Auto Insurance Quote Estimator

Fast coverage calculator • 2026 rates

Auto Insurance Premium Formula:

Show the calculator\( P = B \times (1 + R_d) \times (1 + R_a) \times (1 + R_m) \times (1 + R_v) \times (1 + R_l) \)

Where:

- \( P \) = Final Premium

- \( B \) = Base Rate (typically $500-$1500 annually)

- \( R_d \) = Driver Risk Factor (age, driving record)

- \( R_a \) = Area Risk Factor (location-based)

- \( R_m \) = Vehicle Risk Factor (make, model, age)

- \( R_v \) = Coverage Level Factor (coverage limits)

- \( R_l \) = Loyalty/Credit Factor (discounts)

This formula calculates the comprehensive auto insurance premium by multiplying the base rate by various risk multipliers that reflect individual circumstances.

Example: For a base rate of \( B = \$800 \) with driver risk factor \( R_d = 0.30 \), area risk \( R_a = 0.20 \), vehicle risk \( R_m = 0.15 \), coverage factor \( R_v = 0.40 \), and loyalty discount \( R_l = -0.10 \):

\( P = 800 \times (1 + 0.30) \times (1 + 0.20) \times (1 + 0.15) \times (1 + 0.40) \times (1 - 0.10) \)

\( P = 800 \times 1.30 \times 1.20 \times 1.15 \times 1.40 \times 0.90 \approx \$1,609 \)

Thus, the annual premium would be approximately $1,609.

