Student Loan Calculator

Fast payment calculator • 2026 rates

Student Loan Payment Formula:

Show the calculator\( M = P \frac{r(1+r)^n}{(1+r)^n - 1} \)

Where:

- \( M \) = monthly payment

- \( P \) = loan principal (total loan amount)

- \( r \) = monthly interest rate (annual rate divided by 12, in decimal form)

- \( n \) = total number of monthly payments (loan term in years × 12)

This formula calculates the fixed monthly payment required to fully pay off a student loan over the loan term, taking into account compound interest.

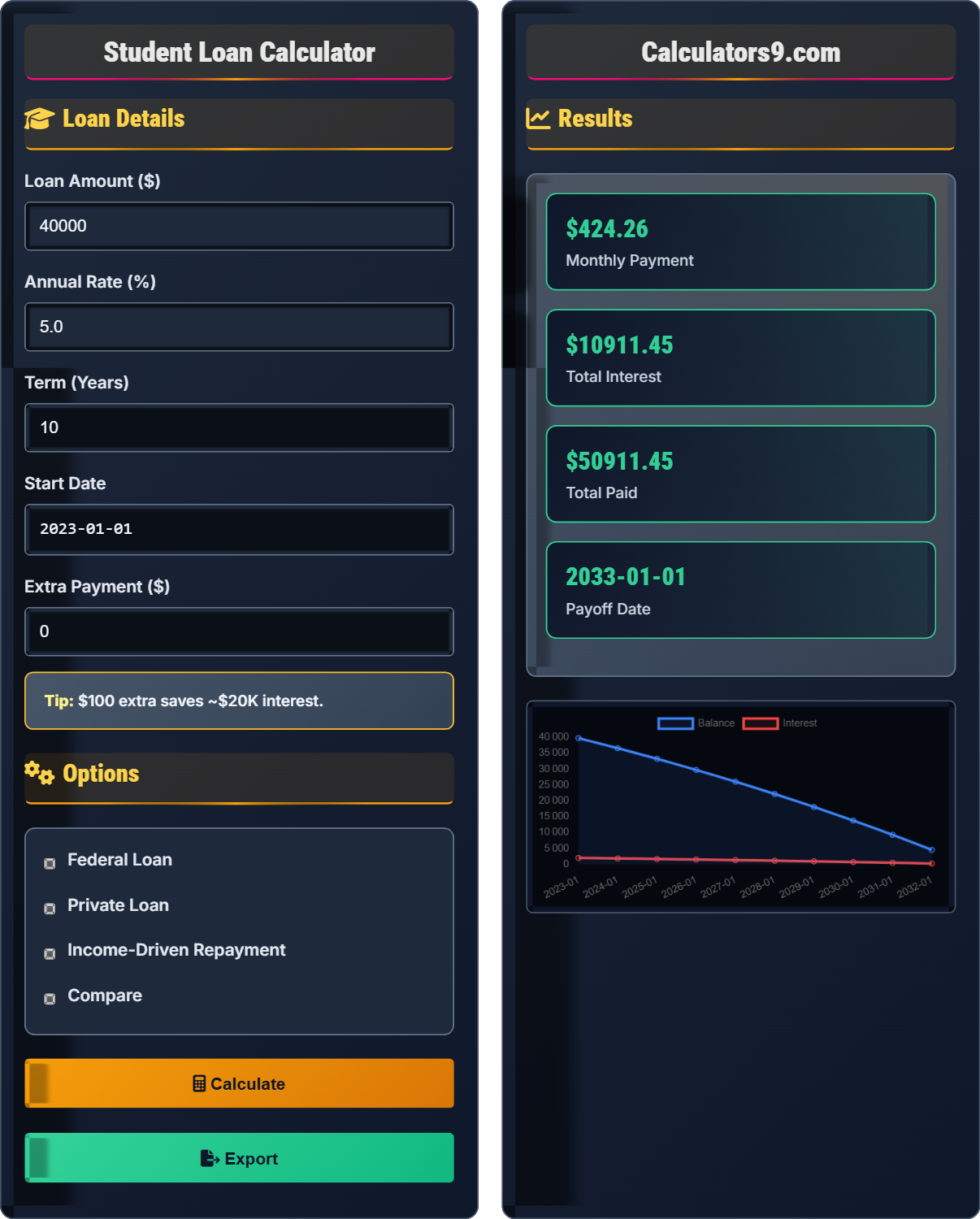

Example: For a loan of \( P = \$40{,}000 \) at an annual interest rate of 5.0% over 10 years:

Monthly interest rate: \( r = \frac{5.0\%}{12} = 0.004167 \)

Total payments: \( n = 10 \times 12 = 120 \)

Monthly payment:

\( M = 40{,}000 \times \frac{0.004167(1+0.004167)^{120}}{(1+0.004167)^{120} - 1} \approx \$424 \)

Thus, the borrower would pay approximately $424 per month for 10 years.

