Cash Back or Low Interest Calculator

Auto financing decision tool • 2026

Cash Back vs Low Interest Formula:

Show the calculator\( \text{Monthly Payment} = \frac{P \times r \times (1+r)^n}{(1+r)^n - 1} \)

Where:

- \( P \) = Principal loan amount (after cash back if applicable)

- \( r \) = Monthly interest rate (annual rate divided by 12)

- \( n \) = Total number of payments (loan term in months)

To compare options:

- Cash Back Option: Principal = Vehicle Price - Cash Back Amount

- Low Interest Option: Principal = Vehicle Price, but with lower interest rate

This formula calculates the fixed monthly payment for an installment loan. To decide between cash back and low interest, calculate the total cost of each option over the loan term. The option with the lower total cost is financially superior.

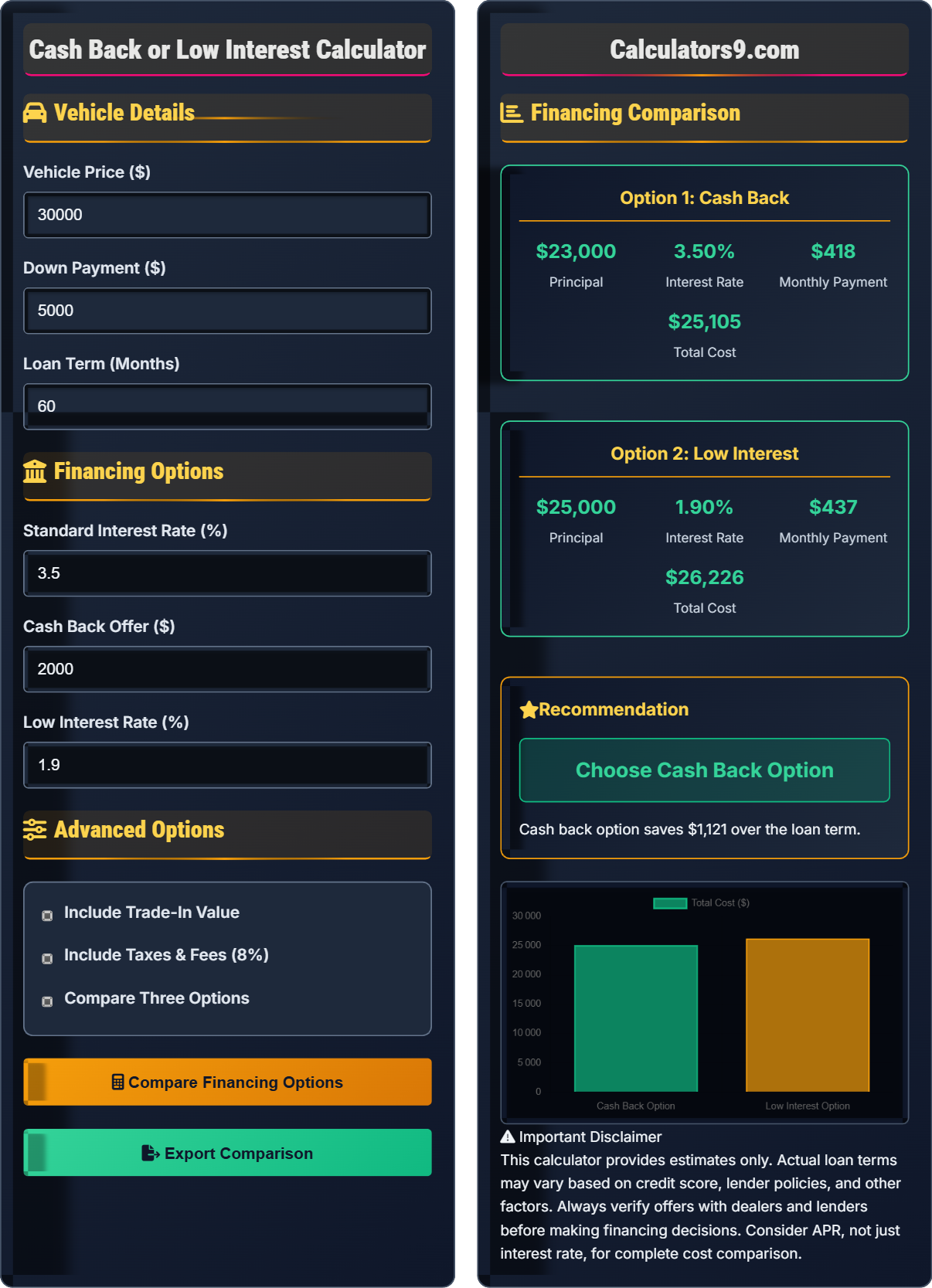

Example: For a $30,000 vehicle with $2,000 cash back or 1.9% interest (vs 3.5% standard rate) over 60 months:

Cash Back Option: Principal = $28,000, Rate = 3.5%/12, Monthly Payment ≈ $508

Low Interest Option: Principal = $30,000, Rate = 1.9%/12, Monthly Payment ≈ $524

Total Cost Cash Back: $508 × 60 = $30,480

Total Cost Low Interest: $524 × 60 = $31,440

In this case, cash back saves $960 over the loan term.