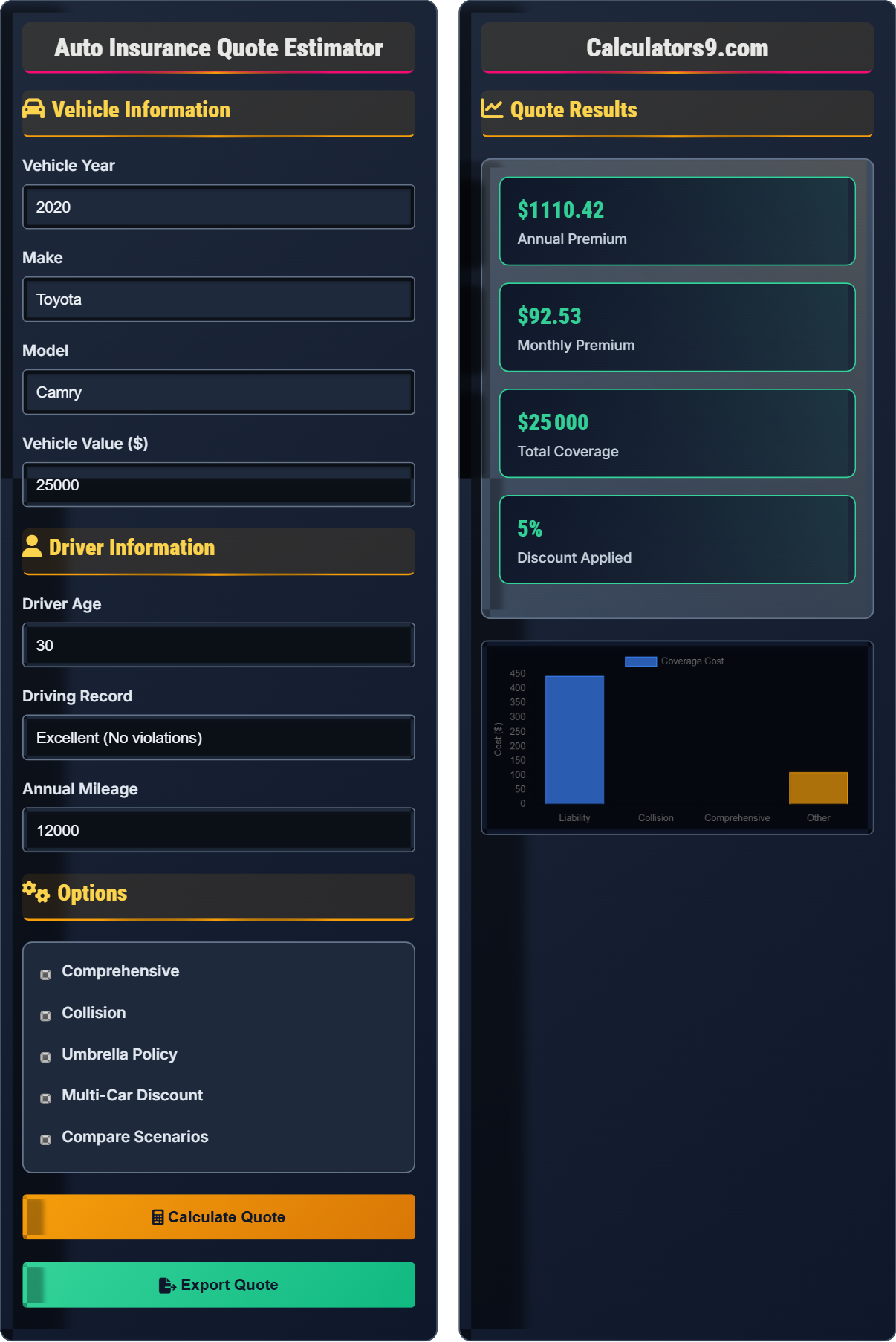

Vehicle Information

Driver Information

Options

Quote Results

| Component | Factor | Amount |

|---|

| Coverage Type | Limit | Cost |

|---|

Comprehensive Auto Insurance Guide

Auto insurance is a contract between you and an insurance company that protects you against financial loss in case of an accident. It covers property damage, liability, medical expenses, and other related costs. The policyholder pays a premium to the insurer in exchange for coverage protection.

Auto insurance premiums are calculated based on multiple factors:

Where:

- \(P\) = Final Premium

- \(B\) = Base Rate

- \(R_d\) = Driver Risk Multiplier

- \(R_a\) = Area Risk Multiplier

- \(R_m\) = Vehicle Risk Multiplier

- \(R_v\) = Coverage Level Multiplier

- \(R_l\) = Loyalty/Discount Multiplier

Your auto insurance premium is influenced by several key factors:

- Driving Record: Traffic violations, accidents, and claims history

- Location: Where you live affects risk of accidents and theft

- Vehicle Type: Make, model, age, and safety features

- Mileage: More driving means higher risk exposure

- Credit Score: Many insurers use credit history as a risk indicator

- Deductibles: Higher deductibles typically mean lower premiums

- Bundle policies: Combine auto and home insurance for discounts

- Maintain good credit: Improves your insurance score

- Take defensive driving courses: Qualify for safe driver discounts

- Choose higher deductibles: Reduce premium in exchange for higher out-of-pocket costs

- Shop around annually: Compare quotes from multiple insurers

- Drive safely: Maintain a clean driving record for best rates

Auto Insurance Learning Quiz

Which type of auto insurance coverage pays for damage to your own vehicle in an accident where you are at fault?

The answer is B) Collision Coverage. Collision coverage pays for damage to your vehicle regardless of who is at fault in an accident involving another vehicle or object. Liability coverage only pays for damage you cause to others, not your own vehicle.

Understanding the difference between collision and comprehensive coverage is fundamental to auto insurance literacy. Collision coverage specifically addresses accidents involving vehicles or objects (like hitting a tree), while comprehensive covers non-collision events like theft, vandalism, or natural disasters. This distinction helps policyholders make informed decisions about their coverage needs.

Collision Coverage: Insurance that pays for damage to your car in an accident involving another vehicle or object

Liability Coverage: Insurance that pays for damage you cause to others

Comprehensive Coverage: Insurance that covers non-collision damage like theft or weather

• Collision coverage pays for your vehicle regardless of fault

• Liability coverage does not cover your own vehicle damage

• Collision is often required if you finance or lease your car

• Remember: Collision = Crashes with cars/objects

• Collision covers both at-fault and not-at-fault accidents

• Consider deductible costs when choosing coverage

• Confusing collision with comprehensive coverage

• Thinking liability covers your own vehicle damage

• Forgetting that collision is separate from liability

Calculate the estimated annual premium for a 25-year-old driver with a $1,000 base rate, excellent driving record (0.20 multiplier), living in a moderate-risk area (0.15 multiplier), driving a mid-range vehicle (0.10 multiplier), with comprehensive coverage (0.30 multiplier), and a 10% loyalty discount (-0.10 multiplier). Show your work.

