Insurance Reimbursement Calculator

Healthcare operations tool • 2026 edition

Reimbursement Formula:

Show the calculator\( IR = (BC \times PM) \times (1 - DR) \times (1 - CD) \times (1 + AD) \times (1 - PC) \)

Where:

- \( IR \) = Insurance Reimbursement ($)

- \( BC \) = Base Charge (CPT code value)

- \( PM \) = Payer Multiplier (insurance contract rate)

- \( DR \) = Denial Rate (claims rejected)

- \( CD \) = Contractual Discount (negotiated rates)

- \( AD \) = Additional Adjustments (coding/billing adjustments)

- \( PC \) = Prior Authorization Corrections (preapproval adjustments)

This formula calculates expected insurance reimbursement based on contracted rates, denial rates, and various adjustments. Healthcare facilities use this to project revenue, optimize billing processes, and negotiate payer contracts. Reimbursement varies significantly by payer type and procedure complexity.

Example: For a procedure with \( BC = \$1,000 \), \( PM = 0.8 \) (80% of base), \( DR = 0.05 \) (5% denials), \( CD = 0.15 \) (15% discount), \( AD = 0.02 \) (2% adjustments), and \( PC = 0.03 \) (3% prior auth corrections):

\( IR = (1000 \times 0.8) \times (1 - 0.05) \times (1 - 0.15) \times (1 + 0.02) \times (1 - 0.03) = 800 \times 0.95 \times 0.85 \times 1.02 \times 0.97 = \$637.47 \)

Thus, the expected reimbursement would be $637.47.

