Savings Calculator

Compound interest & goal planning tool • 2026

Savings Formula:

Show the calculator\( \text{Future Value} = PV \times (1 + r)^n + PMT \times \left(\frac{(1 + r)^n - 1}{r}\right) \)

Where:

- \( PV \) = Present value (initial deposit)

- \( PMT \) = Periodic payment (monthly deposit)

- \( r \) = Periodic interest rate (annual rate ÷ 12)

- \( n \) = Number of periods (months)

This formula calculates the future value of a savings account with regular deposits and compound interest. The first term represents growth of the initial deposit, while the second term represents growth of recurring deposits.

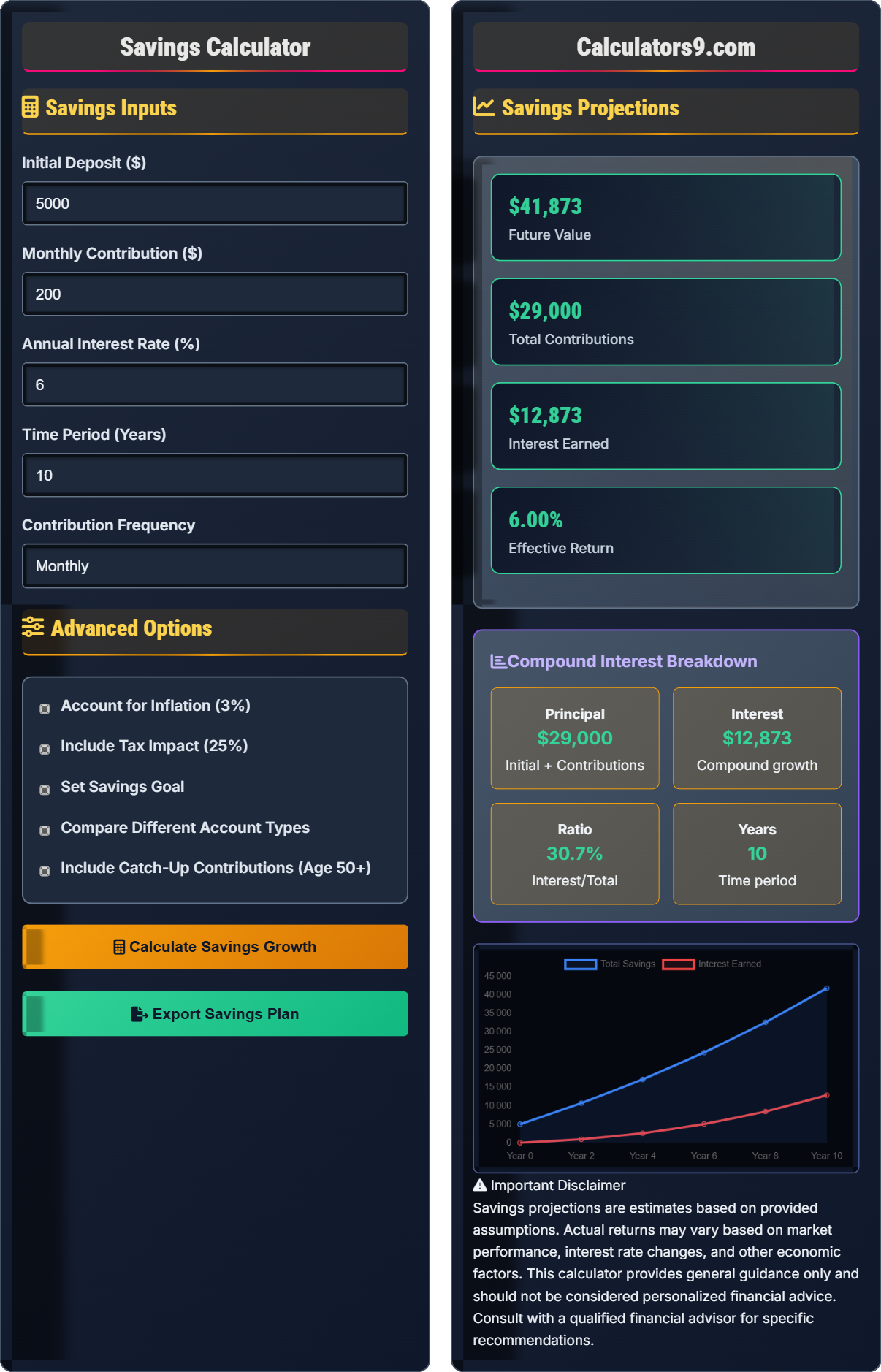

Example: For $5,000 initial deposit, $200 monthly contributions, 6% annual interest over 10 years:

\( r = \frac{6\%}{12} = 0.005 \)

\( n = 10 \times 12 = 120 \)

