Procedure Cost Calculator

Healthcare operations tool • 2026 edition

Procedure Cost Formula:

Show the calculator\( PC = (ST + MT + ET + OT) \times (1 + CF) \times (1 - EF) \times (1 + RF) \)

Where:

- \( PC \) = Procedure Cost ($)

- \( ST \) = Staff Time Cost (labor)

- \( MT \) = Materials and Supplies Cost

- \( ET \) = Equipment Time Cost

- \( OT \) = Operating Time Cost (facility overhead)

- \( CF \) = Complexity Factor (procedure difficulty)

- \( EF \) = Efficiency Factor (process optimization)

- \( RF \) = Resource Factor (scarce resources)

This formula calculates total procedure costs based on direct and indirect expenses. Healthcare facilities use this to determine pricing, budget allocation, and operational efficiency. Costs vary significantly based on procedure complexity and resource requirements.

Example: For a procedure with \( ST = \$800 \), \( MT = \$400 \), \( ET = \$300 \), \( OT = \$200 \), complexity factor of 0.15, efficiency factor of 0.1 (10% improvement), and resource factor of 0.05:

\( PC = (800 + 400 + 300 + 200) \times (1 + 0.15) \times (1 - 0.1) \times (1 + 0.05) = 1700 \times 1.15 \times 0.9 \times 1.05 = \$1,860 \)

Thus, the total procedure cost would be $1,860.