Loan Details

Options

Results

| Month | Payment | Principal | Interest | Balance |

|---|

| Year | Total | Principal | Interest | Balance |

|---|

Comprehensive Student Loan Guide

A student loan is a type of financial aid that must be repaid with interest. These loans help students pay for education expenses including tuition, fees, room and board, books, supplies, and transportation. Student loans can be federal (government-funded) or private (from banks, credit unions, or schools).

The standard student loan payment calculation uses the following formula:

Where:

- \(M\) = Monthly payment

- \(P\) = Principal loan amount

- \(r\) = Monthly interest rate (annual rate divided by 12)

- \(n\) = Total number of payments (loan term in years multiplied by 12)

Your monthly student loan payment typically includes:

- Principal: Portion that reduces the outstanding loan balance

- Interest: Cost of borrowing money, paid to the lender

- Origination Fees: For federal loans, a percentage of the loan amount

- Late Fees: Penalties for missed payments (avoidable)

Degree

Skills

Loans

Interest

Monthly Payments

Income

- Maximize federal loans first: Better terms and protections than private loans

- Consider income-driven plans: Lower payments based on earnings

- Make payments during grace period: Reduce interest capitalization

- Pay more than minimum: Reduces total interest paid

- Look into forgiveness programs: Public Service Loan Forgiveness, Teacher Loan Forgiveness

Student Loan Basics

Loan for educational expenses with repayment after graduation.

\(M = P\frac{r(1+r)^n}{(1+r)^n-1}\)

Where M=monthly payment, P=loan amount, r=monthly rate, n=payments.

- Interest calculated on remaining balance

- Federal loans have grace periods

- Income-driven plans adjust payments

Strategies

Payments based on income and family size.

- Choose federal over private loans

- Explore income-driven options

- Consider forgiveness programs

- Make extra payments when possible

- Federal loans offer deferment

- Private loans lack forgiveness options

- APR varies significantly

- Grace periods apply to federal loans

Student Loan Learning Quiz

Which of the following is TRUE about federal student loans compared to private student loans?

The answer is B) Federal loans offer income-driven repayment plans. Federal student loans provide several income-driven repayment options (IBR, PAYE, REPAYE, ICR) that adjust monthly payments based on income and family size. Private loans typically do not offer these flexible repayment options.

Understanding the differences between federal and private student loans is crucial for making informed borrowing decisions. Federal loans offer more flexible repayment options and borrower protections that private loans typically don't provide. This is why federal loans are generally recommended before considering private loans.

Federal Student Loans: Government-funded loans with standardized terms and protections

Income-Driven Repayment (IDR): Plans that adjust payments based on income and family size

Private Student Loans: Loans from banks and other lenders with varying terms

• Federal loans offer standardized protections

• Income-driven plans are exclusive to federal loans

• Private loans have more variable terms

• Exhaust federal loan options first

• Understand repayment options before borrowing

• Keep federal and private loans separate

• Assuming all loans are the same

• Not understanding repayment differences

• Borrowing private loans before exhausting federal options

Calculate the monthly payment for a $30,000 student loan at 4.5% annual interest over 15 years. Show your work.

Using the student loan formula: \(M = P\frac{r(1+r)^n}{(1+r)^n-1}\)

Given:

- P = $30,000

- r = 0.045 ÷ 12 = 0.00375

- n = 15 × 12 = 180

Step 1: Calculate (1+r)^n = (1.00375)^180 = 1.9672

Step 2: Calculate numerator: r(1+r)^n = 0.00375 × 1.9672 = 0.007377

Step 3: Calculate denominator: (1+r)^n - 1 = 1.9672 - 1 = 0.9672

Step 4: Calculate M = P × (numerator/denominator) = $30,000 × (0.007377/0.9672) = $30,000 × 0.007627 = $228.81

This problem demonstrates the calculation of student loan payments using the standard amortization formula. The longer repayment term results in lower monthly payments but higher total interest costs over the life of the loan. Students should consider both monthly affordability and total cost when choosing repayment terms.

Amortization: Gradual repayment of loan through regular payments

Monthly Rate: Annual interest rate divided by 12

Number of Payments: Loan term in years multiplied by 12

• Always convert annual rates to monthly rates for calculations

• Convert loan terms to months for accurate calculations

• The loan formula accounts for compound interest over time

• Remember: r = annual rate ÷ 12

• Remember: n = loan years × 12

• Use a calculator for complex exponent calculations

• Forgetting to convert annual rates to monthly rates

• Using the wrong number of payments (not converting years to months)

• Making calculation errors with large exponents

Alex takes out a 10-year student loan for $50,000 at an interest rate of 6.0%. His monthly payment is $555. What is the total interest he will pay over the life of the loan?

Step 1: Calculate total number of payments = 10 years × 12 months/year = 120 payments

Step 2: Calculate total amount paid = $555 × 120 = $66,600

Step 3: Calculate total interest = Total paid - Principal = $66,600 - $50,000 = $16,600

Therefore, Alex will pay $16,600 in interest over the life of his loan.

