Take-Home Paycheck Calculator

Net pay • Paystub analysis

Take-Home Pay Formula:

Show the calculatorGross Pay = Hourly Rate × Hours Worked

Net Pay = Gross Pay - (Federal Tax + State Tax + Social Security + Medicare + Other Deductions)

Take-Home Percentage = (Net Pay ÷ Gross Pay) × 100

Where:

- Federal Tax: Progressive tax based on income and filing status

- State Tax: Varies by state (some states have no income tax)

- Social Security: 6.2% of wages up to $168,600 (2026)

- Medicare: 1.45% of all wages (plus 0.9% on high earners)

- Other Deductions: Health insurance, retirement contributions, etc.

This calculation determines your actual take-home pay after all mandatory and voluntary deductions. The net pay represents the amount you actually receive in your paycheck. Understanding this breakdown helps with budgeting and financial planning.

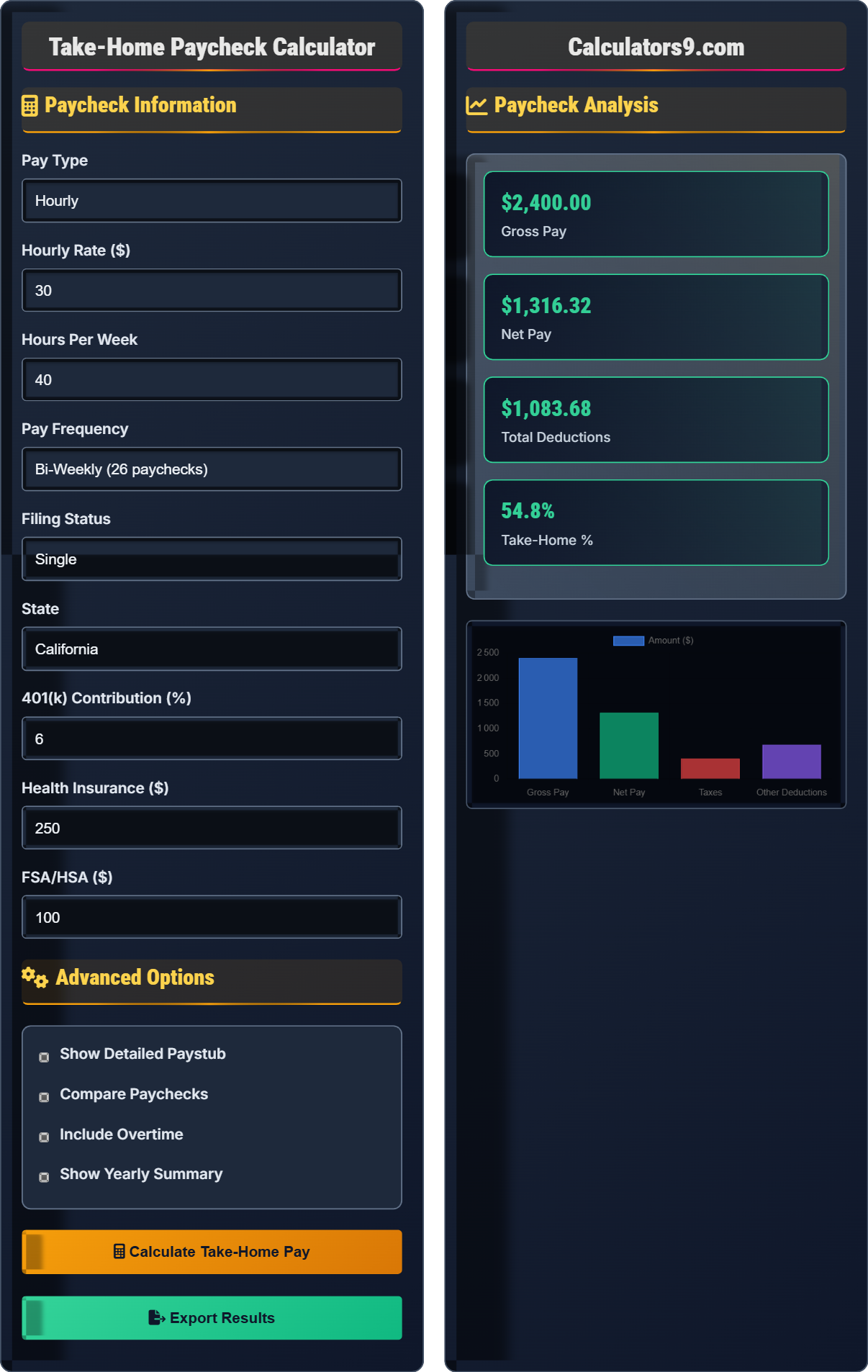

Example: For an hourly wage of $30 with 40 hours per week:

Gross Pay per Paycheck = $30 × 40 × 2 (bi-weekly) = $2,400

After federal tax (12%), state tax (5%), SS (6.2%), Medicare (1.45%), and $250 other deductions:

Net Pay = $2,400 - ($288 + $120 + $148.80 + $34.80 + $250) = $1,558.40

Take-Home Percentage = ($1,558.40 ÷ $2,400) × 100 = 64.9%

Paycheck Information

Advanced Options

Paycheck Analysis

| Item | Earnings | Deductions | YTD |

|---|

| Category | Amount | Percentage |

|---|

Comprehensive Paycheck Guide

Your paycheck shows the difference between your gross pay (total earnings) and net pay (take-home amount). Understanding each deduction helps you manage your finances and optimize your compensation. The paystub provides a detailed breakdown of all earnings and deductions.

