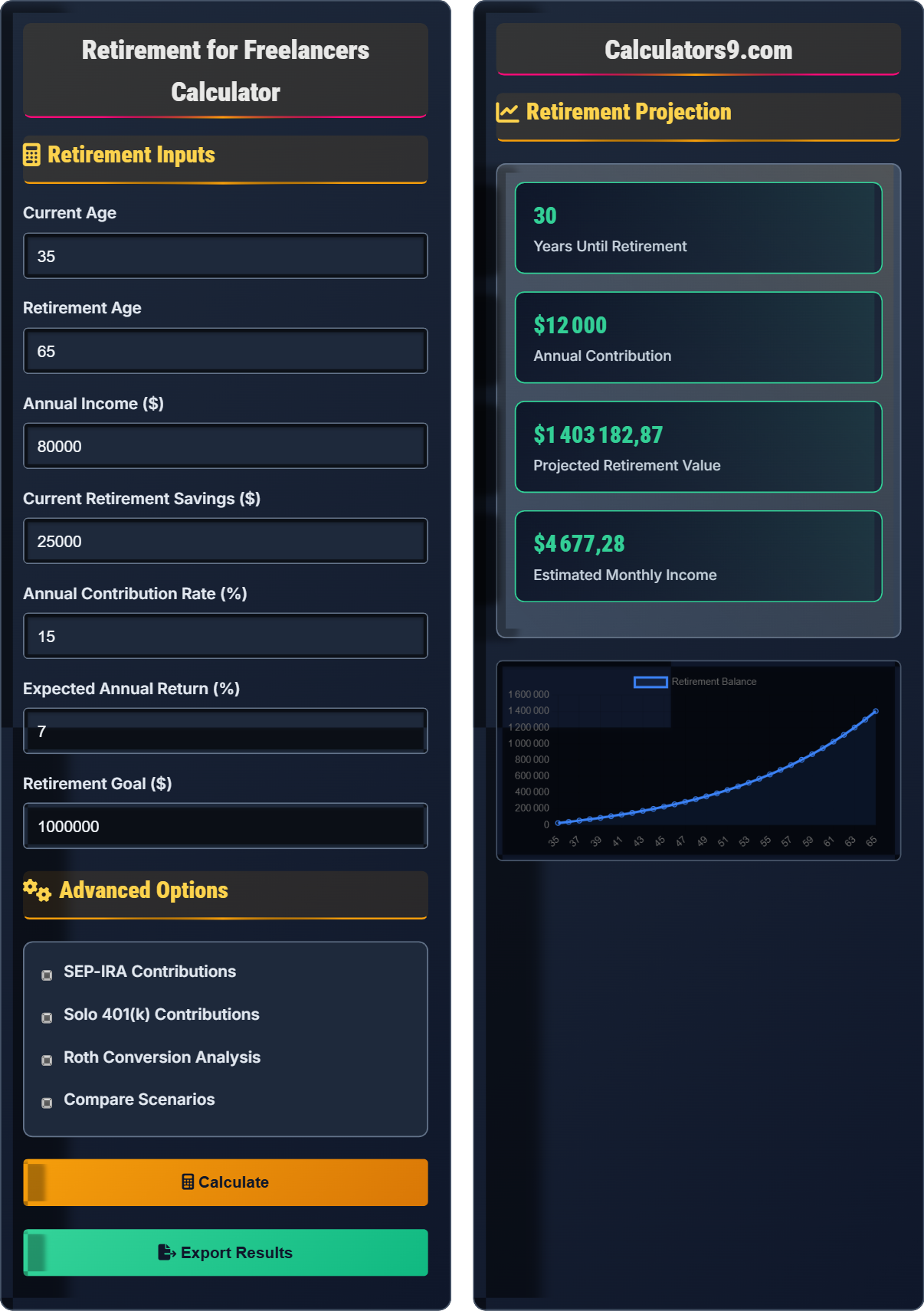

Retirement for Freelancers Calculator

Independent contractor retirement planner • 2026 edition

Retirement Planning Formulas for Freelancers:

- SEP-IRA Contribution: Up to 25% of net self-employment income OR $66,000 (2023 limit)

- Solo 401(k) Contribution: Employee ($23,000) + Employer (25% of net income)

- Estimated Growth: Future Value = Present Value × (1 + r)^n

- Required Savings Rate: Target ÷ (Years until retirement × Income)

For example: With $80,000 annual income, a freelancer can contribute up to $20,000 to a SEP-IRA. At 7% annual growth for 25 years, this would grow to approximately $126,000.