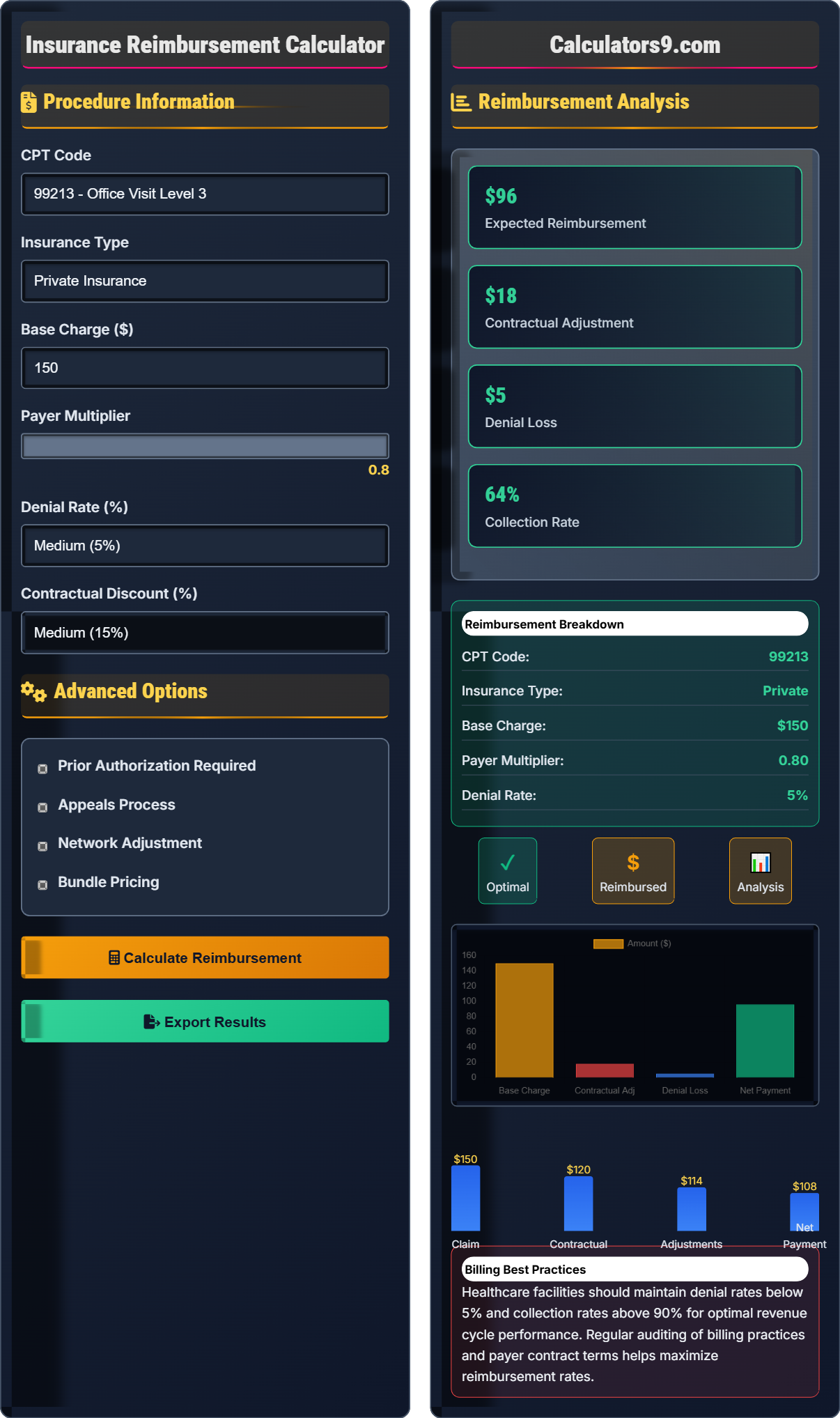

Procedure Information

Advanced Options

Reimbursement Analysis

Healthcare facilities should maintain denial rates below 5% and collection rates above 90% for optimal revenue cycle performance. Regular auditing of billing practices and payer contract terms helps maximize reimbursement rates.

Insurance Reimbursement Framework

Insurance reimbursement in healthcare involves complex calculations based on CPT codes, payer contracts, and regulatory requirements. Healthcare facilities must understand the various factors affecting reimbursement rates to maintain financial sustainability and optimize revenue cycle management.

The standard healthcare insurance reimbursement calculation uses the following formula:

Where:

- \(IR\) = Insurance Reimbursement

- \(BC\) = Base Charge

- \(PM\) = Payer Multiplier

- \(DR\) = Denial Rate

- \(CD\) = Contractual Discount

- \(AD\) = Additional Adjustments

- \(PC\) = Prior Authorization Corrections

Healthcare facilities experience varying reimbursement rates by payer type:

- Private Insurance: Typically 70-120% of Medicare rates

- Medicare: Standardized rates based on RBRVS system

- Medicaid: Usually 50-80% of Medicare rates

- Managed Care: Negotiated rates, typically 60-100% of charges

- Self-Pay: Full charge amount (if collected)

- Workers' Compensation: Often 100% of charges

- Pre-Service Verification: Confirm insurance eligibility and authorization

- Accurate Coding: Ensure proper CPT and ICD-10 coding

- Timely Submission: Submit claims within payer deadlines

- Denial Management: Systematic tracking and appeal process

- Contract Negotiation: Optimize payer contract terms

- Technology Integration: Automated billing and verification systems

Reimbursement Framework

CPT codes, payer contracts, and adjustments determine insurance reimbursement amounts.

\(IR = (BC \times PM) \times (1 - DR) \times (1 - CD) \times (1 + AD) \times (1 - PC)\)

Where IR=reimbursement, BC=base charge, PM=payer multiplier, DR=denial rate, CD=contractual discount, AD=adjustments, PC=prior auth corrections.

- Private insurance: 70-120% of Medicare

- Medicaid: 50-80% of Medicare

- Optimal denial rate: < 5%

Reimbursement Analysis

Insurance type, CPT codes, and contract terms influence reimbursement amounts.

- Identify base charge for CPT code

- Apply payer multiplier

- Subtract contractual adjustments

- Account for denials and adjustments

- Denial rates affect collection rates

- Contractual adjustments are permanent

- Appeals can recover denied amounts

Insurance Reimbursement Learning Quiz

Which of the following typically has the highest reimbursement rates for healthcare providers?

The answer is C) Private Insurance. Private insurance typically reimburses at rates of 70-120% of Medicare rates, while Medicaid reimburses at 50-80% of Medicare rates. Self-pay patients may pay full charges but are not guaranteed payment.

Healthcare reimbursement rates vary significantly by payer type. Private insurers typically reimburse at higher rates than government programs because they have more negotiating flexibility. Medicare serves as the baseline for many calculations, with other payers adjusting their rates relative to Medicare fee schedules.

