VAT Calculator

Multi-country VAT calculator • 2026 rates

VAT Formula:

Show the calculator\( \text{VAT Amount} = \frac{\text{Price} \times \text{VAT Rate}}{100 + \text{VAT Rate}} \)

\( \text{Price Including VAT} = \text{Price} + \text{VAT Amount} \)

Where:

- Price = Price excluding VAT

- VAT Rate = Value Added Tax rate as percentage

- VAT Amount = Tax amount to be added

- Price Including VAT = Final price with tax

This formula calculates VAT based on the standard method used in most countries. VAT is a consumption tax levied on the value added at each stage of production and distribution. Unlike sales tax, VAT is collected incrementally throughout the supply chain.

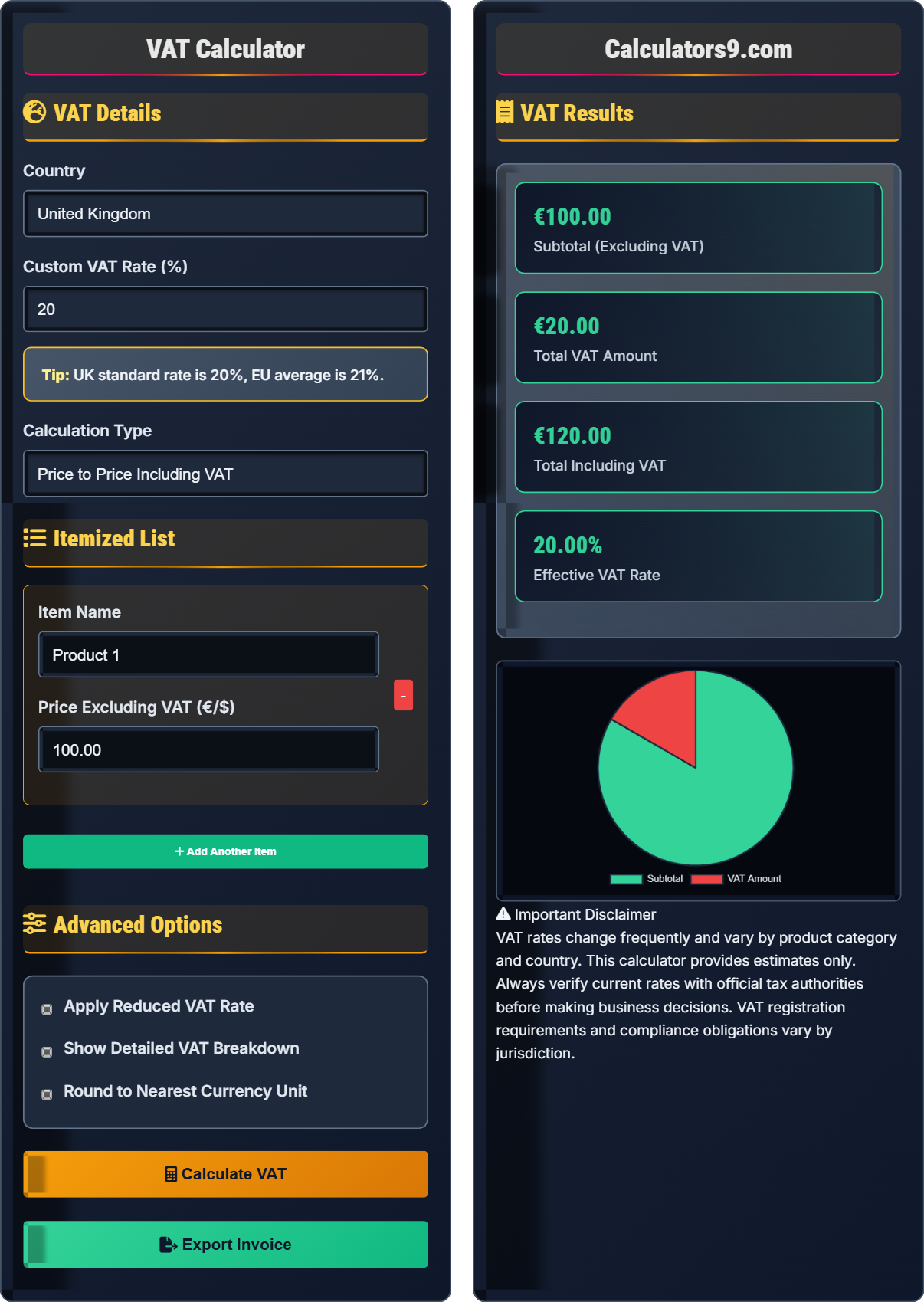

Example: For a product priced at €100 in a country with 20% VAT:

VAT Amount = (€100 × 20) / (100 + 20) = €20

Price Including VAT = €100 + €20 = €120

Alternatively: Price Including VAT = €100 × 1.20 = €120

Thus, the customer pays €120 total for the €100 product.

VAT Details

Itemized List

Advanced Options

VAT Results

VAT rates change frequently and vary by product category and country. This calculator provides estimates only. Always verify current rates with official tax authorities before making business decisions. VAT registration requirements and compliance obligations vary by jurisdiction.