Retirement Inputs

Advanced Options

Retirement Projection

| Year | Age | Contribution | Balance | Growth |

|---|

| Strategy | Limit | Eligibility | Benefits |

|---|

Retirement Planning for Freelancers

Freelancers face distinct retirement planning challenges: irregular income, lack of employer-sponsored benefits, and complex tax situations. However, they also have unique advantages like higher contribution limits to retirement accounts and greater flexibility in investment choices.

Key retirement account options for freelancers include:

SEP-IRA: Up to 25% of net self-employment income

Solo 401(k): Employee + Employer contributions

Traditional IRA: Standard individual account

Roth IRA: Tax-free growth in retirement

As of 2023, retirement contribution limits for freelancers:

- SEP-IRA: Up to 25% of net self-employment income OR $66,000

- Solo 401(k): Employee ($23,000) + Employer (up to 25% of net income)

- Traditional IRA: $6,500 ($7,500 if 50+)

- Roth IRA: $6,500 ($7,500 if 50+) - income limits apply

- Immediate Deduction: SEP-IRA contributions reduce current taxable income

- Flexibility: Adjust contribution amount annually based on income

- Roth Conversions: Convert traditional to Roth for tax-free growth

- Self-Employment Tax: Retirement contributions reduce self-employment tax

- Spousal Benefits: Spouse can contribute to SEP-IRA if they have earned income

Retirement Planning Learning Quiz

For a freelancer earning $100,000 in net self-employment income in 2023, what is the maximum contribution to a SEP-IRA?

The answer is A) $25,000. For a SEP-IRA, the contribution limit is the lesser of 25% of net self-employment income or $66,000. In this case, 25% of $100,000 = $25,000, which is less than the $66,000 cap. So the maximum contribution is $25,000.

This question tests understanding of the dual limits for SEP-IRA contributions. The calculation involves taking the lesser of two values: 25% of net income OR the dollar limit ($66,000 for 2023). For freelancers with lower incomes, the percentage limit typically applies. For those with higher incomes, the dollar limit caps the contribution.

Net Self-Employment Income: Business income minus business expenses

Contribution Limit: Maximum amount that can be contributed annually

SEP-IRA: Simplified Employee Pension Individual Retirement Account

• SEP-IRA contribution = MIN(25% of net income, $66,000)

• Contribution is tax-deductible

• No catch-up contributions allowed

• Calculate net income after business expenses

• Remember to account for self-employment tax

• Consider SEP-IRA for simplicity and high limits

• Using gross income instead of net income

• Forgetting that only 92.35% of net income counts for SE tax

• Not understanding the dual limit structure

If a freelancer earns $120,000 annually and contributes the maximum employee amount to a Solo 401(k), how much can they contribute as the employer, and what is the total annual contribution?

Step 1: Calculate employee contribution = $23,000 (2023 limit)

Step 2: Calculate employer contribution = 25% of net self-employment income

Employer contribution = $120,000 × 0.25 = $30,000

Step 3: Calculate total contribution = Employee + Employer

Total contribution = $23,000 + $30,000 = $53,000

Therefore: Employer can contribute $30,000 and total annual contribution is $53,000.

This problem demonstrates the dual nature of Solo 401(k) contributions. As both employee and employer, freelancers can contribute from both perspectives. The employee contribution has a fixed limit, while the employer contribution is based on a percentage of income. This allows for significantly higher total contributions compared to traditional IRAs.