Medicare Fee Schedule: Standardized rates for services

Contractual Adjustment: Reduction in billed amount

Reimbursement Rate: Percentage of charges paid

• Private insurance: 70-120% of Medicare

• Medicaid: 50-80% of Medicare

• Workers' Comp: Often 100% of charges

• Negotiate better rates with private insurers

• Monitor Medicaid rate changes

• Verify insurance before services

• Assuming all insurance pays equally

• Not tracking payer-specific rates

• Overlooking contractual adjustments

Calculate the expected reimbursement for a procedure with base charge of $500, payer multiplier of 0.75 (75% of base), denial rate of 8%, contractual discount of 12%, additional adjustments of 3%, and prior authorization corrections of 2%. Show your work.

Using the reimbursement formula: \(IR = (BC \times PM) \times (1 - DR) \times (1 - CD) \times (1 + AD) \times (1 - PC)\)

Given:

- BC = $500 (base charge)

- PM = 0.75 (payer multiplier)

- DR = 0.08 (denial rate)

- CD = 0.12 (contractual discount)

- AD = 0.03 (additional adjustments)

- PC = 0.02 (prior auth corrections)

Step 1: Calculate initial payment

Initial payment = BC × PM = $500 × 0.75 = $375

Step 2: Apply factors

IR = $375 × (1 - 0.08) × (1 - 0.12) × (1 + 0.03) × (1 - 0.02)

= $375 × 0.92 × 0.88 × 1.03 × 0.98

= $375 × 0.772 = $289.50

The expected reimbursement is $289.50.

This calculation demonstrates how multiple factors compound to affect reimbursement. The denial rate and contractual discount reduce payment, while additional adjustments slightly increase it. Prior authorization corrections also reduce the final amount. Understanding these factors helps facilities project revenue accurately.

Base Charge (BC): Standard rate for service

Payer Multiplier (PM): Contracted rate percentage

Contractual Discount (CD): Negotiated rate reduction

• Denial rate reduces final amount

• Contractual adjustments are permanent

• Additional adjustments can increase amount

• Calculate base amount first

• Apply factors sequentially

• Verify all adjustments are accounted for

• Forgetting to apply all factors

• Misapplying subtraction/addition for factors

• Not considering the compounding effect

A hospital performs 1,000 procedures per month with an average base charge of $1,200. Their private insurance contracts have a 75% multiplier with 15% contractual adjustments and 6% denial rate. Calculate the monthly revenue loss due to denials and contractual adjustments. If they could reduce denials by 2%, what would be the monthly savings?

Step 1: Calculate contracted amount per procedure

Contracted amount = $1,200 × 0.75 = $900

Step 2: Calculate monthly revenue without denials

Monthly revenue = 1,000 × $900 = $900,000

Step 3: Calculate revenue loss from contractual adjustments

Contractual loss = $900,000 × 0.15 = $135,000

Step 4: Calculate revenue loss from denials

Denial loss = $900,000 × 0.06 = $54,000

Step 5: Calculate total revenue loss

Total loss = $135,000 + $54,000 = $189,000

Step 6: Calculate savings from 2% reduction in denials

New denial loss = $900,000 × 0.04 = $36,000

Savings = $54,000 - $36,000 = $18,000

The hospital loses $189,000 monthly due to denials and adjustments. Reducing denials by 2% would save $18,000 monthly.

This example shows the significant impact of revenue cycle inefficiencies. Even modest reductions in denial rates can result in substantial savings. The calculation demonstrates how denials and contractual adjustments compound to reduce total revenue. Healthcare facilities should prioritize denial prevention and management as a revenue optimization strategy.

Revenue Cycle: Process from service delivery to payment

Denial Management: Process to address rejected claims

Contractual Adjustment: Permanent reduction in payment

• Denials reduce collectible revenue

• Contractual adjustments are permanent losses

• Small improvements can yield large savings

• Track denial reasons systematically

• Implement automated verification systems

• Negotiate favorable contract terms

• Not distinguishing between denials and adjustments

• Underestimating impact of small percentage changes

• Not tracking root causes of denials

A medical practice is negotiating a new contract with an insurance company. Their current contract has a 70% multiplier with 20% contractual adjustments. The new offer provides an 80% multiplier with 25% contractual adjustments. For a procedure with base charge of $1,000, which contract provides better reimbursement? Calculate the difference.