VAT Basics

Value Added Tax (VAT) is a consumption tax placed on a product whenever value is added at each stage of the supply chain, from production to the point of sale. The amount of VAT that the consumer pays is the cost of the product, minus any of the costs of materials used in the product that have already been subject to VAT.

Alternatively: Price Including VAT = Price × (1 + VAT Rate/100)

- VAT is charged on most goods and services sold for domestic consumption

- Businesses must register for VAT if their turnover exceeds certain thresholds

- VAT is charged at different rates depending on the product/service

- Businesses can reclaim VAT paid on business expenses

- VAT is ultimately borne by the final consumer

Country VAT Rates

Standard VAT rates vary significantly across countries. The EU has minimum standards but allows member states flexibility within ranges. Some countries have higher rates to fund public services.

| Country | Standard Rate | Reduced Rate | Special Rates |

|---|---|---|---|

| United Kingdom | 20% | 5% | 0% (books, children's clothes) |

| Germany | 19% | 7% | Food, hotels, books |

| France | 20% | 5.5%, 10% | Multiple reduced rates |

| Italy | 22% | 4%, 5%, 10% | Complex tiered system |

| Spain | 21% | 10%, 4% | Super-reduced rate |

| Netherlands | 21% | 9% | Food, books, restaurants |

| Australia | 10% | - | GST system |

| Canada | 5% | - | Plus provincial sales tax |

- UK: £85,000 annual taxable turnover

- Germany: €22,000 in first year, €50,000 ongoing

- France: €85,800 for goods, €34,400 for services

- Italy: €77,000 for services, €400,000 for goods

VAT Compliance

Many countries apply reduced VAT rates to essential goods and services to reduce the tax burden on consumers. These rates vary significantly by country and product category.

Essential Goods

Food, water, medicines, and basic necessities often qualify for reduced rates.

Cultural Services

Books, newspapers, museums, and cultural events may have reduced rates.

Transportation

Public transport and train tickets often qualify for reduced rates.

Energy

Heating and electricity may have reduced rates in some countries.

- Keep detailed records of all VAT transactions

- Submit VAT returns regularly (monthly/quarterly/annually)

- Charge correct VAT rate for each product/service

- Reclaim VAT on eligible business expenses

- Issue valid VAT invoices for all taxable supplies

VAT Learning Quiz

Which of the following best describes how VAT differs from sales tax?

The answer is B) VAT is collected at each stage of production/distribution. Unlike sales tax which is only charged at the final point of sale, VAT is levied at each stage where value is added to the product. However, businesses can reclaim VAT they pay on business inputs, so the ultimate burden falls on the final consumer.

VAT operates differently from traditional sales tax. As a product moves through the supply chain, each business adds value and charges VAT on that value. But they can also reclaim VAT they've paid on inputs. This means the VAT system captures tax at each stage, but the total burden is equivalent to taxing the final consumer. This prevents tax evasion that can occur with traditional sales tax systems.

VAT (Value Added Tax): Tax on the value added at each stage of production

Supply Chain: Series of stages from production to final sale

VAT Reclamation: Process of getting back VAT paid on business expenses

• VAT is charged at each value-adding stage

• Businesses can reclaim VAT on inputs

• Final consumer bears the total tax burden

• Think of VAT as a tax on value creation

• Businesses act as tax collectors for government

• VAT ensures tax collection at multiple points

• Confusing VAT with simple sales tax

• Not understanding the reclamation mechanism

• Assuming businesses pay the final tax

Calculate the VAT amount and final price for a product priced at €150 with a 20% VAT rate. Show your work.

Method 1: Direct calculation

VAT Amount = Price × VAT Rate

VAT Amount = €150 × 0.20 = €30

Final Price = €150 + €30 = €180

Method 2: Using the standard formula

VAT Amount = (Price × VAT Rate) / (100 + VAT Rate)

VAT Amount = (€150 × 20) / (100 + 20) = €3000 / 120 = €25

Wait, that's not right. Let me recalculate:

If the price €150 is EXCLUDING VAT:

VAT Amount = €150 × 0.20 = €30

Final Price = €150 + €30 = €180

When the base price excludes VAT, we simply multiply by the VAT rate to find the tax amount. The confusion often arises when the given price already includes VAT. In that case, we need to work backwards using the formula: VAT Amount = (Price Including VAT × VAT Rate) / (100 + VAT Rate).

Price Excluding VAT: Base price before tax addition

Price Including VAT: Final price with tax includedVAT Rate: Percentage of tax to be applied

• Clarify whether price includes or excludes VAT

• Use different formulas based on given information

• VAT rates must be in decimal form for calculations

• Always clarify the base amount before calculating

• Use Price × (1 + VAT rate) for quick inclusion

• Double-check which amount is given

• Confusing price including/excluding VAT

• Using wrong formula for the given information

• Forgetting to convert percentage to decimal

You see a product priced at €120 including 20% VAT. What is the price excluding VAT and how much VAT was charged?

