Claim Settlement Calculator

Fast settlement estimator • 2026 rates

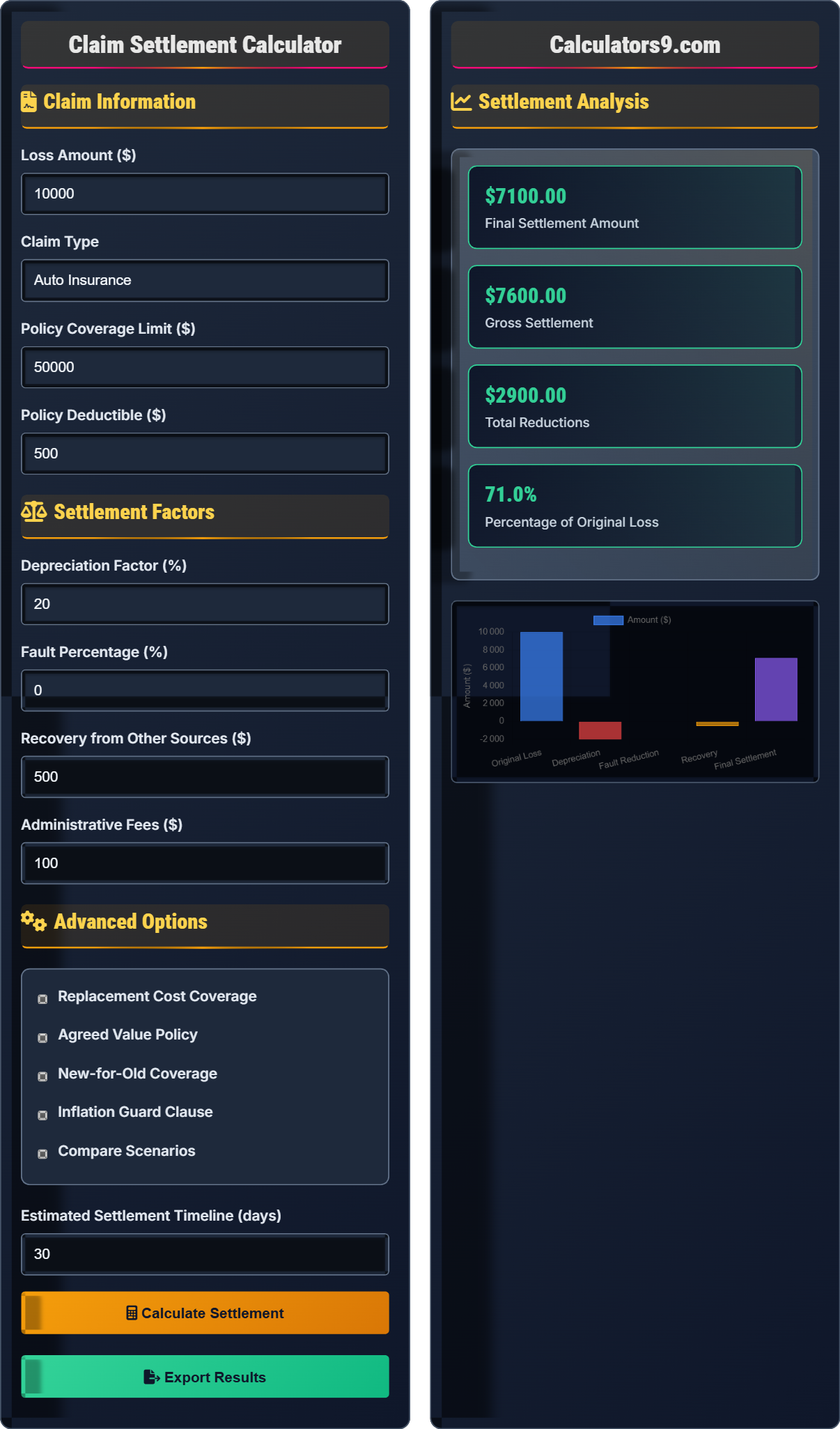

Claim Settlement Formula:

Show the calculator\( S = L \times (1 - D) \times (1 - F) \times (1 - R) \times (1 - A) \)

Where:

- \( S \) = Settlement Amount

- \( L \) = Loss Amount (actual damage/cost)

- \( D \) = Depreciation Factor (for property replacement)

- \( F \) = Fault Percentage (liability share)

- \( R \) = Recovery Factor (from other sources)

- \( A \) = Administrative Deductions (processing fees, etc.)

This formula calculates the final settlement amount by adjusting the loss amount for various factors that reduce the payout.

Example: For a loss of \( L = \$10,000 \) with 20% depreciation \( D = 0.20 \), 30% fault \( F = 0.30 \), 10% recovery \( R = 0.10 \), and 5% administrative deductions \( A = 0.05 \):

\( S = 10000 \times (1 - 0.20) \times (1 - 0.30) \times (1 - 0.10) \times (1 - 0.05) \)

\( S = 10000 \times 0.80 \times 0.70 \times 0.90 \times 0.95 \approx \$4,788 \)

Thus, the final settlement amount would be approximately $4,788.