Solo 401(k): 401(k) plan for self-employed individuals

Employee Contribution: Contribution made by the individualEmployer Contribution: Contribution made by the business

• Employee contribution: $23,000 (2023) or $30,500 if 50+

• Employer contribution: Up to 25% of net self-employment income

• Total cannot exceed $66,000 (2023) or $73,500 with catch-up

• Solo 401(k) offers highest contribution limits for freelancers

• Can make both employee and employer contributions

• Allows for loan provisions (if plan permits)

• Not accounting for the dual contribution structure

• Forgetting the total contribution limit

• Confusing Solo 401(k) with traditional 401(k)

Sarah is 30 years old and wants to retire at 65. She currently has $30,000 in retirement savings and earns $90,000 annually as a freelancer. If she wants to have $1.5 million at retirement and expects a 7% annual return, what percentage of her income should she contribute annually?

Step 1: Calculate years until retirement = 65 - 30 = 35 years

Step 2: Calculate future value needed = $1,500,000

Step 3: Calculate future value of current savings = $30,000 × (1.07)^35

Future value of current = $30,000 × 10.68 = $320,400

Step 4: Calculate amount needed from contributions = $1,500,000 - $320,400 = $1,179,600

Step 5: Calculate required annual contribution using future value of annuity formula

Using FV = PMT × [((1+r)^n - 1) / r]

$1,179,600 = PMT × [((1.07)^35 - 1) / 0.07]

$1,179,600 = PMT × [10.68 / 0.07] = PMT × 152.57

PMT = $1,179,600 / 152.57 = $7,730

Step 6: Calculate percentage of income = ($7,730 / $90,000) × 100 = 8.6%

Therefore: Sarah should contribute approximately 8.6% of her income annually.

This problem demonstrates reverse retirement planning: starting with a goal and calculating the required contributions. The solution separates the growth of current savings from the contributions needed, then uses the future value of an annuity formula to find the required annual contribution. This approach helps freelancers set realistic savings targets.

Future Value of Annuity: Value of a series of equal payments at a future date

Time Value of Money: Concept that money today is worth more than money tomorrow

Compound Growth: Growth that includes returns on previous returns

• FV of annuity = PMT × [((1+r)^n - 1) / r]

• Current savings grow separately from contributions

• Earlier contributions have more time to compound

• Start saving early to maximize compounding

• Use retirement calculators for complex scenarios

• Increase contributions as income grows

• Not accounting for current savings in calculations

• Using simple interest instead of compound interest

• Forgetting to factor in inflation

Mike is a freelancer in the 24% federal tax bracket who contributes $20,000 to a SEP-IRA. His state tax rate is 5%. How much will he save in federal and state taxes this year, and how does this affect his effective contribution cost? Additionally, if his self-employment tax rate is 15.3%, how much does he save on self-employment tax?

Step 1: Calculate federal tax savings = Contribution × Federal tax rate

Federal tax savings = $20,000 × 0.24 = $4,800

Step 2: Calculate state tax savings = Contribution × State tax rate

State tax savings = $20,000 × 0.05 = $1,000

Step 3: Calculate total tax savings = Federal + State

Total tax savings = $4,800 + $1,000 = $5,800

Step 4: Calculate effective contribution cost = Gross contribution - Tax savings

Effective cost = $20,000 - $5,800 = $14,200

Step 5: Calculate self-employment tax savings = Contribution × 0.9235 × SE tax rate

SE tax savings = $20,000 × 0.9235 × 0.153 = $2,830

Therefore: $5,800 in income tax savings, $2,830 in SE tax savings, $14,200 effective cost.

This problem demonstrates the multiple tax benefits of retirement contributions for freelancers. The calculation includes both income tax deductions and self-employment tax reductions. The self-employment tax calculation requires multiplying by 0.9235 because only 92.35% of net earnings are subject to SE tax. These multiple benefits make retirement contributions particularly valuable for freelancers.