\( \text{Future Value} = 5000 \times (1.005)^{120} + 200 \times \left(\frac{(1.005)^{120} - 1}{0.005}\right) \)

\( = 5000 \times 1.819 + 200 \times 163.879 = 9,095 + 32,776 = \$41,871 \)

Total contributions: $5,000 + ($200 × 120) = $29,000

Interest earned: $41,871 - $29,000 = $12,871

Savings Inputs

Advanced Options

Savings Projections

Principal

Initial + Contributions

Interest

Compound growth

Ratio

Interest/Total

Years

Time period

Savings projections are estimates based on provided assumptions. Actual returns may vary based on market performance, interest rate changes, and other economic factors. This calculator provides general guidance only and should not be considered personalized financial advice. Consult with a qualified financial advisor for specific recommendations.

Savings Fundamentals

Compound interest is the process where interest earned on an investment generates its own interest over time. This creates exponential growth rather than linear growth.

- Time is Your Friend: The longer money is invested, the more dramatic the effect

- Consistent Contributions: Regular additions accelerate growth

- Higher Rates: Small differences in rates compound to large differences

- Early Start: Starting early maximizes compounding effect

- Save at least 10-20% of income

- Start saving as early as possible

- Automate savings contributions

- Choose appropriate account types

- Minimize fees and taxes

Savings Strategies

Different strategies work for different goals and time horizons.

| Strategy | Best For | Typical Return | Access | Risk Level |

|---|---|---|---|---|

| Emergency Fund | Short-term needs | 0.05-4.5% | High | Very Low |

| High-Yield Savings | Medium-term goals | 4-5% | High | Low |

| CDs | Fixed-term savings | 3-5% | Low | Low |

| IRAs | Retirement | 5-8% | Medium | Medium |

| Index Funds | Long-term growth | 7-10% | Medium | Medium-High |

- Pay Yourself First: Set up automatic transfers

- Round Up Purchases: Use apps that round up transactions

- 52-Week Challenge: Save increasing amounts each week

- Side Hustle: Direct extra income to savings

- Windfall Strategy: Automatically save bonuses, refunds

Goal Planning

Setting specific, measurable goals helps maintain motivation and track progress.

Emergency Fund

of expenses

Down Payment

of home price

Retirement

of income

Education

tax-advantaged

- Set specific numeric targets

- Establish realistic timelines

- Create separate accounts for different goals

- Review and adjust goals annually

- Track progress regularly

Savings Planning Learning Quiz

Which statement about compound interest is TRUE?

The answer is B) Interest is calculated on principal plus previously earned interest. Compound interest is the process where interest earned on an investment generates its own interest over time. Each period's interest is calculated on the previous period's principal plus accumulated interest, leading to exponential growth.

Compound interest differs from simple interest, where interest is only calculated on the original principal. With compound interest, your money earns interest on interest, creating an accelerating growth effect. This is why starting to save early is so important - even small amounts can grow significantly over long periods due to compounding.

Compound Interest: Interest calculated on principal and accumulated interest

Exponential Growth: Growth that accelerates over time

Principal: Original investment amount

• Interest compounds on previous interest earnings

• Time significantly amplifies compounding effect

• Higher rates accelerate growth

• Start saving as early as possible

• Reinvest dividends and interest

• Use the "Rule of 72" to estimate doubling time

• Confusing compound with simple interest

• Underestimating time's impact

• Not reinvesting earnings

Calculate the future value of $3,000 initial deposit plus $150 monthly contributions at 5% annual interest over 15 years. Show your work.

Using the compound interest formula: \( FV = PV \times (1 + r)^n + PMT \times \left(\frac{(1 + r)^n - 1}{r}\right) \)

Where:

- PV = $3,000 (initial deposit)

- PMT = $150 (monthly contribution)

- r = 0.05 ÷ 12 = 0.004167 (monthly rate)

- n = 15 × 12 = 180 (number of months)

Step 1: Calculate growth of initial deposit

$3,000 × (1.004167)^180 = $3,000 × 2.114 = $6,342

Step 2: Calculate growth of monthly contributions

(1.004167)^180 = 2.114

(2.114 - 1) ÷ 0.004167 = 267.24

$150 × 267.24 = $40,086

Step 3: Calculate total future value

$6,342 + $40,086 = $46,428

Therefore, the future value is $46,428.

This calculation demonstrates how both the initial deposit and regular contributions grow over time. The formula accounts for compound interest on the initial amount plus the growing value of regular contributions. The regular contributions often contribute more to the final value than the initial deposit due to the compounding effect over time.