Using the premium formula: \( P = B \times (1 + R_d) \times (1 + R_a) \times (1 + R_m) \times (1 + R_v) \times (1 + R_l) \)

Given:

- B = $1,000

- R_d = 0.20 (excellent driving record)

- R_a = 0.15 (moderate-risk area)

- R_m = 0.10 (mid-range vehicle)

- R_v = 0.30 (comprehensive coverage)

- R_l = -0.10 (10% loyalty discount)

Step 1: Calculate the multipliers: (1 + 0.20) = 1.20, (1 + 0.15) = 1.15, (1 + 0.10) = 1.10, (1 + 0.30) = 1.30, (1 - 0.10) = 0.90

Step 2: Calculate P = $1,000 × 1.20 × 1.15 × 1.10 × 1.30 × 0.90

Step 3: Calculate sequentially: $1,000 × 1.20 = $1,200

Step 4: $1,200 × 1.15 = $1,380

Step 5: $1,380 × 1.10 = $1,518

Step 6: $1,518 × 1.30 = $1,973.40

Step 7: $1,973.40 × 0.90 = $1,776.06

The estimated annual premium is $1,776.06

This calculation demonstrates how multiple risk factors compound to determine insurance premiums. Each multiplier builds on the previous result, showing how seemingly small percentage adjustments can significantly impact the final premium. The discount factor works differently as a reduction rather than addition, showing how insurers incentivize good behavior.

Base Rate: The starting premium before adjustments

Risk Multiplier: A factor that increases or decreases the base rate

Loyalty Discount: A reduction in premium for long-term customers

• Risk multipliers are additive to 1 (e.g., 0.20 becomes 1.20)

Jennifer has a 2015 Honda Civic worth $8,000 with a loan balance of $5,000. She's considering dropping collision and comprehensive coverage to save $400 annually. Is this financially wise? Assume her deductible is $500.

Step 1: Calculate potential savings vs. risk exposure

Annual savings: $400

Potential maximum payout if totaled: $8,000 (vehicle value) - $500 (deductible) = $7,500

Step 2: Consider the loan balance: If the car is totaled, she still owes $5,000 but only receives $8,000, leaving her with a positive equity position.

Step 3: However, if the car is stolen or severely damaged, she would lose $8,000 in asset value for $400 annual savings.

Step 4: Calculate break-even: $8,000 ÷ $400 = 20 years (meaning she'd need to go 20 years without an incident to break even on the savings).

Conclusion: Dropping coverage is risky unless Jennifer has sufficient emergency savings to replace the vehicle if it's totaled or stolen. The financial exposure ($7,500) far exceeds the annual savings ($400).

This example illustrates the cost-benefit analysis needed when deciding on coverage levels. The decision isn't just about the premium savings but also about the financial exposure if an incident occurs. The break-even analysis shows how to quantify the risk, helping students understand that insurance is about managing financial uncertainty rather than just finding the lowest premium.

Deductible: The amount you pay out-of-pocket before insurance kicks in

Financial Exposure: The maximum potential loss in an adverse event

Break-even Analysis: Calculating how long it would take to recover costs through savings

• Consider asset value vs. premium savings when dropping coverage

• Factor in loan balances when making coverage decisions

• Evaluate both probability and severity of potential losses

• Use the 10% rule: If premium exceeds 10% of car value, consider dropping coverage

• Keep full coverage if car is financed or leased

• Maintain emergency fund equal to vehicle replacement cost

• Focusing only on premium savings without considering exposure

• Forgetting to factor in loan balances when evaluating coverage

• Not considering the emotional and logistical impact of vehicle loss

Mark is a 19-year-old college student with a sports car who commutes 25 miles daily through a busy city. His friend Tom is a 35-year-old with a family sedan who drives 5 miles to work in a suburban area. Both have clean driving records. Who will likely pay higher premiums and why? Calculate approximate premium differences assuming a base rate of $1,000.

Step 1: Analyze risk factors for Mark:

• Age (19): High risk (+0.50 multiplier)

• Vehicle (sports car): High risk (+0.40 multiplier)

• Location (busy city): High risk (+0.35 multiplier)

• Mileage (25 miles daily): High exposure (+0.20 multiplier)

Step 2: Analyze risk factors for Tom:

• Age (35): Low risk (+0.05 multiplier)

• Vehicle (family sedan): Low risk (+0.05 multiplier)

• Location (suburban): Low risk (+0.10 multiplier)

• Mileage (5 miles): Low exposure (+0.05 multiplier)

Step 3: Calculate Mark's premium: $1,000 × 1.50 × 1.40 × 1.35 × 1.20 = $3,402

Step 4: Calculate Tom's premium: $1,000 × 1.05 × 1.05 × 1.10 × 1.05 = $1,276

Step 5: Difference: $3,402 - $1,276 = $2,126

Mark will pay approximately $2,126 more annually due to higher risk factors.

