College Cost Calculator

Fast cost estimator • 2026 rates

College Cost Formula:

Show the calculator\( \text{Net Cost} = \text{Total Cost} - \text{Financial Aid} \)

Where:

- \( \text{Total Cost} = \text{Tuition} + \text{Room & Board} + \text{Books & Supplies} + \text{Other Expenses} \)

- \( \text{Financial Aid} = \text{Grants} + \text{Scholarships} + \text{Work-Study} \)

This formula calculates the actual cost to families after financial assistance.

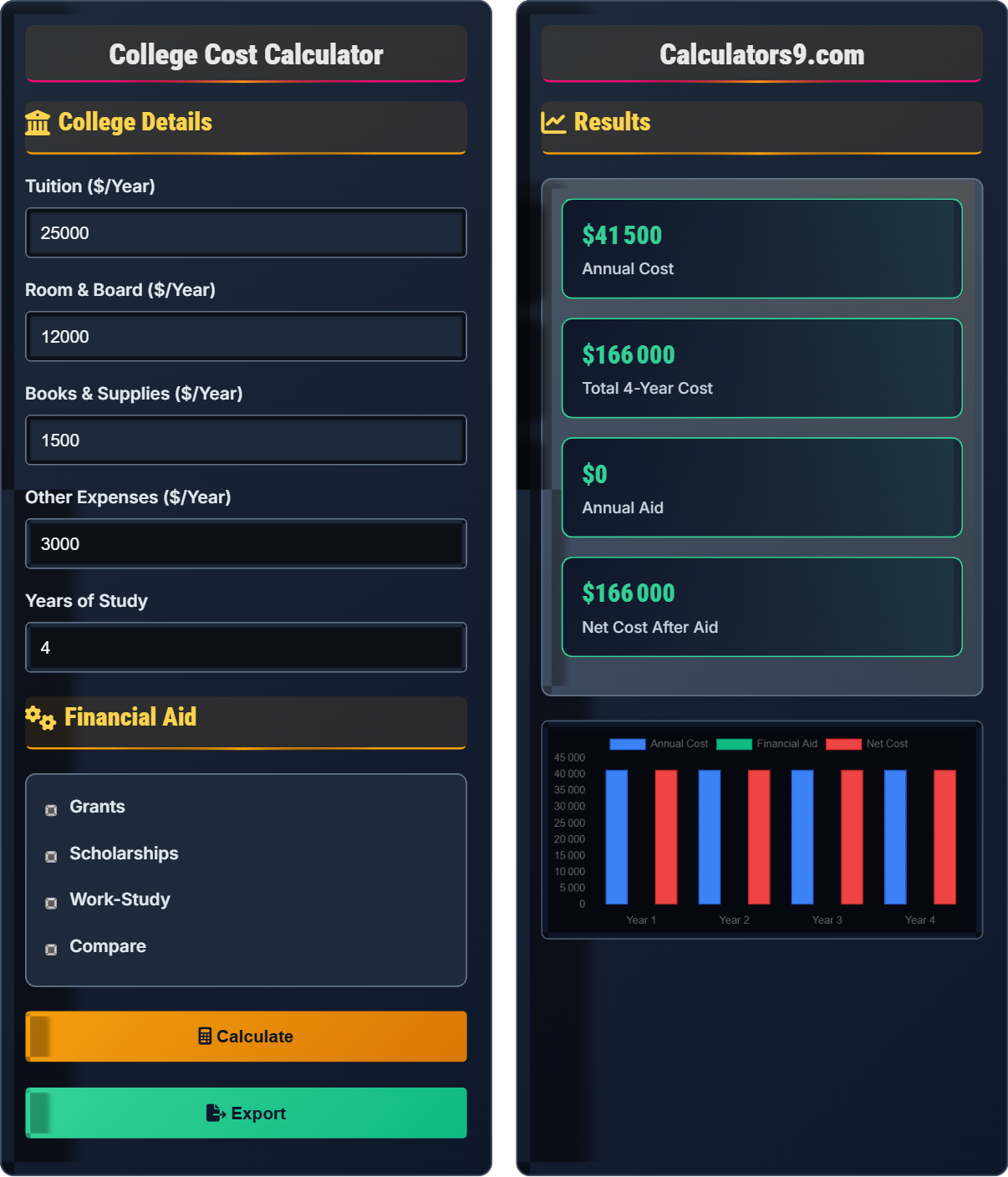

Example: For a college with tuition of \( \$25{,}000 \), room & board of \( \$12{,}000 \), books of \( \$1{,}500 \), and other expenses of \( \$3{,}000 \), with financial aid of \( \$15{,}000 \):

Total Cost: \( \$25{,}000 + \$12{,}000 + \$1{,}500 + \$3{,}000 = \$41{,}500 \)

Net Cost: \( \$41{,}500 - \$15{,}000 = \$26{,}500 \)

Thus, the family would pay approximately $26,500 per year.