The standard paycheck calculation uses this formula:

Where:

- Federal Tax: Progressive tax based on income and filing status

- State Tax: Varies by state (some have no income tax)

- Social Security: 6.2% of wages up to annual limit

- Medicare: 1.45% of all wages (0.9% additional for high earners)

- Other Deductions: Health insurance, retirement, etc.

Key advantages of understanding your paycheck include:

- Better Budgeting: Plan around actual take-home pay

- Tax Optimization: Maximize pre-tax deductions

- Financial Planning: Make informed career decisions

- Payroll Accuracy: Verify correct calculations

- Retirement Preparation: Plan for future income needs

- Understand Your Deductions: Know what's coming out of your paycheck

- Maximize 401(k): Get full employer match and tax benefits

- Use FSA/HSA: Pre-tax savings for medical expenses

- Review Your W-4: Optimize tax withholding

- Track YTD Totals: Monitor annual compensation

Paycheck Fundamentals

Understanding the components of your paycheck.

Net Pay = Gross Pay - (Tax + Deductions)

Take-Home % = (Net Pay ÷ Gross Pay) × 100

- Gross pay is higher than net pay due to deductions

- Payroll taxes are mandatory

- Pre-tax deductions reduce taxable income

Strategies

Maximizing your take-home pay through strategic planning.

- Calculate your actual take-home pay

- Maximize pre-tax deductions

- Review your paystub regularly

- Adjust tax withholding as needed

- State tax rates vary significantly

- Some states have no income tax

- Payroll taxes are flat rates

- Pre-tax deductions lower taxable income

Paycheck Planning Learning Quiz

Which of the following is NOT typically found on a paystub?

The answer is C) Credit score. A paystub shows earnings, deductions, and taxes, but does not include credit scores. Paystubs typically include gross pay, net pay, federal and state tax withholdings, Social Security and Medicare deductions, health insurance premiums, retirement contributions, and other voluntary deductions.

This question tests basic knowledge of paystub components. A paystub is a record of your employment compensation and deductions for a specific pay period. It's important to understand what information is typically included on paystubs to properly verify your compensation and deductions.

Paystub: Document showing earnings and deductions for a pay period

Gross Pay: Total earnings before deductions

Net Pay: Amount received after all deductions

• Paystubs show earnings and deductions

• Credit scores are not payroll information

• Verify all amounts on your paystub

• Review your paystub for accuracy

• Understand all deductions listed

• Keep records for tax purposes

• Not reviewing paystub for accuracy

• Not understanding all listed deductions

• Confusing paystub information with credit reports

Calculate the biweekly net pay for an employee earning $25/hour, working 40 hours per week, with 6% 401(k) contribution, $200 health insurance, and estimated federal tax of 12% and state tax of 5% on gross pay. Show your work.

Biweekly gross pay: $25 × 40 × 2 = $2,000

401(k) contribution: $2,000 × 6% = $120

Adjusted gross for taxes: $2,000 - $120 = $1,880

Federal tax: $1,880 × 12% = $225.60

State tax: $1,880 × 5% = $94.00

Social Security: $2,000 × 6.2% = $124.00

Medicare: $2,000 × 1.45% = $29.00

Total deductions: $120 + $225.60 + $94.00 + $124.00 + $29.00 + $200 = $792.60

Net pay: $2,000 - $792.60 = $1,207.40

Therefore, the biweekly net pay is $1,207.40.

This calculation demonstrates the multi-step process of determining take-home pay from hourly wages. First, calculate gross pay per period based on hours worked. Then, determine pre-tax deductions that reduce taxable income. Calculate taxes on the adjusted amount. Finally, subtract all deductions to arrive at net pay. Note that some deductions (like Social Security/Medicare) are calculated on gross pay, not adjusted pay.

Hourly Wage: Amount paid per hour of work

Pay Period: Time interval for which pay is calculated

Pre-Tax Deduction: Reduces taxable income

• Calculate gross pay first

• Apply pre-tax deductions before taxes

• Calculate taxes on adjusted gross pay

• Pre-tax deductions reduce your tax burden

• Calculate each deduction separately

• Double-check your math for accuracy

• Forgetting to apply pre-tax deductions before taxes

• Calculating taxes on gross instead of adjusted pay

• Missing deductions in the calculation

An employee earns $30/hour with 40 hours per week at regular pay and overtime at 1.5 times the regular rate for hours worked over 40. If they work 45 hours in a week, what is their gross pay for that week? How does this affect their take-home pay compared to a regular 40-hour week? (Hint: Calculate regular pay + overtime pay)

Regular pay: $30 × 40 = $1,200

Overtime hours: 45 - 40 = 5 hours

Overtime pay: $30 × 1.5 × 5 = $225

Total gross pay: $1,200 + $225 = $1,425

Compared to a 40-hour week ($1,200), the overtime week provides $225 more in gross pay.

