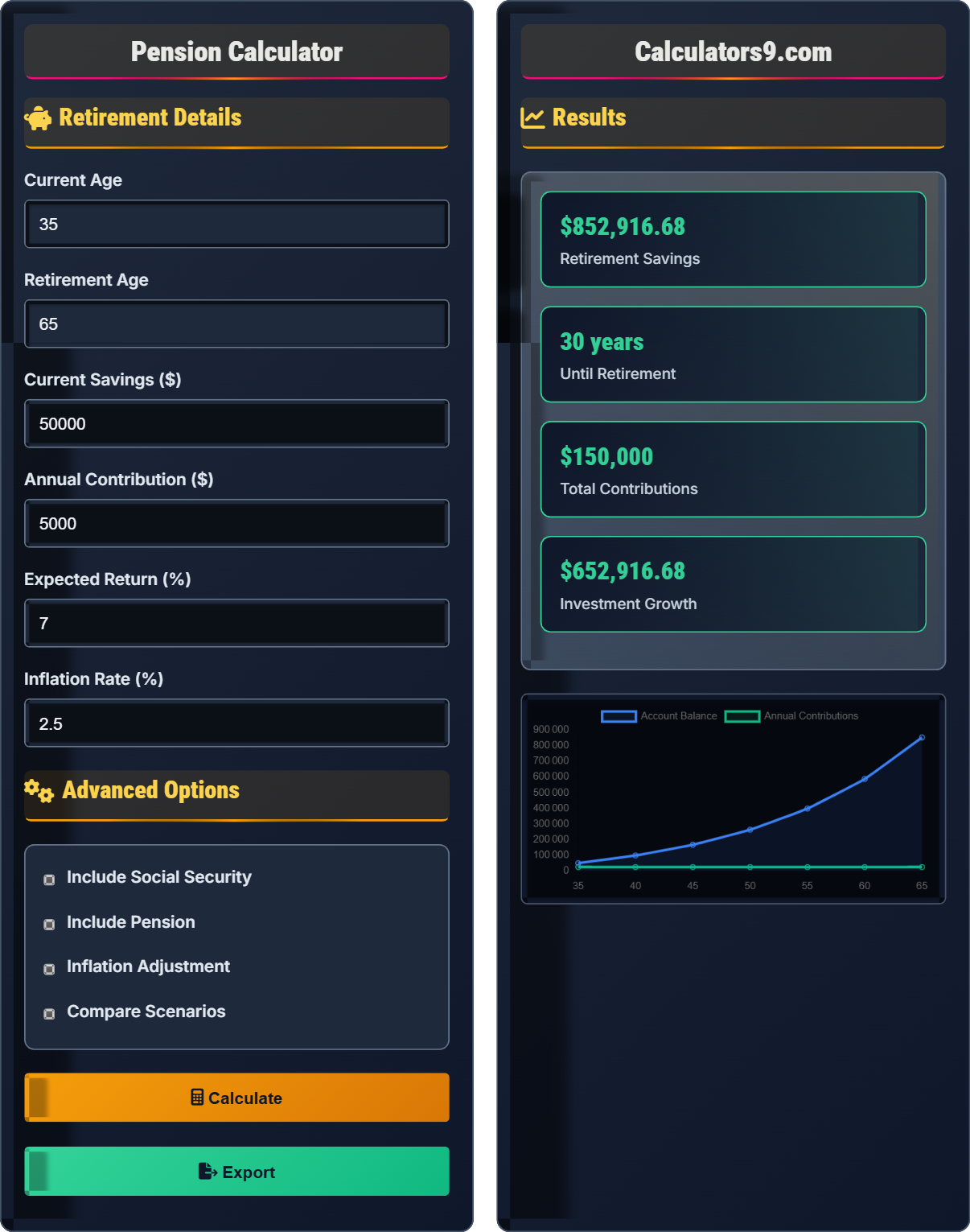

Example: For current savings of \( PV = \$50{,}000 \), annual contributions of \( PMT = \$5{,}000 \), 30 years to retirement at 7% annual return:

\( FV = 50{,}000 \times (1.07)^{30} + 5{,}000 \times \left(\frac{(1.07)^{30} - 1}{0.07}\right) \)

\( FV = 50{,}000 \times 7.612 + 5{,}000 \times 94.461 \)

\( FV = 380{,}600 + 472{,}305 = \$852{,}905 \)

Thus, the retiree would have approximately $852,905 at retirement.

Retirement Details

Advanced Options

Results

| Year | Age | Balance | Contribution | Growth |

|---|

| Category | Amount | Monthly |

|---|

Comprehensive Pension Planning Guide

Pension planning is the process of preparing financially for retirement by estimating future income needs and determining how much to save regularly. It involves calculating how much money you'll need in retirement, considering factors like inflation, life expectancy, and desired lifestyle. Effective pension planning ensures financial security and independence during your golden years.

