Payment Calculator

Loan payment & amortization calculator • 2026

Payment Formula:

Show the calculator\( \text{Payment} = \frac{P \times r \times (1+r)^n}{(1+r)^n - 1} \)

Where:

- \( P \) = Principal loan amount

- \( r \) = Monthly interest rate (annual rate ÷ 12)

- \( n \) = Total number of payments (loan term in years × 12)

This formula calculates the fixed monthly payment required to fully pay off a loan over the specified term, taking into account compound interest. The payment includes both principal and interest components that change over time.

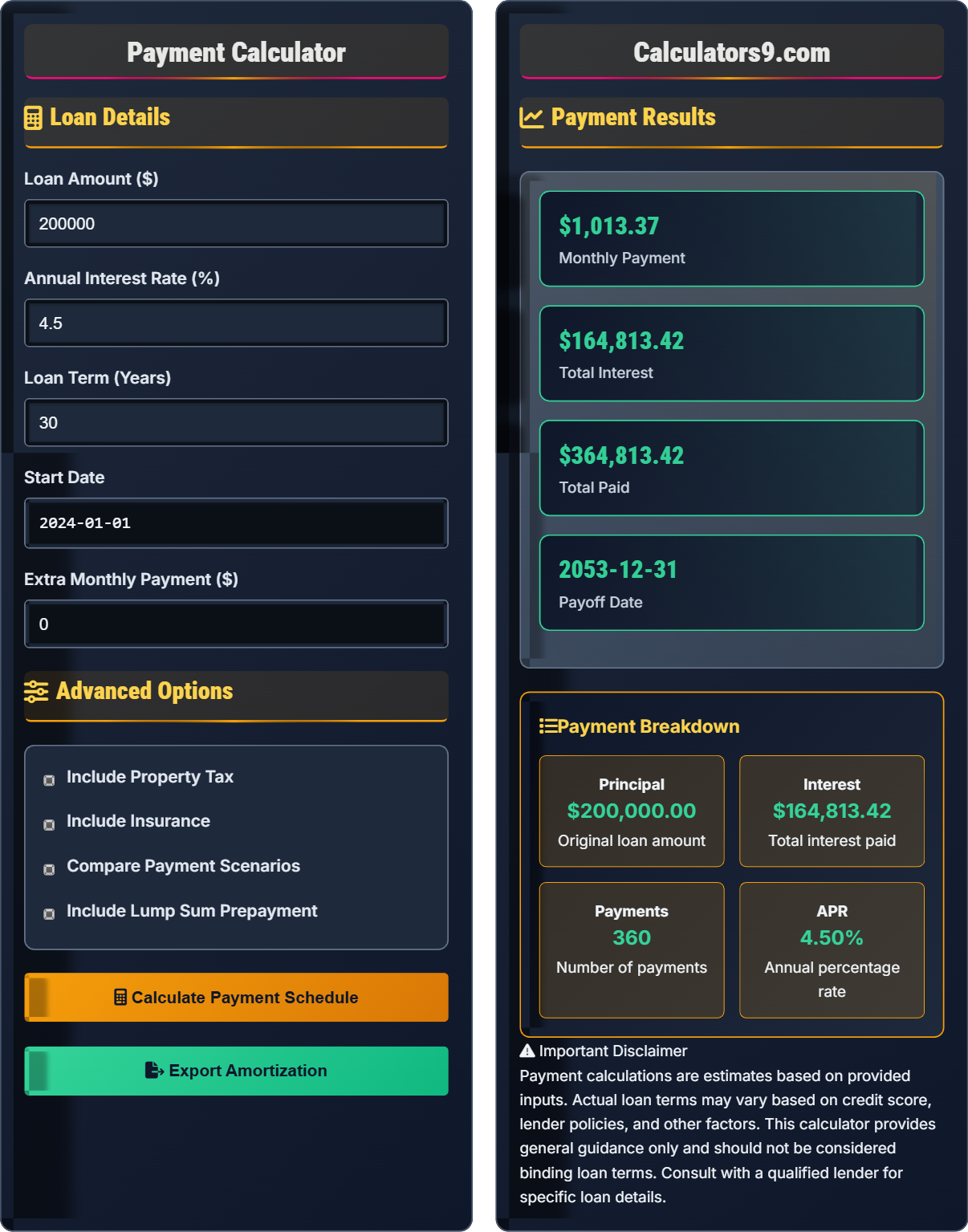

Example: For a $200,000 loan at 4.5% annual interest over 30 years:

\( r = \frac{4.5\%}{12} = 0.00375 \)

\( n = 30 \times 12 = 360 \)

\( \text{Payment} = \frac{200,000 \times 0.00375 \times (1.00375)^{360}}{(1.00375)^{360} - 1} \)

\( \text{Payment} = \frac{200,000 \times 0.00375 \times 3.847}{3.847 - 1} = \frac{2,885.25}{2.847} = \$1,013.46 \)

Monthly payment: $1,013.46

Loan Details

Advanced Options

Payment Results

Principal

Original loan amount

Interest

Total interest paid

Payments

Number of payments

APR

Annual percentage rate

| Payment # | Date | Payment | Principal | Interest | Balance |

|---|

| Year | Principal Paid | Interest Paid | Remaining Balance |

|---|

Payment calculations are estimates based on provided inputs. Actual loan terms may vary based on credit score, lender policies, and other factors. This calculator provides general guidance only and should not be considered binding loan terms. Consult with a qualified lender for specific loan details.