However, the higher income may push the employee into a higher tax bracket for that pay period, potentially increasing the effective tax rate on the additional income.

Therefore, the gross pay is $1,425 with increased tax implications.

This example shows how overtime pay affects both gross and net pay. While overtime provides additional income, it can also increase the tax burden. The additional income is subject to the same tax rates as regular income, but may push the total pay period income into a higher marginal tax bracket, affecting the effective tax rate on the additional earnings.

Overtime: Hours worked beyond standard work week

Time and a Half: 1.5 times regular hourly rate

Marginal Tax Rate: Rate applied to highest income bracket

• Overtime is typically paid at 1.5x regular rate

• Additional income may increase tax burden

• Higher pay periods may affect tax withholding

• Overtime can significantly boost take-home pay

• Consider tax implications of extra income

• Higher pay periods may require W-4 adjustments

• Not accounting for tax implications of overtime

• Calculating overtime at regular rate instead of 1.5x

• Forgetting to consider marginal tax brackets

An employee earning $2,500 biweekly contributes 8% to their 401(k). If they're in the 12% federal tax bracket and 5% state tax bracket, how much in taxes do they save per paycheck due to the 401(k) contribution? What is the total tax savings annually? (Hint: Calculate tax savings from pre-tax contribution)

401(k) contribution per paycheck: $2,500 × 8% = $200

Federal tax savings per paycheck: $200 × 12% = $24

State tax savings per paycheck: $200 × 5% = $10

Total tax savings per paycheck: $24 + $10 = $34

Annual tax savings: $34 × 26 paychecks = $884

Therefore, the employee saves $34 per paycheck and $884 annually in taxes.

This demonstrates the immediate tax benefit of pre-tax retirement contributions. The 401(k) contribution reduces taxable income for the current year, lowering the tax bill. This is in addition to the long-term benefits of tax-deferred growth. The higher your tax bracket, the greater the immediate tax savings from pre-tax contributions.

Pre-Tax Contribution: Reduces current taxable income

Tax Savings: Reduction in tax liability

Traditional 401(k): Pre-tax contribution retirement account

• Pre-tax contributions reduce current tax liability

• Higher tax brackets mean greater savings

• Annual contribution limits apply

• Maximize contributions in higher tax brackets

• Get full employer match first

• Consider tax implications at retirement

• Not maximizing employer matching

• Forgetting tax benefits of pre-tax contributions

• Not considering retirement tax rates

Which statement about state income taxes is TRUE?

The answer is B) Some states have no income tax. States like Texas, Florida, Washington, Nevada, Tennessee, and New Hampshire do not have state income taxes. This means residents of these states don't have state income tax deducted from their paychecks, resulting in higher take-home pay compared to similar earners in states with income taxes.

This question addresses the variation in state tax laws across the United States. Understanding whether your state has an income tax is crucial for accurate take-home pay calculations. The absence of state income tax can significantly impact your net pay compared to states with high income tax rates.

State Income Tax: Tax collected by state governments

No-Income-Tax States: States that don't tax income

Take-Home Pay: Amount received after all deductions

• State tax rates vary significantly

• Some states have no income tax

• State taxes reduce take-home pay

• Check your state's tax rate

• Consider state taxes when relocating

• Factor state taxes into salary negotiations

• Assuming all states have income taxes

• Not considering state tax differences

• Ignoring state tax impact on take-home pay

FAQ

Q: Why is my take-home pay less than my gross pay?

A: Your take-home pay is reduced by mandatory and voluntary deductions. Using the formula: Net Pay = Gross Pay - (Federal Tax + State Tax + SS + Medicare + Other Deductions).

For example, with $2,400 gross pay ($30/hr × 40hrs × 2 weeks), common deductions include: - Federal tax (~12%): $288 - State tax (~5%): $120 - Social Security (6.2%): $148.80 - Medicare (1.45%): $34.80 - Other deductions: $250.00 Total deductions: $841.60, leaving $1,558.40 net pay.

Q: How do pre-tax deductions affect my take-home pay?

A: Pre-tax deductions like 401(k) contributions reduce both your taxable income AND your tax liability. For example, if you earn $2,400 and contribute $144 (6%) to 401(k):

Adjusted gross for taxes: $2,400 - $144 = $2,256

Federal tax at 12%: $2,256 × 0.12 = $270.72

Without 401(k), federal tax would be: $2,400 × 0.12 = $288

You save $17.28 in federal tax plus state tax savings, while only reducing take-home by $144.