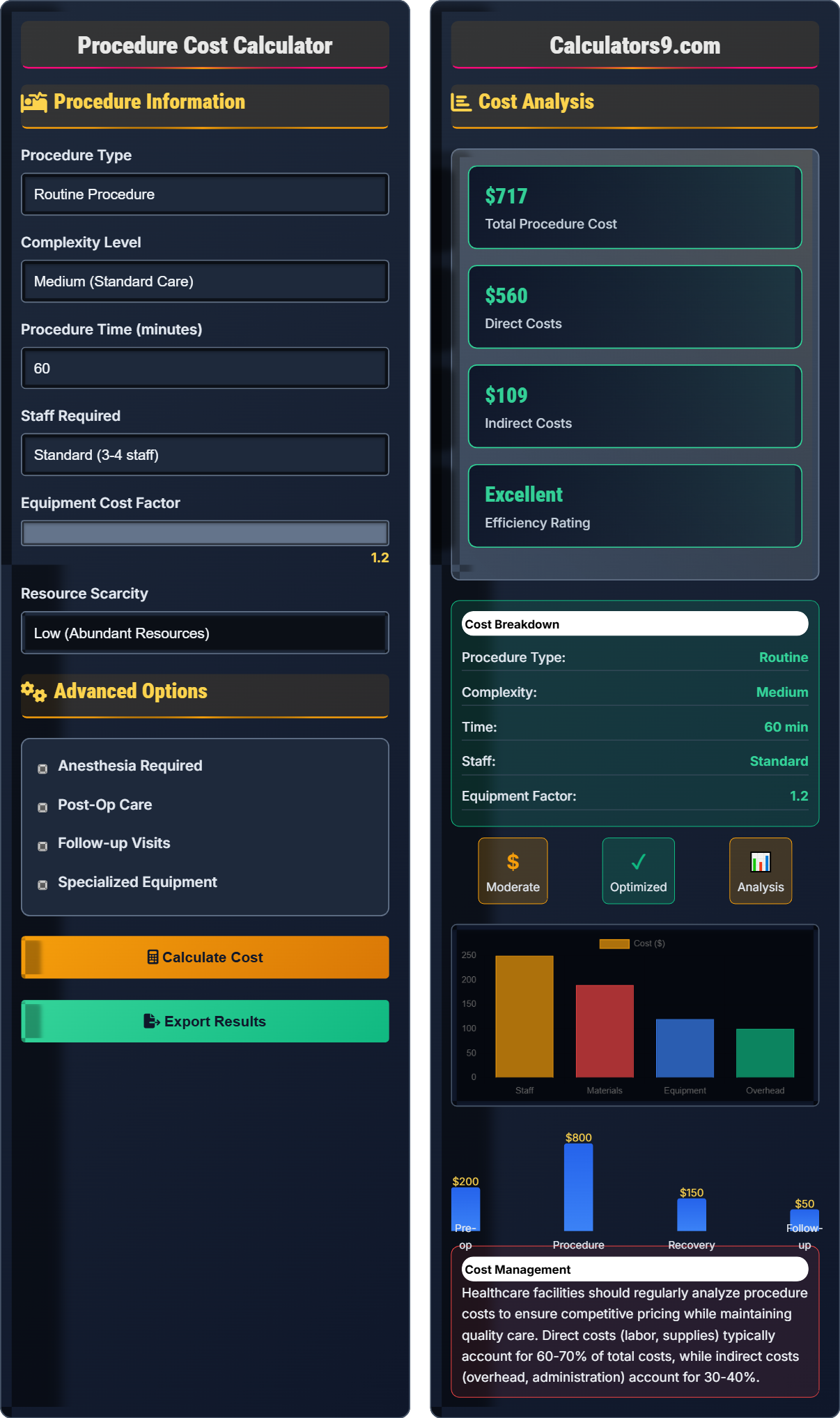

Procedure Information

Advanced Options

Cost Analysis

Healthcare facilities should regularly analyze procedure costs to ensure competitive pricing while maintaining quality care. Direct costs (labor, supplies) typically account for 60-70% of total costs, while indirect costs (overhead, administration) account for 30-40%.

Procedure Cost Framework

Healthcare procedure costing involves analyzing all direct and indirect expenses associated with delivering patient care. Accurate cost calculation is essential for pricing, budgeting, and operational efficiency. Costs are typically categorized into labor, materials, equipment, and facility overhead.

The standard healthcare procedure cost calculation uses the following formula:

Where:

- \(PC\) = Procedure Cost

- \(ST\) = Staff Time Cost

- \(MT\) = Materials and Supplies Cost

- \(ET\) = Equipment Time Cost

- \(OT\) = Operating Time Cost

- \(CF\) = Complexity Factor

- \(EF\) = Efficiency Factor

- \(RF\) = Resource Factor

Healthcare facilities track various metrics related to procedure costs:

- Cost per Case: Total cost divided by number of procedures

- Direct vs. Indirect: Ratio of direct to indirect costs

- Material Utilization: Efficiency of supply usage

- Labor Productivity: Cases per labor hour

- Equipment Utilization: Usage efficiency and ROI

- Cost Variance: Actual vs. budgeted cost differences

- Standardization: Consistent protocols and supply usage

- Bulk Purchasing: Volume discounts for supplies

- Efficiency Training: Reduce procedural time

- Technology Integration: Automation and digital tools

- Supply Chain Management: Optimize inventory and sourcing

- Performance Analytics: Monitor and improve metrics

Cost Framework

Direct labor, materials, equipment, and facility overhead determine procedure costs.

\(PC = (ST + MT + ET + OT) \times (1 + CF) \times (1 - EF) \times (1 + RF)\)

Where PC=procedure cost, ST=staff time, MT=materials, ET=equipment, OT=operating time, CF=complexity factor, EF=efficiency factor, RF=resource factor.

- Direct costs: 60-70% of total

- Indirect costs: 30-40% of total

- Labor: 25-35% of direct costs

Cost Analysis

Procedure type, complexity, and resource availability influence total costs.

- Identify all cost components

- Calculate direct costs

- Add indirect costs

- Apply adjustment factors

- Complexity increases costs significantly

- Efficiency improvements reduce costs

- Resource scarcity increases costs

Procedure Cost Learning Quiz

Which of the following represents the largest component of direct procedure costs in most healthcare facilities?

The answer is B) Materials and supplies costs. Materials and supplies typically represent 30-40% of total procedure costs, making it the largest direct cost component. This includes consumables, implants, medications, and other supplies used during procedures.