Payment Basics

Loan payments consist of both principal and interest components that change over time. Early payments are mostly interest, while later payments are mostly principal.

Where P = principal, r = monthly rate, n = number of payments.

- Early payments are mostly interest

- Later payments are mostly principal

- Fixed payments for standard loans

- Extra payments reduce total interest

- Prepayments accelerate loan payoff

Payment Strategies

Several strategies can reduce total interest and accelerate loan payoff.

| Strategy | Impact | Example Savings | Application |

|---|---|---|---|

| Extra Monthly Payments | Reduces principal | $32,000+ saved | Any loan type |

| Bi-weekly Payments | 13th payment annually | $25,000+ saved | Fixed-rate loans |

| Lump Sum Prepayment | Immediate principal reduction | $50,000+ saved | Available funds |

| Refinancing | Lower rate/term | $100,000+ saved | Rate improvement |

| Round Up Payments | Small principal reduction | $15,000+ saved | Any loan |

- Start Early: Maximum interest savings

- Consistency: Regular extra payments

- Timing: Pay early in loan term

- Documentation: Ensure extra payments go to principal

- Review: Adjust strategy as needed

Amortization Insights

Amortization spreads loan payments over time, with changing principal and interest components.

Early Years

Most payments go to interest

Middle Years

Equal principal/interest

Final Years

Most payments reduce balance

Payoff

Final payments eliminate balance

- Interest is front-loaded in payments

- Principal reduction accelerates over time

- Extra payments have greatest impact early

- Amortization schedule shows payment breakdown

- Refinancing resets amortization

Payment Calculation Learning Quiz

In the early years of a loan, what percentage of each payment typically goes to interest?

The answer is C) 70-80%. In the early years of a loan, most of each payment goes toward interest rather than principal. For example, in a 30-year mortgage, the first payment might allocate about 80% to interest and 20% to principal.

This occurs because interest is calculated on the outstanding principal balance. Since the principal is highest at the beginning of the loan, the interest component of each payment is also highest. As payments are made and principal is reduced, more of each subsequent payment goes toward principal rather than interest.

Amortization: Spreading payments over time

Front-Loaded Interest: Higher interest in early payments

Principal Reduction: Decreasing loan balance

• Interest calculated on remaining principal

• Early payments mostly interest

• Later payments mostly principal

• Make extra payments early in loan term

• Interest is highest when balance is highest

• Principal reduction accelerates over time

• Expecting early payments to reduce principal significantly

• Not understanding front-loaded interest

• Believing payments are evenly split throughout

Calculate the monthly payment for a $150,000 loan at 3.75% annual interest over 20 years. Show your work.

Using the payment formula: \( \text{Payment} = \frac{P \times r \times (1+r)^n}{(1+r)^n - 1} \)

Where:

- P = $150,000 (principal)

- r = 0.0375 ÷ 12 = 0.003125 (monthly rate)

- n = 20 × 12 = 240 (number of payments)

Step 1: Calculate (1+r)^n

(1.003125)^240 = 2.114

Step 2: Calculate numerator

$150,000 × 0.003125 × 2.114 = $991.88

Step 3: Calculate denominator

2.114 - 1 = 1.114

Step 4: Calculate payment

$991.88 ÷ 1.114 = $889.84

Therefore, the monthly payment is $889.84.

This calculation demonstrates how to use the standard loan payment formula. The key is correctly converting the annual interest rate to a monthly rate and calculating the total number of payments. The formula accounts for compound interest over the loan term, ensuring the loan is fully paid off by the end of the term.

Monthly Rate: Annual rate divided by 12

Number of Payments: Loan term in years × 12Compound Interest: Interest calculated on principal and accrued interest

• Convert annual rate to monthly rate

• Calculate correct number of payments

• Account for compound interest

• r = annual rate ÷ 12

• n = years × 12

• Use calculator for exponent calculations

• Forgetting to convert annual to monthly rate

• Using wrong number of payments

• Calculation errors with exponents

Sarah has a $250,000 mortgage at 4.25% for 30 years with a monthly payment of $1,229. If she pays an extra $200 each month, how much interest will she save over the life of the loan?