Step 1: Set up the equation

If final price = original price × (1 + VAT rate)

Then original price = final price ÷ (1 + VAT rate)

Step 2: Convert VAT rate to decimal

20% = 0.20

Step 3: Calculate original price

Original price = €120 ÷ (1 + 0.20) = €120 ÷ 1.20 = €100

Step 4: Calculate VAT amount

VAT amount = €120 - €100 = €20

Alternatively: VAT amount = (€120 × 20) / (100 + 20) = €20

Therefore, the price excluding VAT is €100 and VAT charged is €20.

Reverse VAT calculation is essential when you only know the final price including tax. This is common in expense reporting, budgeting, and comparing prices across regions with different tax rates. The formula divides the total price by (1 + VAT rate) to find the original amount before tax.

Reverse Calculation: Finding original amount from final amount

Price Excluding VAT: Original price before tax

Price Including VAT: Final price after tax addition

• Divide by (1 + VAT rate) for reverse calculation

• VAT rate must be in decimal form

• Always verify with forward calculation

• Remember: Final = Original × (1 + rate)

• So: Original = Final ÷ (1 + rate)

• Use calculator for precise division

• Subtracting VAT percentage from final amount

• Forgetting to convert percentage to decimal

• Using wrong formula for reverse calculation

A restaurant bill includes: €50 for food (subject to 5% reduced VAT), €30 for drinks (subject to 20% standard VAT), and €20 for services (subject to 20% standard VAT). Calculate the total VAT and final bill amount.

Step 1: Calculate VAT for each category

Food VAT: €50 × 0.05 = €2.50

Drinks VAT: €30 × 0.20 = €6.00

Services VAT: €20 × 0.20 = €4.00

Step 2: Calculate subtotal (excluding VAT)

Subtotal = €50 + €30 + €20 = €100

Step 3: Calculate total VAT

Total VAT = €2.50 + €6.00 + €4.00 = €12.50

Step 4: Calculate final bill

Final Bill = €100 + €12.50 = €112.50

Therefore, the total VAT is €12.50 and the final bill is €112.50.

This problem demonstrates how different products/services may be subject to different VAT rates within the same transaction. Many countries have multiple VAT rates for different categories of goods and services. This complexity requires careful tracking and calculation for businesses and accurate reporting for tax compliance.

Multiple VAT Rates: Different tax rates for different product categories

Rate Classification: Assigning correct VAT rate to each item

Composite Calculation: Summing taxes across different rates

• Apply correct VAT rate to each product category

• Calculate VAT separately for each rate

• Sum individual VAT amounts for total

• Maintain separate totals for each VAT rate

• Keep detailed records by rate category

• Use POS systems to automate rate assignment

• Applying standard rate to all items

• Not knowing correct rate for specific items

• Misclassifying products/services for tax purposes

Which statement about VAT registration is TRUE?

The answer is B) VAT registration is mandatory when turnover exceeds thresholds. Most countries have VAT registration thresholds (e.g., £85,000 in the UK). Once a business's taxable turnover exceeds this threshold, registration becomes mandatory. Below the threshold, registration may be voluntary.

VAT registration thresholds protect small businesses from administrative burdens while ensuring adequate tax collection. The threshold concept recognizes that smaller businesses may not have the resources to manage VAT compliance. However, once a business grows beyond the threshold, it must register to prevent tax avoidance and ensure fair competition with registered competitors.

VAT Registration: Official enrollment to collect and remit VAT

Threshold: Turnover limit triggering registration requirement

Turnover: Total business revenue in a period

• Registration required when turnover exceeds threshold

• Thresholds vary by country

• Voluntary registration may be available below threshold

• Monitor turnover regularly to avoid late registration

• Check your country's specific threshold

• Consider voluntary registration for business benefits

• Not tracking turnover toward threshold

• Assuming registration is always optional

• Missing registration deadlines

FAQ

Q: When do I need to register for VAT?

A: VAT registration requirements vary by country, but generally you must register when your taxable turnover exceeds the threshold. For example:

- UK: £85,000 annual taxable turnover

- Germany: €22,000 in first year, €50,000 ongoing

- France: €85,800 for goods, €34,400 for services

You must register within a specific timeframe (usually 30 days) after exceeding the threshold. However, you can register voluntarily before reaching the threshold. Once registered, you must charge VAT on all taxable supplies and submit regular VAT returns. The registration process includes obtaining a VAT identification number and setting up record-keeping systems.

Q: How does VAT work for imports and exports?

A: VAT treatment for international trade follows specific rules:

- Imports: VAT is typically due at customs clearance based on the value of goods plus duties

- Exports: Generally zero-rated (0% VAT) if goods leave the country within specified time

- B2B Supplies: Within EU, reverse charge mechanism may apply

- B2C Supplies: VAT charged at destination country rate

For example, if a German company sells goods to a French consumer, French VAT (20%) would apply. For B2B transactions, the customer may be responsible for VAT under the reverse charge mechanism. Import VAT can usually be reclaimed if you're VAT-registered. Proper documentation is essential for all international transactions.