Future Value: Value of investment at future date

Regular Contributions: Consistent periodic depositsCompound Growth: Exponential increase in value

• Convert annual rate to monthly rate

• Calculate number of periods correctly

• Account for both initial and regular deposits

• Use calculator for exponent calculations

• Break down complex formulas into steps

• Verify with online savings calculators

• Forgetting to convert annual to monthly rate

• Not accounting for regular contributions

• Calculation errors with exponents

Mike earns $60,000 annually and has monthly expenses of $3,200. He wants to build an emergency fund that covers 6 months of expenses. How much should he save monthly to reach this goal in 2 years?

Step 1: Calculate emergency fund target

Monthly expenses: $3,200

Months to cover: 6

Emergency fund target: $3,200 × 6 = $19,200

Step 2: Calculate monthly savings needed

Time frame: 2 years = 24 months

Monthly savings: $19,200 ÷ 24 = $800

Step 3: Calculate percentage of income

Monthly income: $60,000 ÷ 12 = $5,000

Percentage: ($800 ÷ $5,000) × 100 = 16%

Therefore, Mike should save $800 per month (16% of income).

This problem demonstrates the importance of setting specific savings goals. Emergency funds provide financial security for unexpected expenses. The calculation shows that saving for an emergency fund requires a significant portion of income, highlighting the importance of starting with smaller goals and building up gradually.

Emergency Fund: Liquid savings for unexpected expenses

Monthly Expenses: Recurring costs for living

Financial Security: Protection against emergencies

• Aim for 3-6 months of expenses

• Build gradually if needed

• Start with smaller goal (e.g., $1,000)

• Automate monthly contributions

• Use high-yield savings account

• Not having an emergency fund

• Investing emergency funds in risky assets

• Using emergency funds for non-emergencies

Sarah is 30 years old and wants to retire at 65. She estimates needing $1.2 million at retirement. If she can earn 7% annually, how much should she save monthly to reach her goal?

Step 1: Calculate time period

Years until retirement: 65 - 30 = 35 years

Months until retirement: 35 × 12 = 420 months

Step 2: Calculate monthly rate

Monthly rate: 7% ÷ 12 = 0.5833% = 0.005833

Step 3: Use future value of annuity formula

For future value with no initial deposit: \( PMT = \frac{FV \times r}{(1 + r)^n - 1} \)

Step 4: Calculate required monthly payment

\( PMT = \frac{1,200,000 \times 0.005833}{(1.005833)^{420} - 1} \)

\( PMT = \frac{7,000}{10.67 - 1} = \frac{7,000}{9.67} = \$724 \)

Therefore, Sarah needs to save approximately $724 per month.

This problem shows how compound interest works over long periods. Starting early significantly reduces the monthly savings needed. The calculation demonstrates that even modest monthly contributions can grow to substantial amounts over 35 years due to compound interest. This highlights the importance of starting retirement savings early.

Retirement Planning: Preparing financially for post-work life

Time Horizon: Years until retirement

Future Value: Required amount at retirement

• Start saving early for compound growth

• Use tax-advantaged accounts

• Adjust contributions annually

• Maximize employer 401(k) match

• Consider catch-up contributions after age 50

• Review and adjust plan annually

• Starting retirement savings too late

• Not accounting for inflation

• Underestimating retirement duration

Which savings account type typically offers the highest interest rate?

The answer is B) High-Yield Savings Account. High-yield savings accounts typically offer the highest interest rates among liquid savings options, often 10-20 times higher than traditional savings accounts. CDs may offer competitive rates but require locking up funds for a specific term.

Savings account rates vary significantly based on type and institution. High-yield savings accounts are designed to compete with other investment options while maintaining liquidity. They typically offer higher rates than traditional savings accounts but lower than long-term investments. The trade-off is between accessibility and returns.

High-Yield Savings: Savings account with higher interest rate

Liquidity: Ease of accessing funds

Interest Rate: Percentage earned on deposits

• Compare rates across institutions

• Consider minimum balance requirements

• Check for fees

• Shop around for best rates

• Consider online banks for higher rates

• Look for promotional rates

• Keeping money in low-rate accounts

• Not researching alternatives

• Ignoring fees that reduce returns

FAQ

Q: How much should I save each month?

A: Financial experts recommend saving 10-20% of your gross income for long-term financial health. For beginners, start with 10% and gradually increase to 15-20% over time.

- Emergency Fund: 3-6 months of expenses

- Retirement: 10-15% of income

- Other Goals: Variable based on objectives

For example, if you earn $5,000 per month, aim to save $500-$1,000 monthly. Start with what you can manage and increase gradually. The key is consistency rather than perfection.

Q: What's the difference between a savings account and a money market account?

A: Both accounts earn interest, but they differ in several ways:

- Savings Account: Higher liquidity, lower rates, no minimums

- Money Market: Higher rates, higher minimums, limited transactions

Money market accounts typically offer higher interest rates than savings accounts but require higher minimum balances (often $1,000-$25,000). They may also limit the number of transactions per month. Savings accounts offer more flexibility but lower returns.