Step 1: Calculate current contract reimbursement

Contracted amount = $1,000 × 0.70 = $700

Net reimbursement = $700 × (1 - 0.20) = $700 × 0.80 = $560

Step 2: Calculate proposed contract reimbursement

Contracted amount = $1,000 × 0.80 = $800

Net reimbursement = $800 × (1 - 0.25) = $800 × 0.75 = $600

Step 3: Calculate difference

Difference = $600 - $560 = $40

The proposed contract provides $40 more reimbursement per procedure, representing a 7.1% improvement.

This demonstrates the importance of evaluating both the multiplier and contractual adjustment rate together. A higher multiplier may not always result in better reimbursement if contractual adjustments are also higher. The net effect depends on the combination of both factors. Healthcare facilities should evaluate the total net reimbursement rather than focusing on individual components.

Payer Contract: Agreement specifying payment terms

Multiplier: Percentage of base charge paid

Contractual Adjustment: Reduction from contracted amount

• Evaluate net reimbursement, not just multiplier

• Consider both positive and negative adjustments

• Negotiate terms that optimize net payment

• Calculate net reimbursement for each option

• Consider volume and mix of services

• Negotiate both components simultaneously

• Focusing only on multiplier rate

• Not considering contractual adjustments

• Not calculating net reimbursement

What is the primary benefit of maintaining denial rates below 5% in healthcare facilities?

The answer is B) It improves cash flow and revenue cycle efficiency. Maintaining low denial rates ensures more claims are paid initially, improving cash flow and reducing the administrative burden of managing denials and resubmissions. This optimizes the revenue cycle and reduces costs associated with claim processing.

Denial management is a critical component of revenue cycle optimization. When claims are denied, they must be investigated, corrected, and resubmitted, which delays payment and increases administrative costs. Facilities with denial rates below 5% typically have streamlined billing processes, accurate coding, and effective pre-service verification systems.

Denial Rate: Percentage of claims rejected by payers

Revenue Cycle: Process from service to payment

Cash Flow: Timing of revenue receipt

• Target denial rate: < 5%

• Denials delay payment

• Low denials improve efficiency

• Implement real-time eligibility checks

• Train staff on common denial reasons

• Track denial patterns and trends

• Accepting high denial rates as normal

• Not investigating denial root causes

• Inadequate staff training on requirements

Healthcare Operations FAQ

Q: How do contractual adjustments differ from denials in insurance reimbursement?

A: Contractual adjustments and denials are fundamentally different in insurance reimbursement:

Contractual Adjustments: These are predetermined reductions in payment based on payer contracts. They are "write-offs" that providers agree to accept as part of their contract. For example, if a procedure has a base charge of $1,000 but the contract specifies payment at 80% of charges, the $200 difference is a contractual adjustment.

Denials: These are claims that are rejected by the insurance company for various reasons (coding errors, missing prior authorization, etc.). Denials represent potential revenue that is lost unless successfully appealed.

Using our formula: Contractual adjustments are applied as factor \( CD \) (permanent reduction), while denials are applied as factor \( DR \) (percentage of claims not paid). Contractual adjustments are planned and permanent, while denials should be minimized through proper billing practices.

Q: What's the relationship between prior authorizations and reimbursement rates?

A: Prior authorizations significantly impact reimbursement rates through the factor \( PC \) (Prior Authorization Corrections) in our formula: \( IR = (BC \times PM) \times (1 - DR) \times (1 - CD) \times (1 + AD) \times (1 - PC) \).

When prior authorization is required but not obtained:

• Claim may be denied entirely (affecting \( DR \))

• Claim may be paid at a reduced rate

• Additional documentation may be required

For a procedure with base charge of $1,000 and 80% multiplier:

Without prior auth (PC = 0.15): \( IR = (1000 \times 0.8) \times (1 - 0.15) = \$680 \)

With prior auth (PC = 0.02): \( IR = (1000 \times 0.8) \times (1 - 0.02) = \$784 \)

That's a difference of $104 per procedure. Proper prior authorization management can significantly improve reimbursement rates.