This demonstrates how multiple risk factors compound to dramatically affect premiums. Age alone can double or triple premiums for young drivers, while location and vehicle type can add significant additional costs. The multiplicative effect of risk factors explains why premiums can vary so widely between similar individuals with different circumstances.

Risk Factor: A characteristic that influences insurance premium calculations

Risk Multiplier: A numerical value that adjusts the base premium

Exposure: The likelihood of an insurance claim based on usage patterns

• Young drivers face significantly higher premiums

• Sports cars carry higher premiums than sedans

• Urban areas typically have higher premiums than suburban areas

• Students can save by staying on parents' policy

• Choose safer vehicles to reduce premiums

• Consider public transportation to reduce mileage

• Underestimating how age affects premiums

• Not considering location impact on premiums

• Ignoring how vehicle choice affects insurance costs

Which statement about deductibles is TRUE?

The answer is B) Lower deductibles mean lower out-of-pocket costs in accidents. A deductible is the amount you pay out-of-pocket before insurance coverage kicks in. So with a $500 deductible, you pay $500 and the insurance covers the rest. With a $1,000 deductible, you pay $1,000 before insurance coverage begins.

Understanding the inverse relationship between deductibles and premiums is crucial for insurance planning. Higher deductibles reduce premiums because the insurer bears less risk for smaller claims. However, they increase your financial responsibility in case of an accident. This trade-off requires balancing monthly affordability with emergency preparedness.

Deductible: The amount you pay before insurance coverage begins

Out-of-pocket: Expenses you pay directly, not covered by insurance

Trade-off: The balance between premium savings and increased risk

• Higher deductibles = Lower premiums (and vice versa)

• Deductibles apply to collision and comprehensive coverage

• Liability coverage typically doesn't have a deductible

• Choose deductible you can afford to pay immediately

• Consider emergency fund when selecting deductible

• Higher deductibles make sense for safe drivers

• Choosing a deductible too high for your emergency fund

• Confusing deductible with premium

• Thinking deductibles apply to all coverage types

Insurance Basics

Contract protecting against financial loss from vehicle accidents.

\( P = B \times (1 + R_d) \times (1 + R_a) \times (1 + R_m) \times (1 + R_v) \times (1 + R_l) \)

Where P=premium, B=base rate, Rd=driver risk, Ra=area risk, Rm=vehicle risk, Rv=coverage risk, Rl=loyalty factor.

- Risk multipliers compound multiplicatively

- Higher deductibles = Lower premiums

- Younger drivers pay more

Coverage Types

Required in most states, covers damage you cause to others.

- Collision: Damage to your vehicle

- Comprehensive: Non-collision damage

- Uninsured Motorist: Protection from uninsured drivers

- Personal Injury Protection: Medical expenses

- Required minimums vary by state

- Full coverage recommended for financed vehicles

- Consider umbrella policies for additional protection

- Compare quotes annually

FAQ

Q: Why do young drivers pay significantly more for auto insurance?

A: Young drivers pay more because statistical data shows they have higher accident rates. Insurance companies use actuarial data that demonstrates drivers under 25, particularly those aged 16-19, are significantly more likely to be involved in accidents due to:

- Lack of driving experience

- Increased risk-taking behavior

- Higher likelihood of distracted driving

- Less developed hazard recognition skills

Mathematically, if the base rate is \( B = \$1,000 \) and the age risk multiplier for a 19-year-old is \( R_d = 0.50 \), then the premium becomes \( P = B \times (1 + R_d) = \$1,000 \times 1.50 = \$1,500 \). This represents a 50% increase due solely to age.

Young drivers can reduce premiums by maintaining good grades (good student discount), completing driver education courses, and staying on parents' policies.

Q: When should I consider dropping collision and comprehensive coverage?

A: Consider dropping collision and comprehensive coverage when the annual premium for these coverages exceeds 10% of your vehicle's value. For example, if your car is worth $5,000 and your collision/comprehensive premium is $600 annually, the ratio is 12% ($600 ÷ $5,000), suggesting you might consider dropping the coverage.

However, consider these factors:

- Is your car financed or leased? (Usually required)

- Do you have emergency funds to replace the vehicle?

- How much would you lose if the car were totaled?

- Are you comfortable with the financial risk?

The break-even calculation: If you save $500 annually by dropping coverage but face a $5,000 loss if the car is totaled, you'd need to go 10 years without an incident to come out ahead ($5,000 ÷ $500 = 10 years).