Vehicle Details

Financing Options

Advanced Options

Financing Comparison

Calculating savings difference...

This calculator provides estimates only. Actual loan terms may vary based on credit score, lender policies, and other factors. Always verify offers with dealers and lenders before making financing decisions. Consider APR, not just interest rate, for complete cost comparison.

Financing Basics

When financing a vehicle, manufacturers often offer two promotional options: a cash back rebate or a low interest rate. The choice between these options can significantly impact your total cost and monthly payments.

Where P = Principal (loan amount), r = monthly interest rate, n = number of payments.

- Cash back reduces the principal loan amount

- Low interest keeps principal high but reduces interest charges

- Shorter loan terms favor cash back

- Higher loan amounts favor low interest

- Always compare total cost, not just monthly payments

Decision Factors

The optimal choice depends on several factors including loan amount, term length, and the difference between rates.

| Factor | Favors Cash Back | Favors Low Interest |

|---|---|---|

| Loan Amount | Smaller loans | Larger loans |

| Loan Term | Shorter terms (36-48 mo) | Longer terms (60+ mo) |

| Rate Difference | Small differences (0.5-1%) | Large differences (1.5%+) |

| Cash Back Amount | Large rebates | Small rebates |

| Interest Rate Level | Already low rates | Higher standard rates |

- Quick Rule: If cash back × loan term in years > loan amount × rate difference, choose cash back

- For Small Loans: Cash back often wins due to immediate reduction

- For Large Loans: Low interest typically saves more over time

- For Long Terms: Low interest compounds to greater savings

Maximizing Savings

Maximize your savings beyond the basic cash back vs low interest decision.

Negotiate Further

Reduce price before applying incentives

Improve Credit Score

Qualify for better rates

Shorter Term

Less interest over life

Shop Around

Compare lenders

- Don't finance for more than 80% of vehicle value

- Keep monthly payments under 15% of gross income

- Consider total cost, not just monthly payment

- Read all loan terms carefully

- Understand prepayment penalties

Financing Decision Learning Quiz

When deciding between cash back and low interest, which factor is most important to consider?

The answer is B) Total cost over loan term. While monthly payments are important for cash flow, the total cost determines the actual savings over the life of the loan. A lower monthly payment might result in higher total interest paid over time.

Many consumers focus solely on monthly payments, but this can lead to poor financial decisions. The total cost calculation considers both the principal reduction (via cash back) and interest savings (via low rate) over the entire loan period. For example, a $50 lower monthly payment over 60 months equals $3,000 in savings, but if cash back would save more than that, it's the better choice.

Total Cost: Sum of all payments over loan term

Monthly Payment: Amount paid each month

Loan Term: Duration of the loan

• Compare total costs, not monthly payments

• Consider loan term in decision-making

• Factor in both principal and interest

• Calculate total payments: Monthly × Number of months

• Use the calculator to compare both options

• Don't be misled by lower monthly payments

• Focusing only on monthly payment

• Ignoring total interest paid

• Not considering loan term effect

Calculate the monthly payment for a $25,000 loan at 3.5% annual interest over 60 months. Show your work.

Step 1: Convert annual rate to monthly

Monthly rate (r) = 3.5% ÷ 12 = 0.035 ÷ 12 = 0.002917

Step 2: Identify variables

Principal (P) = $25,000

Number of payments (n) = 60

Step 3: Apply the formula

Monthly Payment = P × r × (1+r)^n ÷ [(1+r)^n - 1]

(1+r)^n = (1.002917)^60 = 1.1909

Monthly Payment = $25,000 × 0.002917 × 1.1909 ÷ (1.1909 - 1)

= $87.09 ÷ 0.1909 = $456.18

Therefore, the monthly payment is approximately $456.18.

This calculation demonstrates the standard loan payment formula. The key is converting the annual interest rate to a monthly rate and using the correct number of payments. The formula accounts for compound interest over the loan term. Understanding this calculation helps evaluate financing offers accurately.

Principal: Initial loan amount

Monthly Rate: Annual rate divided by 12

Compound Interest: Interest on interest

• Convert annual rate to monthly rate

• Use correct number of payments

• Account for compound interest

• Remember: r = annual rate ÷ 12

• Use calculator for exponent calculations

• Verify with online loan calculators

• Forgetting to convert annual to monthly rate

• Using wrong number of payments

• Calculation errors with exponents

You're buying a $35,000 car with $7,000 down payment. The dealer offers either $3,000 cash back or 2.5% interest (instead of standard 4.0%). The loan term is 60 months. Which option saves more money over the loan term?