Healthcare procedure costs are typically distributed with materials and supplies as the largest component (30-40%), followed by labor (25-35%), equipment (15-20%), and facility overhead (20-25%). Understanding this distribution helps administrators focus cost reduction efforts on the most impactful areas.

Direct Costs: Expenses directly attributable to a procedure

Materials & Supplies: Consumables used in patient care

Cost Distribution: How expenses are allocated across categories

• Materials: 30-40% of direct costs

• Labor: 25-35% of direct costs

• Equipment: 15-20% of direct costs

• Focus on supply chain optimization

• Negotiate bulk purchasing agreements

• Standardize supply usage

• Underestimating material costs

• Overemphasizing labor costs

• Not tracking supply utilization

Calculate the procedure cost for a surgery with staff time cost of $600, materials cost of $400, equipment cost of $200, operating time cost of $150, complexity factor of 0.25, efficiency factor of 0.1 (10% improvement), and resource factor of 0.08. Show your work.

Using the procedure cost formula: \(PC = (ST + MT + ET + OT) \times (1 + CF) \times (1 - EF) \times (1 + RF)\)

Given:

- ST = $600 (staff time)

- MT = $400 (materials)

- ET = $200 (equipment)

- OT = $150 (operating time)

- CF = 0.25 (complexity factor)

- EF = 0.1 (efficiency factor)

- RF = 0.08 (resource factor)

Step 1: Calculate base cost

Base cost = ST + MT + ET + OT = $600 + $400 + $200 + $150 = $1,350

Step 2: Apply factors

PC = $1,350 × (1 + 0.25) × (1 - 0.1) × (1 + 0.08)

= $1,350 × 1.25 × 0.9 × 1.08

= $1,350 × 1.215 = $1,640.25

The total procedure cost is $1,640.25.

This calculation demonstrates how multiple factors compound to affect total costs. The complexity factor increases costs by 25%, but the efficiency factor reduces them by 10%. The resource factor adds another 8%. Understanding how these factors interact is crucial for accurate cost estimation.

Complexity Factor (CF): Adjusts for procedure difficulty

Efficiency Factor (EF): Reflects process improvements

Resource Factor (RF): Accounts for supply availability

• Calculate base cost first

• Add 1 to positive factors

• Subtract efficiency from 1

• Calculate base cost before applying factors

• Verify factor applications

• Round to nearest dollar for reporting

• Forgetting to add 1 to factors

• Misapplying efficiency factor

• Not following order of operations

A surgical suite performs 200 procedures per month with an average direct cost of $1,500 per procedure. If they implement efficiency improvements that reduce labor time by 15% and material waste by 10%, calculate the monthly cost savings. Assume labor represents 30% of direct costs and materials represent 35% of direct costs.

Step 1: Calculate current monthly costs

Current monthly costs = 200 × $1,500 = $300,000

Step 2: Calculate labor and material costs per procedure

Labor cost per procedure = $1,500 × 0.30 = $450

Material cost per procedure = $1,500 × 0.35 = $525

Step 3: Calculate savings per procedure

Labor savings = $450 × 0.15 = $67.50

Material savings = $525 × 0.10 = $52.50

Total savings per procedure = $67.50 + $52.50 = $120

Step 4: Calculate monthly savings

Monthly savings = 200 × $120 = $24,000

The surgical suite would save $24,000 per month with these efficiency improvements.

This example demonstrates how small percentage improvements in high-cost categories can result in significant savings. Since labor and materials represent 65% of direct costs, improvements in these areas have a disproportionately large impact on total costs. This is why cost management often focuses on these categories first.

Direct Costs: Expenses directly tied to patient care

Efficiency Improvements: Process changes that reduce costs

Cost Savings: Reduction in total expenses

• Focus on high-cost categories

• Calculate per-unit savings first

• Identify highest-cost categories

• Calculate potential savings before implementation

• Monitor actual savings post-implementation

• Not considering cost category distributions

• Underestimating impact of small improvements

• Forgetting to scale per-unit savings

A hospital is considering purchasing new imaging equipment that costs $2 million and would reduce procedure time by 20% for 500 procedures per year. Current average procedure time is 90 minutes with labor cost of $2 per minute. The equipment has an annual operating cost of $150,000 and a 5-year useful life. Calculate the net present value of this investment assuming a 10% discount rate. Should the hospital proceed?