The standard pension calculation uses the future value of an annuity formula:

Where:

- \(FV\) = Future Value (total retirement savings)

- \(PV\) = Present Value (current retirement savings)

- \(r\) = Annual rate of return (as decimal)

- \(n\) = Number of years until retirement

- \(PMT\) = Annual contribution amount

Your retirement income typically comes from multiple sources:

- Personal Savings: 401(k), IRAs, taxable investment accounts

- Social Security: Government benefits based on work history

- Pensions: Employer-provided defined benefit plans

- Other Income: Part-time work, rental income, annuities

- Start Early: Take advantage of compound interest and dollar-cost averaging

- Maximize Employer Match: Contribute enough to receive full company match

- Diversify Investments: Balance stocks, bonds, and other assets

- Rebalance Regularly: Adjust portfolio allocation as you age

- Consider Inflation: Plan for rising costs in retirement

Pension Basics

Regular income during retirement from various sources.

\(FV = PV \times (1 + r)^n + PMT \times \left(\frac{(1 + r)^n - 1}{r}\right)\)

Where FV=future value, PV=current savings, r=return rate, n=years, PMT=annual contribution.

- Compound interest grows exponentially over time

- Early contributions have maximum impact

- Higher returns = greater future value

Planning Strategies

Early contributions grow more than late contributions due to time value of money.

- Automate increases annually

- Bonus contributions

- Maximize employer match

- Consider catch-up contributions

- Inflation reduces purchasing power

- Healthcare costs increase with age

- Lifespan uncertainty affects planning

- Tax implications vary by account type

Pension Planning Learning Quiz

Which of the following is NOT a common source of retirement income?

The answer is D) Car Loan Payments. Car loan payments are an expense, not a source of retirement income. Common sources of retirement income include 401(k) accounts, Social Security benefits, defined benefit pensions from employers, and other investment accounts. Car loan payments represent an ongoing obligation that ends when the vehicle is paid off.

It's important to distinguish between retirement income sources and expenses when planning for retirement. Income sources provide money during retirement, while expenses reduce your available funds. Understanding this distinction helps in creating realistic retirement budgets and planning for adequate savings to cover expenses.

401(k): Employer-sponsored retirement account with tax advantages

Social Security: Government program providing retirement benefits

Defined Benefit Pension: Employer-provided guaranteed monthly payments

• Retirement income comes from savings, investments, and government programs

• Expenses during retirement must be covered by income sources

• Plan for both income and expense management in retirement

• Remember: Income - Expenses = Available funds

• Diversify retirement income sources for security

• Confusing expenses with income sources

• Not accounting for all potential retirement expenses

Calculate the future value of retirement savings with $30,000 current savings, $4,000 annual contributions, 25 years to retirement, and 6% annual return. Show your work.

Using the pension formula: \(FV = PV \times (1 + r)^n + PMT \times \left(\frac{(1 + r)^n - 1}{r}\right)\)

Given:

- PV = $30,000

- PMT = $4,000

- r = 0.06

- n = 25

Step 1: Calculate (1+r)^n = (1.06)^25 = 4.2919

Step 2: Calculate PV component: $30,000 × 4.2919 = $128,757

Step 3: Calculate annuity factor: \(\left(\frac{(1.06)^{25} - 1}{0.06}\right) = \left(\frac{4.2919 - 1}{0.06}\right) = 54.865\)

Step 4: Calculate PMT component: $4,000 × 54.865 = $219,460

Step 5: Calculate FV = $128,757 + $219,460 = $348,217

This calculation demonstrates how both current savings and regular contributions contribute to retirement wealth. The current savings grow through compound interest, while regular contributions accumulate over time and also earn compound returns. The combination creates substantial growth over long periods.

Future Value (FV): Value of an asset at a specific date in the future

Present Value (PV): Current value of a future sum of money

Compound Interest: Interest earned on both principal and previous interest

• Time is the most important factor in compound growth

• Both initial savings and regular contributions matter

• Higher returns accelerate growth significantly

• Start contributing early to maximize time advantage

• Consistent contributions build momentum over time

• Use online calculators for complex scenarios

• Forgetting to account for both current savings and contributions

• Misapplying the compound interest formula

• Not considering the impact of different time periods

Maria estimates she'll need $50,000 annually in today's dollars during retirement, which is 30 years away. If inflation averages 3% per year, how much will she actually need in retirement to maintain the same purchasing power?

Step 1: Use the future value formula to adjust for inflation: \(FV = PV \times (1 + r)^n\)

Step 2: Calculate future needed amount = $50,000 × (1.03)^30

Step 3: Calculate (1.03)^30 = 2.4273

Step 4: Calculate future amount needed = $50,000 × 2.4273 = $121,365

Therefore, Maria will need approximately $121,365 per year in retirement to maintain the same purchasing power as $50,000 today.

This example illustrates the significant impact of inflation on retirement planning. Over 30 years, even modest inflation of 3% per year nearly doubles the amount needed to maintain the same standard of living. This is why it's crucial to factor inflation into retirement calculations.