Step 1: Calculate loan amounts

Standard loan amount: $35,000 - $7,000 = $28,000

Cash back loan amount: $28,000 - $3,000 = $25,000

Low interest loan amount: $28,000

Step 2: Calculate monthly payments

Cash back monthly payment (4.0%): $25,000 × 0.04/12 × (1.003333)^60 ÷ [(1.003333)^60 - 1] ≈ $462

Low interest monthly payment (2.5%): $28,000 × 0.025/12 × (1.002083)^60 ÷ [(1.002083)^60 - 1] ≈ $497

Step 3: Calculate total costs

Cash back total: $462 × 60 = $27,720

Low interest total: $497 × 60 = $29,820

Step 4: Calculate savings

Savings with cash back: $29,820 - $27,720 = $2,100

Therefore, cash back saves $2,100 over the loan term.

This problem demonstrates how cash back can be superior despite a higher interest rate. The immediate principal reduction of $3,000 outweighs the interest savings from the lower rate. This is especially true for shorter loan terms where interest has less time to compound.

Principal Reduction: Immediate decrease in loan amount

Interest Savings: Reduced interest charges over time

Compounding Effect: How interest builds over time

• Calculate total cost for each option

• Consider both principal and interest effects

• Time value of money matters

• Larger cash back favors cash back option

• Longer terms favor low interest

• Use calculator for complex comparisons

• Not calculating total costs

• Confusing monthly vs. total savings

• Ignoring loan term effect

You're considering a $40,000 car with $10,000 down payment. You have three options: (1) $2,500 cash back with 3.5% rate, (2) 1.5% rate with no cash back, or (3) $1,500 cash back with 2.0% rate. The loan term is 72 months. Which option gives the lowest total cost?

Step 1: Calculate loan amounts for each option

Base loan amount: $40,000 - $10,000 = $30,000

Option 1: $30,000 - $2,500 = $27,500 at 3.5%

Option 2: $30,000 at 1.5%

Option 3: $30,000 - $1,500 = $28,500 at 2.0%

Step 2: Calculate monthly payments

Option 1: $27,500 at 3.5% over 72 months ≈ $440/month

Option 2: $30,000 at 1.5% over 72 months ≈ $442/month

Option 3: $28,500 at 2.0% over 72 months ≈ $431/month

Step 3: Calculate total costs

Option 1 total: $440 × 72 = $31,680

Option 2 total: $442 × 72 = $31,824

Option 3 total: $431 × 72 = $31,032

Step 4: Compare and decide

Option 3 has the lowest total cost at $31,032.

This problem shows how to compare multiple financing options systematically. With longer terms (72 months), the low interest rate has more time to compound, making Option 3 the winner despite the smaller cash back. The key is to calculate total cost for each option and compare.

Systematic Comparison: Calculating same metric for all options

Compound Effect: How longer terms amplify interest differences

Optimal Choice: Lowest total cost option

• Calculate identical metrics for all options

• Longer terms favor low interest

• Compare total costs, not monthly payments

• Organize calculations in a table

• Use consistent calculation method

• Consider multiple factors simultaneously

• Inconsistent calculation methods

• Comparing different metrics

• Not considering all options equally

Which statement about cash back vs low interest financing is TRUE?

The answer is C) The better option depends on loan amount, term, and rate difference. There's no universal rule - the optimal choice varies based on the specific combination of loan amount, term length, and the difference between interest rates. Small loans with short terms often favor cash back, while large loans with long terms often favor low interest.

The cash back vs low interest decision is nuanced and depends on multiple variables. No single factor determines the best choice. The interaction between loan amount, term length, and rate differential creates different outcomes. This is why using a calculator to model specific scenarios is essential for making the optimal decision.

Variable Interaction: How multiple factors affect outcome

Scenario Modeling: Testing specific situations

Context-Dependent: Outcome varies by situation

• No universal rule exists

• Multiple factors interact

• Individual situation matters

• Model your specific situation

• Consider multiple variables

• Use calculator for accurate comparison

• Assuming one option always wins

• Not considering all variables

• Making generalizations

FAQ

Q: Can I negotiate further after choosing cash back or low interest?

A: Yes, you can often negotiate further! The cash back vs low interest decision is separate from the vehicle price negotiation. Here's how:

- Price Negotiation: Negotiate the vehicle price first, then apply the incentive

- Combination Offers: Some dealers may offer partial cash back plus a reduced rate

- Additional Perks: Warranty extensions, maintenance packages, or accessories

- Trade-In Value: Negotiate separately from financing

Remember, incentives are marketing tools. The dealer's goal is to sell the car. If you're willing to buy, they often have flexibility beyond the stated offers. Always calculate your total cost after all negotiations.

Q: How does my credit score affect the cash back vs low interest decision?

A: Your credit score significantly impacts both the availability and terms of financing options:

- High Credit Score (720+): Qualify for manufacturer low-rate programs

- Medium Credit Score (620-719): May have limited access to promotional rates

- Lower Credit Score (Below 620): May not qualify for either option

For those with excellent credit, low interest rates become more attractive because you're already getting good rates. For those with lower credit scores, cash back might be more valuable since your baseline rate is higher. The rate difference between promotional and standard rates is often greater for lower credit tiers, potentially making cash back more beneficial.