Step 1: Calculate original total interest

Monthly payment: $1,229

Total payments: $1,229 × 360 = $442,440

Total interest: $442,440 - $250,000 = $192,440

Step 2: Calculate with extra payments

With extra $200, the loan will be paid off earlier

Using amortization calculations, the loan is paid off in approximately 24 years (288 payments)

Total paid with extra payments: $1,229 × 288 = $353,952

Step 3: Calculate interest savings

Interest savings: $192,440 - ($353,952 - $250,000) = $192,440 - $103,952 = $88,488

Therefore, Sarah saves approximately $88,488 in interest.

Extra payments directly reduce the principal balance, which decreases the amount of interest charged in subsequent periods. This creates a compounding effect where each extra payment saves interest on all future payments. The earlier the extra payments are made, the greater the savings due to the front-loaded interest structure.

Principal Reduction: Decrease in loan balance

Interest Savings: Money saved by paying down principal

Compounding Effect: Savings on future interest

• Extra payments reduce principal immediately

• Lower principal reduces future interest

• Even small extra payments create significant savings

• Make extra payments early in loan term

• Ensure extra payments go to principal

• Not understanding compounding effect of extra payments

• Making extra payments late in loan term

• Not confirming extra payments go to principal

John has a $300,000 mortgage at 5.5% for 30 years with 25 years remaining. His current payment is $1,740. He can refinance to a 15-year loan at 3.75%. What would be his new monthly payment and total interest savings?

Step 1: Calculate remaining balance after 5 years

Using amortization, after 60 payments on original loan, remaining balance ≈ $279,000

Step 2: Calculate new payment

New loan: $279,000 at 3.75% for 15 years

Monthly rate: 0.0375 ÷ 12 = 0.003125

Number of payments: 15 × 12 = 180

New payment = $279,000 × 0.003125 × (1.003125)^180 ÷ [(1.003125)^180 - 1]

New payment ≈ $2,018

Step 3: Calculate interest savings

Original remaining interest: $1,740 × 300 - $279,000 = $243,000

New interest: $2,018 × 180 - $279,000 = $84,240

Interest savings: $243,000 - $84,240 = $158,760

Therefore, new payment is $2,018 with $158,760 in interest savings.

Refinancing can significantly reduce total interest by lowering the rate and/or shortening the term. However, it typically increases monthly payments due to the shorter term. The key is calculating the net benefit by comparing total interest costs. Consider closing costs when evaluating refinancing options.

Refinancing: Replacing existing loan with new terms

Remaining Balance: Principal left on original loan

Net Benefit: Savings minus costs

• Calculate remaining balance before refinancing

• Consider closing costs in decision

• Compare total interest costs

• Refinance when rate drops by 1% or more

• Consider break-even point

• Factor in closing costs

• Not considering closing costs

• Refinancing too frequently

• Ignoring break-even period

How does switching from monthly to bi-weekly payments affect a 30-year mortgage?

The answer is B) Adds an extra payment each year. Bi-weekly payments mean paying half the monthly payment every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments (equivalent to 13 full payments) instead of 12 monthly payments, adding one extra payment per year.

Bi-weekly payments accelerate loan payoff by effectively making one additional payment per year. The extra payment goes directly to principal, reducing the balance and subsequent interest charges. This strategy can significantly reduce total interest and shorten the loan term without dramatically changing monthly cash flow.

Bi-weekly Payments: Every two weeks (26 times per year)

Extra Payment: Additional principal reduction

Accelerated Payoff: Shortened loan term

• Bi-weekly = 26 payments per year

• Equivalent to 13 monthly payments

• One extra payment annually

• Half monthly payment every two weeks

• Creates 13th payment annually

• Significant interest savings

• Thinking bi-weekly doubles monthly payment

• Not understanding the extra payment effect

• Confusing frequency with amount

FAQ

Q: How much can I save by making extra principal payments?

A: The savings from extra principal payments depend on your loan balance, interest rate, and timing:

- Small Extra Payments: $100 extra monthly on a $200K loan at 4.5% saves ~$30K interest and 4 years

- Large Extra Payments: $500 extra monthly saves ~$120K interest and 10+ years

- Timing Matters: Extra payments in first 10 years have maximum impact

The formula for interest savings is complex, but generally, the earlier you make extra payments, the more interest you save due to the front-loaded interest structure of amortizing loans. Each extra payment reduces your principal balance immediately, which reduces interest charges for all future payments.

Q: When does refinancing make financial sense?

A: Refinancing typically makes sense when:

- Rate Drop: New rate is 1% or more below current rate

- Break-Even: Closing costs recovered within 2-3 years

- Term Reduction: Shortening loan term significantly

- Financial Stability: Secure employment/income

Example calculation: If closing costs are $3,000 and monthly savings are $150, break-even is 20 months ($3,000 ÷ $150). If you plan to stay in the home longer than the break-even period, refinancing makes financial sense. Consider your long-term plans and the total cost of the new loan.