Step 1: Calculate annual labor savings

Time saved per procedure = 90 × 0.20 = 18 minutes

Labor savings per procedure = 18 × $2 = $36

Annual labor savings = 500 × $36 = $18,000

Step 2: Calculate net annual benefit

Net annual benefit = $18,000 - $150,000 = -$132,000

Step 3: Calculate NPV

Initial investment = $2,000,000

Annual net benefit = -$132,000 for 5 years

NPV = -$2,000,000 + Σ[$132,000/(1.10)^t] for t=1 to 5

NPV = -$2,000,000 + [-$132,000 × 3.791] = -$2,000,000 + (-$500,412) = -$2,500,412

The negative NPV suggests the hospital should not proceed with this investment as currently structured.

This demonstrates the importance of comprehensive financial analysis before equipment purchases. While the equipment reduces procedure time and labor costs, the high operating costs outweigh the savings. The NPV calculation reveals that the investment would not be financially beneficial. Hospitals should consider alternative financing options or different equipment that offers better economics.

Net Present Value (NPV): Present value of future cash flows

Equipment ROI: Return on investment for capital equipment

Operating Costs: Annual costs to operate equipment

• Consider all costs and benefits

• Include operating expenses

• Use appropriate discount rate

• Perform sensitivity analysis

• Consider volume changes

• Include intangible benefits

• Only considering cost savings

• Ignoring operating expenses

• Not performing NPV analysis

What is the primary purpose of tracking cost variance in healthcare procedure costing?

The answer is B) To identify inefficiencies and opportunities for improvement. Cost variance analysis compares actual costs to budgeted or standard costs, revealing areas where operations deviate from expectations. This information helps managers identify inefficiencies, control costs, and improve operational performance.

Cost variance analysis is a fundamental management accounting technique in healthcare. Positive variances (actual > budgeted) indicate opportunities for improvement, while negative variances (actual < budgeted) may indicate successful cost management or potential quality concerns. The goal is to understand causes of variance and implement appropriate management actions.

Cost Variance: Difference between actual and budgeted costs

Management Accounting: Internal financial analysis for decision-making

Operational Performance: How efficiently resources are used

• Investigate significant variances

• Understand root causes

• Implement corrective actions

• Track variances regularly

• Focus on actionable items

• Include quality metrics

• Not investigating variances

• Focusing only on cost reduction

• Ignoring quality implications

Healthcare Operations FAQ

Q: How does procedure complexity affect overall costs?

A: Procedure complexity significantly impacts costs through multiple pathways. The complexity factor \( CF \) in our formula \( PC = (ST + MT + ET + OT) \times (1 + CF) \times (1 - EF) \times (1 + RF) \) accounts for:

• Extended procedural time requiring more staff hours

• Specialized equipment and supplies

• Higher-skilled personnel with premium wages

• Increased risk requiring additional safety measures

For example, a high-complexity procedure with \( CF = 0.5 \) increases costs by 50% compared to standard procedures. A procedure with base cost of $1,000 would cost $1,500 with high complexity. This is why healthcare facilities often charge significantly more for complex procedures and why cost accounting must incorporate complexity factors.

Q: What's the relationship between efficiency improvements and procedure costs?

A: Efficiency improvements directly reduce procedure costs through the efficiency factor \( EF \) in our formula. Efficiency improvements can come from:

• Standardized protocols reducing variability

• Staff training reducing procedural time

• Technology integration automating tasks

• Workflow optimization minimizing delays

For a procedure with base cost of $2,000:

Without improvements (EF = 0): Total cost = $2,000

With 15% efficiency improvement (EF = 0.15): Total cost = $2,000 × (1 - 0.15) = $1,700

This represents $300 in savings per procedure. For 1,000 procedures annually, the facility would save $300,000. The efficiency factor works multiplicatively with other factors, making it especially valuable when combined with other improvements.