College Details

Financial Aid

Results

| Expense Type | Annual Amount | 4-Year Total |

|---|

| Year | Cost Before Aid | Financial Aid | Net Cost |

|---|

Comprehensive College Cost Guide

College costs extend far beyond tuition. The total cost of attendance (COA) includes tuition and fees, room and board, books and supplies, transportation, and personal expenses. Understanding all components helps families plan effectively and identify opportunities for cost savings.

The standard college cost calculation uses the following formula:

Where:

- \( \text{Total Cost} = \text{Tuition} + \text{Room & Board} + \text{Books & Supplies} + \text{Other Expenses} \)

- \( \text{Financial Aid} = \text{Grants} + \text{Scholarships} + \text{Work-Study} \)

Financial aid can significantly reduce college costs:

- Grants: Need-based aid that doesn't require repayment

- Scholarships: Merit-based or need-based aid that doesn't require repayment

- Work-Study: Part-time employment opportunities for students

- Loans: Borrowed money that must be repaid with interest

Earnings

Savings

Tuition

Living

Grants

Scholarships

- Start at community college: Complete general education requirements at lower cost

- Live at home: Save on room and board expenses

- Apply for scholarships: Research and apply for numerous scholarship opportunities

- Buy used textbooks: Rent or purchase used books when possible

- Work-study programs: Earn money while gaining work experience

College Cost Basics

Total cost minus financial aid received.

\( \text{Net Cost} = \text{Total Cost} - \text{Financial Aid} \)

Where Total Cost = Tuition + Room & Board + Books + Other Expenses

- Net cost is what families actually pay

- Financial aid reduces net cost

- Costs vary significantly by institution

Strategies

Plan for all expenses across multiple years.

- Research financial aid opportunities

- Consider community college transfer

- Apply for multiple scholarships

- Plan for inflation in costs

- Public vs private cost differences

- In-state vs out-of-state tuition

- Merit vs need-based aid

- Expected Family Contribution

College Cost Learning Quiz

Which of the following is NOT typically included in the official "Cost of Attendance" reported by colleges?

The answer is C) Student Loan Interest. The official Cost of Attendance (COA) includes tuition, fees, room and board, books and supplies, transportation, and personal expenses. However, student loan interest is not included in COA calculations. Interest is a separate cost that occurs after borrowing begins.

Understanding the official components of Cost of Attendance is crucial for financial planning. The COA is used to determine financial aid eligibility and represents the maximum amount students can borrow. Loan interest is not included because it's not a direct cost of attending college but rather a consequence of financing that attendance.

Cost of Attendance (COA): The total amount it costs to attend a college for one year

Financial Aid Package: Combination of grants, scholarships, loans, and work-study

Net Price: Actual cost after subtracting gift aid

• COA includes direct and indirect costs

• Loan interest is not part of COA

• COA determines borrowing limits

• Look at published COA figures

• Calculate your own actual costs

• Factor in loan interest separately

• Including loan interest in COA calculations

• Not accounting for all expense categories

• Confusing sticker price with net price

Calculate the net cost of attendance for a college with tuition of $30,000, room and board of $14,000, books of $1,800, and other expenses of $2,500. The student receives $8,000 in grants and $4,000 in scholarships. Show your work.

Step 1: Calculate Total Cost of Attendance

Total Cost = Tuition + Room & Board + Books + Other Expenses

Total Cost = $30,000 + $14,000 + $1,800 + $2,500 = $48,300

Step 2: Calculate Total Financial Aid

Financial Aid = Grants + Scholarships

Financial Aid = $8,000 + $4,000 = $12,000

Step 3: Calculate Net Cost

Net Cost = Total Cost - Financial Aid

Net Cost = $48,300 - $12,000 = $36,300

Therefore, the net cost of attendance is $36,300 per year.

This problem demonstrates the fundamental calculation for determining the actual cost of college after financial assistance. The difference between the sticker price ($48,300) and net price ($36,300) shows the significant impact of financial aid. Understanding this calculation helps families plan more accurately for college expenses.

Sticker Price: Published cost before financial aid

Net Price: Actual cost after subtracting gift aid

Gift Aid: Grants and scholarships that don't require repayment

• Net cost = Total cost - Gift aid

• Include all expense categories

• Loans are not subtracted from cost

• Calculate for all years of study

• Factor in cost increases over time

• Consider work-study earnings as offset

• Including loans as aid in calculations

• Forgetting to include all expense categories

• Not accounting for multi-year costs

Sarah is planning to attend a university for four years. The current annual costs are: tuition $28,000, room and board $13,500, books $1,600, and other expenses $2,200. She expects costs to increase by 3% annually. She will receive $6,000 in grants each year. What will be the total net cost for her four-year education?