Inflation: General increase in prices and fall in purchasing power

Purchasing Power: Amount of goods/services that money can buy

Present Value: Today's worth of future money considering inflation

• Inflation reduces the purchasing power of money over time

• Higher inflation rates significantly impact retirement needs

• Plan for inflation-adjusted income needs in retirement

• Use historical inflation rates as a baseline

• Consider healthcare inflation which often exceeds general inflation

• Plan for 2-3% average inflation in long-term planning

• Ignoring inflation in retirement calculations

• Underestimating the impact of long-term inflation

• Confusing nominal and real (inflation-adjusted) amounts

David and Sarah both want to retire with $1 million. David starts saving at age 25, while Sarah starts at age 35. Both expect a 7% annual return. If David saves $X per year, how much more per year must Sarah save to reach the same goal by age 65? (Hint: Calculate the difference in required annual savings)

Step 1: David saves for 40 years (age 25-65) with 7% return

Step 2: Using formula: $1,000,000 = $0 × (1.07)^40 + X × [(1.07^40 - 1)/0.07]

Step 3: Calculate annuity factor = [(1.07^40 - 1)/0.07] = [14.9745 - 1]/0.07 = 199.635

Step 4: David's annual savings = $1,000,000 / 199.635 = $5,009

Step 5: Sarah saves for 30 years (age 35-65) with 7% return

Step 6: Calculate annuity factor = [(1.07^30 - 1)/0.07] = [7.6123 - 1]/0.07 = 94.461

Step 7: Sarah's annual savings = $1,000,000 / 94.461 = $10,586

Step 8: Difference = $10,586 - $5,009 = $5,577

Therefore, Sarah must save $5,577 more per year than David to reach the same goal.

This demonstrates the power of starting early. David has 10 extra years of compound growth, which dramatically reduces his required annual savings. The 10-year difference means Sarah must nearly double her annual contributions to achieve the same outcome. This is why financial advisors emphasize starting early.

Time Value of Money: Money available now is worth more than same amount later

Compound Growth: Growth on both principal and previously earned interest

Annual Savings Requirement: Amount needed to save each year to reach goal

• Every year of delay increases required savings significantly

• The earlier you start, the less you need to save annually

• Time is more valuable than money in retirement planning

• Start saving immediately, even with small amounts

• Take advantage of employer matching programs

• Increase contributions whenever possible

• Believing you can make up for lost time later

• Underestimating the impact of delayed start

• Not considering the exponential nature of compound growth

Which of the following is the most appropriate investment strategy for a 35-year-old planning for retirement?

The answer is C) Balanced portfolio with 70% stocks, 30% bonds. At age 35 with 30+ years until retirement, the investor has time to weather market volatility. A balanced portfolio allows for growth potential while providing some stability. While 90% stocks might offer higher returns, it also carries higher risk. A conservative approach at this age may not provide sufficient growth to meet retirement goals.

Investment allocation should consider both time horizon and risk tolerance. Young investors benefit from stock-heavy portfolios because they have time to recover from market downturns. As retirement approaches, portfolios typically shift toward more conservative allocations. The 70/30 split provides growth potential while managing risk appropriately for someone in their 30s.

Asset Allocation: Distribution of investments across different asset classes

Risk Tolerance: Ability to withstand investment value fluctuations

Time Horizon: Length of time until funds are needed

• Young investors can take more risk due to longer time horizons

• Portfolio allocation should adjust as retirement approaches

• Diversification reduces portfolio risk

• Use age-based rule: 100 minus your age for stock percentage

• Rebalance portfolio annually to maintain target allocation

• Consider target-date funds for automatic rebalancing

• Being too conservative at young age, missing growth opportunities

• Being too aggressive without understanding risk

• Not adjusting allocation as retirement approaches

FAQ

Q: How much should I save annually for a comfortable retirement?

A: A common guideline is to save 10-15% of your gross income annually for retirement. However, this varies based on your age, current savings, expected retirement age, and desired lifestyle.

For example, using the pension formula: If you're 35 with $50,000 in savings, earning $75,000 annually, planning to retire at 65 with a 7% return expectation, you'd need to save approximately $8,000-$12,000 annually (10-15% of income) to reach a retirement goal of $800,000-$1,200,000.

Mathematically: \(FV = 50,000 \times (1.07)^{30} + PMT \times \left(\frac{(1.07)^{30} - 1}{0.07}\right)\)

This formula shows how your savings goal depends on multiple variables including time, returns, and contribution amounts.

Q: Should I prioritize paying off debt or saving for retirement?

A: The decision depends on the interest rate of your debt versus potential investment returns.

- High-interest debt (>8%): Pay off first (credit cards, personal loans)

- Low-interest debt (<5%): Consider investing simultaneously, especially if employer matches

- Medium-interest debt: Balance both priorities

For example, if you have a 4% mortgage and can earn 7% annually in retirement accounts, investing may be better. But if you have credit card debt at 18%, paying that off should be priority.

Always prioritize getting your full employer 401(k) match before paying down low-interest debt.