Self-Employment Tax: Social Security and Medicare taxes for freelancers

Effective Contribution Cost: Actual cost after tax benefits

Income Tax Deduction: Reduction in taxable income

• SEP-IRA contributions reduce both income and SE taxes

• Only 92.35% of net income counts for SE tax

• Effective cost = Gross contribution - Total tax savings

• Consider both income and SE tax benefits

• Track effective contribution costs

• Maximize contributions when in high tax brackets

• Forgetting self-employment tax benefits

• Not accounting for 0.9235 factor in SE tax

• Confusing tax brackets with tax rates

Which combination of strategies would provide the GREATEST retirement benefit for a freelancer earning $150,000 annually?

The answer is B) Solo 401(k) with maximum employee + employer contributions. Let's calculate:

A) SEP-IRA: 25% of $150,000 = $37,500

B) Solo 401(k): $23,000 (employee) + $37,500 (employer) = $60,500

C) Traditional IRA: $6,500 (or $7,500 if 50+)

D) Roth conversion doesn't increase contribution limits

The Solo 401(k) allows for the highest total contribution of $60,500, combining both employee and employer contributions.

This question compares different retirement account options based on contribution limits. The Solo 401(k) is particularly advantageous for freelancers because it allows both employee and employer contributions, effectively doubling the contribution capacity. This makes it ideal for high earners who want to maximize their retirement savings.

Contribution Capacity: Total amount that can be contributed

Maximization Strategy: Choosing the option with highest limits

High Earner Advantage: Higher limits for those with more income

• Solo 401(k) offers highest limits for freelancers

• SEP-IRA limits are based on percentage of income

• Traditional/Roth IRA have fixed limits regardless of income

• High earners should prioritize Solo 401(k)

• Consider both contribution limits and tax treatment

• Evaluate multiple accounts for diversification

• Assuming all accounts have equal limits

• Not understanding the dual contribution feature of Solo 401(k)

• Overlooking self-employment tax benefits

Retirement Planning Basics

Contribution limits, account types, and tax benefits for freelancers.

SEP-IRA: MIN(25% of net income, $66,000)

Solo 401(k): Employee ($23,000) + Employer (25% of net income)

Future Value: PV × (1 + r)^n

- SEP-IRA: Simple but limited

- Solo 401(k): Highest limits

- Maximize early contributions

Planning Strategies

Choose the right account and contribution level for your situation.

- Assess your income stability

- Select appropriate account type

- Maximize tax benefits

- Review annually and adjust

- Income fluctuation affects contributions

- Tax planning is crucial

- Start early for compounding

- Consider professional advice

FAQ

Q: Should I choose a SEP-IRA or Solo 401(k) for my retirement savings?

A: The choice depends on your income level and needs:

Choose SEP-IRA if:

- You want simplicity and low administrative burden

- Your income is moderate (under $100K annually)

- You prefer straightforward contribution calculations

- You don't need loan provisions

Choose Solo 401(k) if:

- You have higher income ($100K+) and want maximum contributions

- You want to contribute both as employee and employer

- You might need loan provisions in the future

- You prefer Roth 401(k) options (if available)

Calculation Example: For $120,000 income:

- SEP-IRA: $120,000 × 0.25 = $30,000

- Solo 401(k): $23,000 + $30,000 = $53,000

Q: How do I handle retirement contributions when my income varies significantly from month to month?

A: Income volatility is common for freelancers. Here are strategies to manage retirement contributions:

1. Percentage-Based Approach: Set a percentage of monthly income to contribute automatically. For example, 15% of whatever you earn each month.

2. Target Annual Amount: Calculate your annual contribution goal and spread it across months when you have income. If you want to contribute $18,000 annually and work 10 months, contribute $1,800 each month you earn.

3. Lump-Sum Contributions: Make larger contributions during high-income months or at tax time when you have a clearer picture of annual earnings.

4. Flexible Account Choice: Solo 401(k) and SEP-IRA allow you to adjust contribution amounts annually based on actual income.

5. Emergency Buffer: Maintain a small emergency fund for months when you can't contribute to avoid breaking your savings habit.

Remember, consistency over perfection. Even contributing $200/month during low months is better than stopping entirely.