This example shows how interest adds significantly to the total cost of a student loan. In this case, Alex will pay 33% more than the original loan amount due to interest charges. This demonstrates why it's important to consider both monthly payments and total interest costs when evaluating loan options and why making extra payments can result in significant savings.

Total Interest: The sum of all interest payments over the life of the loan

Loan Term: The length of time to repay the loan

Principal: The original loan amount

• Total interest = (Monthly payment × Number of payments) - Principal

• Longer loan terms result in more total interest paid

• Higher interest rates increase total interest significantly

• Remember: Total paid = Monthly payment × Total number of payments

• Total interest is always Total paid minus Principal

• Use this calculation to compare different loan scenarios

• Forgetting to multiply monthly payment by total number of payments

• Subtracting the wrong amounts when calculating interest

• Confusing monthly interest with total interest over the loan term

Sarah has $60,000 in federal student loans at 5.5% interest with a standard 10-year repayment plan requiring $636 monthly payments. She qualifies for an Income-Driven Repayment plan that sets her payments at 10% of discretionary income. If her annual income is $45,000 and the poverty guideline for her family size is $25,000, what would her monthly payment be under IDR? (Discretionary income = Annual income - 150% of poverty guideline)

Step 1: Calculate poverty guideline adjustment = 150% × $25,000 = $37,500

Step 2: Calculate discretionary income = $45,000 - $37,500 = $7,500

Step 3: Calculate IDR monthly payment = ($7,500 ÷ 12) × 10% = $625 × 10% = $62.50

Step 4: Compare to standard payment: $62.50 vs $636 monthly

Therefore, Sarah's monthly payment under IDR would be $62.50, a reduction of $573.50 per month.

This demonstrates how income-driven repayment plans can dramatically reduce monthly payments for borrowers with lower incomes relative to their debt burden. The IDR payment is based on income and family size rather than loan balance, which can result in payments that don't cover accruing interest. This may lead to negative amortization where the loan balance grows over time.

Income-Driven Repayment (IDR): Plans that set payments based on income and family size

Discretionary Income: Income above 150% of poverty guidelines

Negative Amortization: When payments don't cover accruing interest

• IDR payments are based on income, not loan balance

• May result in negative amortization

• Forgiveness possible after 20-25 years

• Calculate potential IDR payments before borrowing

• Consider career path and earning potential

• Understand forgiveness requirements

• Not understanding how IDR affects total interest

• Forgetting to recertify income annually

• Assuming all loans qualify for IDR

Which of the following statements about Public Service Loan Forgiveness (PSLF) is TRUE?

The answer is B) PSLF requires employment with a qualifying employer. Public Service Loan Forgiveness requires working full-time for a qualifying employer (government or non-profit organization) while making 120 qualifying monthly payments (10 years). The program only applies to federal student loans, not private loans.

Public Service Loan Forgiveness is a valuable program for those working in public service careers, but it has strict requirements. Borrowers must be employed by qualifying organizations and make payments under qualifying repayment plans. The program only forgives federal loans, not private loans, and requires careful tracking of qualifying payments.

Public Service Loan Forgiveness (PSLF): Program forgiving federal loans after 10 years of qualifying payments

Qualifying Employer: Government or non-profit organization

Qualifying Payments: Payments made under eligible repayment plans

• Requires 120 qualifying payments (10 years)

• Employment must be with qualifying organization

• Verify employer qualification before relying on PSLF

• Track qualifying payments carefully

• Submit employment certification annually

• Assuming private loans qualify for PSLF

• Not tracking qualifying payments properly

• Working for non-qualifying employers

FAQ

Q: How do income-driven repayment plans affect my student loan payments?

A: Income-driven repayment (IDR) plans cap your monthly payment at a percentage of your discretionary income (usually 10-20%), which can be significantly lower than standard payments.

For example, with an income of $40,000 and the poverty guideline of $27,750 (for a family of 2 in 2023), your discretionary income would be $40,000 - $41,625 = $0 (since it's negative, payment would be $0 under PAYE).

Mathematically, if \( I \) is annual income and \( P \) is poverty guideline:

\( \text{Discretionary Income} = \max(0, I - 1.5P) \)

For a graduate with $50,000 income: \( \text{Payment} = \frac{50{,}000 - 41{,}625}{12} \times 10\% = \$69.79 \)

This compares to a standard payment of approximately $500+ for similar loan amounts.

Q: Should I pursue Public Service Loan Forgiveness or pay off loans faster?

A: The decision depends on your loan balance relative to your income.

- PSLF route: If you have $60,000 in loans and earn $50,000, payments under PAYE would be about $160/month. Over 10 years, you'd pay $19,200 and have $40,000+ forgiven.

- Payoff route: Standard payments would be $650+/month. You'd pay about $35,000+ in total over 5 years.

If forgiveness exceeds what you'd pay under standard plans, PSLF is financially advantageous. However, you must commit to public service for 10 years and meet all requirements.