Claim Information

Settlement Factors

Advanced Options

Settlement Analysis

| Component | Calculation | Amount |

|---|

| Factor | Value | Impact |

|---|

| Milestone | Timeframe | Status |

|---|

Comprehensive Claim Settlement Guide

A claim settlement is the amount paid by an insurance company to resolve a claim. Settlements are calculated based on policy terms, actual losses, and various adjustment factors.

Claim settlements are calculated using:

Where:

- \( S \) = Settlement Amount

- \( L \) = Loss Amount

- \( D \) = Depreciation Factor

- \( F \) = Fault Percentage

- \( R \) = Recovery Factor

- \( A \) = Administrative Deductions

Claim settlement processes typically follow these timelines:

- Initial Reporting: Within 24-48 hours of loss

- Investigation: 7-14 days for simple claims, 30+ days for complex

- Estimation: 5-10 business days after inspection

- Settlement Offer: 15-30 days after estimate

- Final Payment: 5-10 days after agreement

- Document Everything: Photos, receipts, and records

- Understand Policy Terms: Know your coverage limits and exclusions

- Get Multiple Estimates: For repair/replacement costs

- Appeal if Necessary: Don't accept lowball offers without challenge

- Consider Public Adjusters: For complex or high-value claims

- Keep Detailed Records: Of all communications and expenses

Claim Settlement Learning Quiz

Which factor would result in a LOWER settlement amount?

The answer is B) High depreciation. Depreciation reduces the settlement amount by accounting for the age and wear of the damaged property. The higher the depreciation percentage, the lower the settlement amount.

Understanding how depreciation affects settlements is crucial for policyholders. Depreciation is calculated based on the age of the item and its expected useful life. For example, a 5-year-old roof with a 20-year expected life would have 25% depreciation, meaning the insurance company would only pay 75% of the replacement cost.

Depreciation: Reduction in value due to age and wear

Replacement Cost: Cost to replace item with new one

Actual Cash Value: Replacement cost minus depreciation

• Higher depreciation = Lower settlement

• Replacement cost coverage avoids depreciation

• Depreciation is calculated based on useful life

• Request replacement cost coverage to avoid depreciation

• Document item age and condition for accurate depreciation

• Consider upgrading to replacement cost coverage

• Confusing replacement cost with actual cash value

• Not understanding how depreciation is calculated

• Accepting actual cash value without considering replacement cost

Calculate the settlement amount for a $15,000 loss with 25% depreciation, 0% fault, $1,000 recovery from other sources, and $200 administrative fees. Show your work.

Using the settlement formula: \( S = L \times (1 - D) \times (1 - F) \times (1 - R) \times (1 - A) \)

Given:

- L = $15,000

- D = 0.25 (25% depreciation)

- F = 0.00 (0% fault)

- R = $1,000 ÷ $15,000 = 0.067 (recovery factor)

- A = $200 ÷ $15,000 = 0.013 (administrative factor)

Step 1: Calculate the multipliers: (1 - 0.25) = 0.75, (1 - 0.00) = 1.00, (1 - 0.067) = 0.933, (1 - 0.013) = 0.987

Step 2: Calculate S = $15,000 × 0.75 × 1.00 × 0.933 × 0.987

Step 3: Calculate sequentially: $15,000 × 0.75 = $11,250

Step 4: $11,250 × 1.00 = $11,250

Step 5: $11,250 × 0.933 = $10,496.25

Step 6: $10,496.25 × 0.987 = $10,360.00

The settlement amount is $10,360.00

This calculation demonstrates how multiple factors compound to determine the final settlement amount. Each multiplier builds on the previous result, showing how seemingly small percentage adjustments can significantly impact the final settlement. The formula accounts for all the major reduction factors that affect claim payouts.

Settlement Amount: Final amount paid to settle a claim

Loss Amount: Initial assessed value of the damage

Reduction Factors: Elements that decrease the settlement

• Reduction factors multiply, not add

• Each factor reduces the previous amount

• Recovery amounts reduce the settlement

• Remember to convert percentages to decimals when calculating

• Apply factors sequentially for accuracy

• Consider all possible reduction factors

• Adding reduction factors instead of multiplying them

• Forgetting to convert percentages to decimals

• Not accounting for all reduction factors

Sarah files a claim for $75,000 in property damage. Her policy has a $50,000 coverage limit and a $1,000 deductible. She has replacement cost coverage with no depreciation. What is her settlement amount and how much will she pay out-of-pocket?

Step 1: Determine the applicable loss amount

Policy limit: $50,000

Actual loss: $75,000

Since the loss exceeds the policy limit, the settlement is capped at the policy limit.

Step 2: Apply the deductible

Settlement = Policy limit - Deductible

Settlement = $50,000 - $1,000 = $49,000

Step 3: Calculate out-of-pocket costs

Out-of-pocket = Total loss - Settlement

Out-of-pocket = $75,000 - $49,000 = $26,000

Step 4: Conclusion

Sarah will receive a settlement of $49,000 and will pay $26,000 out-of-pocket for the $75,000 loss.