Step 1: Calculate Year 1 costs

Year 1 Total Cost = $28,000 + $13,500 + $1,600 + $2,200 = $45,300

Year 1 Net Cost = $45,300 - $6,000 = $39,300

Step 2: Calculate subsequent years with 3% increase

Year 2 Total Cost = $45,300 × 1.03 = $46,659

Year 2 Net Cost = $46,659 - $6,000 = $40,659

Year 3 Total Cost = $46,659 × 1.03 = $48,059

Year 3 Net Cost = $48,059 - $6,000 = $42,059

Year 4 Total Cost = $48,059 × 1.03 = $49,501

Year 4 Net Cost = $49,501 - $6,000 = $43,501

Step 3: Calculate total four-year net cost

Total Net Cost = $39,300 + $40,659 + $42,059 + $43,501 = $165,519

Therefore, the total net cost for Sarah's four-year education will be $165,519.

This example shows how college costs typically increase over time and how this affects long-term planning. The 3% annual increase results in a significant difference between the first-year cost ($39,300) and the total four-year cost ($165,519). Families should plan for these increases when budgeting for college.

Cost Inflation: Annual increase in college expenses

Multi-Year Planning: Considering costs over entire college period

Net Present Value: Today's value of future college costs

• College costs typically increase 3-5% annually

• Plan for multi-year expenses

• Consider inflation in savings plans

• Use 3-5% inflation rate in calculations

• Plan for entire duration of study

• Consider 529 plans for inflation protection

• Not accounting for annual cost increases

• Calculating only first-year costs

• Forgetting to include all expense categories

Mike wants to get a bachelor's degree but is concerned about costs. He's considering starting at a community college for two years (tuition $5,000/year) then transferring to a state university for two years (tuition $22,000/year). Compare this to going straight to the state university for four years. Assume room, board, and other expenses total $15,000/year at both institutions. Ignore financial aid for this calculation. How much does Mike save with the community college strategy?

Strategy 1: Community College + State University

Years 1-2 (Community College): ($5,000 + $15,000) × 2 = $40,000

Years 3-4 (State University): ($22,000 + $15,000) × 2 = $74,000

Total Cost = $40,000 + $74,000 = $114,000

Strategy 2: State University for 4 years

($22,000 + $15,000) × 4 = $148,000

Savings with Community College Strategy

$148,000 - $114,000 = $34,000

Therefore, Mike saves $34,000 by starting at community college.

This demonstrates how strategic college planning can significantly reduce costs. By completing general education requirements at a community college, students can save substantial amounts on tuition while still earning credits toward a four-year degree. This approach is particularly effective for students who plan to live at home during the community college years.

Transfer Student: Student who moves from one institution to another

Articulation Agreement: Formal agreement between institutions for credit transfer

Reverse Transfer: Credits from university back to community college

• Many credits transfer between institutions

• Ensure credits will transfer before enrolling

• Research transfer agreements

• Meet with advisors early

• Plan course sequence carefully

• Taking courses that won't transfer

• Not meeting transfer requirements

• Assuming all credits transfer automatically

Which of the following statements about financial aid is TRUE?

The answer is C) Need-based grants don't require repayment. Need-based grants such as the Federal Pell Grant are forms of gift aid that do not need to be repaid. They are awarded based on demonstrated financial need as determined by the FAFSA. Merit scholarships are based on academic or other achievements, not financial need.

Understanding the different types of financial aid is crucial for college planning. Gift aid (grants and scholarships) reduces the actual cost of attendance without creating debt. Work-study provides employment opportunities but doesn't reduce the cost of attendance directly. Loans must be repaid with interest, increasing the total cost of education.

Need-Based Aid: Financial assistance based on demonstrated need

Merit Aid: Financial assistance based on achievements

Gift Aid: Aid that doesn't require repayment

• Grants and scholarships don't require repayment

• Loans must be repaid with interest

• Work-study provides employment, not aid

• Prioritize gift aid over loans

• Apply for FAFSA early

• Search for outside scholarships

• Confusing grants with loans

• Not applying for sufficient aid

• Accepting loans without understanding terms

FAQ

Q: How does the Expected Family Contribution (EFC) affect financial aid awards?

A: The Expected Family Contribution (EFC) is calculated from the FAFSA and represents how much a family is expected to contribute to college costs. Financial aid is determined by subtracting the EFC from the Cost of Attendance (COA).

Formula: \( \text{Financial Aid Eligibility} = \text{COA} - \text{EFC} \)

For example, if a college's COA is \( \$50{,}000 \) and a family's EFC is \( \$15{,}000 \), the student would be eligible for up to \( \$35{,}000 \) in need-based aid. However, not all of this aid will necessarily be in the form of grants; some may be loans or work-study.

Q: Should I live on campus or off campus to save money?

A: The decision depends on your specific situation and the college location.

- On-campus advantages: Included in financial aid package, convenient, included utilities/Internet, social integration. Example: Room & board package at $12,000/year.

- Off-campus advantages: Potential savings if you can find affordable housing and split costs. Example: Apartment rental $8,000/year + utilities $1,200 = $9,200/year.

However, consider additional costs for off-campus living: transportation, groceries, furniture, utilities, and potential lease obligations. For some students, the convenience and all-inclusive nature of on-campus housing may be worth the premium.