This example demonstrates the importance of adequate coverage limits. When losses exceed policy limits, the policyholder is responsible for the difference. This is why it's crucial to regularly review and update coverage limits to match current replacement costs and potential exposures.

Policy Limit: Maximum amount insurer will pay under policy

Deductible: Amount paid by policyholder before coverage appliesOut-of-Pocket: Expenses paid directly by policyholder

• Settlement cannot exceed policy limits

• Deductible reduces the settlement amount

• Policyholder pays difference when limits are exceeded

• Regularly review policy limits for adequacy

• Consider inflation when setting limits

• Understand the difference between replacement cost and actual cash value

• Not understanding policy limits

• Forgetting to account for deductibles

• Assuming full loss will be covered

Mike's car is totaled in an accident caused by another driver. The actual cash value of his car is $20,000, with $1,000 depreciation bringing it to $19,000. His insurance pays him $19,000 minus a $500 deductible ($18,500). Later, his insurance recovers $15,000 from the at-fault driver's insurance. How much of this recovery will Mike receive?

Step 1: Calculate the initial payment to Mike

Car value: $20,000

Depreciation: $1,000

Actual cash value: $19,000

Payment after deductible: $19,000 - $500 = $18,500

Step 2: Analyze subrogation recovery

Insurance recovered: $15,000

Step 3: Determine distribution

Typically, in subrogation cases:

Insurance company recovers their payment first: $18,500

Remaining recovery: $15,000 - $18,500 = -$3,500 (negative means full recovery paid to insurer)

Step 4: Conclusion

Mike will receive $0 from the recovery since the amount recovered ($15,000) is less than what the insurance company paid him ($18,500). The entire $15,000 goes to the insurance company.

This demonstrates the principle of subrogation, where the insurance company steps into the shoes of the insured to recover from the party responsible for the loss. The insurance company has the right to recover the amounts they paid, up to the amount recovered from the responsible party.

Subrogation: Insurer's right to recover from responsible party

Third Party Recovery: Compensation from other insurers/responsible parties

Right of Recovery: Insurer's legal right to seek compensation

• Insurance companies recover their payments first

• Policyholder may receive excess recovery

• Subrogation prevents double recovery

• Understand subrogation rights in your policy

• Cooperate with insurer's subrogation efforts

• Keep records of all related expenses

• Expecting to keep all subrogation recoveries

• Not understanding insurer's recovery rights

• Accepting settlements without considering subrogation

Which statement about deductibles is TRUE?

The answer is B) Deductibles reduce the settlement amount. A deductible is the amount you pay out-of-pocket before insurance coverage kicks in. So if your settlement is $10,000 and your deductible is $500, you'll receive $9,500 after the deductible is applied.

Understanding the inverse relationship between deductibles and settlements is crucial for insurance planning. Higher deductibles reduce premiums because the insurer bears less risk for smaller claims. However, they also reduce the settlement amount received for each claim. This trade-off requires balancing monthly affordability with potential claim costs.

Deductible: Amount paid before insurance coverage begins

Out-of-pocket: Expenses paid directly, not covered by insurance

Trade-off: Balance between premium savings and claim reduction

• Higher deductibles = Lower premiums (and vice versa)

• Deductibles reduce settlement amounts

• Deductibles apply to property and casualty insurance

• Choose deductible you can afford to pay immediately

• Consider emergency fund when selecting deductible

• Higher deductibles make sense for safe drivers/properties

• Choosing a deductible too high for your emergency fund

• Confusing deductible with premium

• Thinking deductibles apply to all coverage types

Settlement Basics

Amount paid by insurer to resolve a covered loss.

\( S = L \times (1 - D) \times (1 - F) \times (1 - R) \times (1 - A) \)

Where S=settlement, L=loss amount, D=depreciation, F=fault, R=recovery, A=administrative deductions.

- Settlements cannot exceed policy limits

- Reduction factors multiply, not add

- Deductibles reduce settlement amounts

Settlement Factors

Reduction in value due to age and wear.

- Policy Limits: Maximum coverage amount

- Deductibles: Amount paid by policyholder

- Subrogation: Recovery from responsible parties

- Salvage Value: Remaining worth of damaged property

- Replacement cost avoids depreciation

- Higher coverage limits provide better protection

- Subrogation prevents double recovery

- Salvage value reduces settlement amount

FAQ

Q: How long does the claim settlement process typically take?

A: The claim settlement process typically follows this timeline:

- Initial Reporting: Within 24-48 hours of loss

- Investigation: 7-14 days for simple claims, 30+ days for complex

- Estimation: 5-10 business days after inspection

- Settlement Offer: 15-30 days after estimate

- Final Payment: 5-10 days after agreement

Simple auto claims might settle in 2-3 weeks, while complex property damage claims can take 2-6 months. The timeline depends on factors like:

- Complexity of the loss

- Availability of documentation

- Need for expert assessments

- Presence of disputes

Mathematically, if we define the total settlement time as \( T \), it can be expressed as: \( T = T_r + T_i + T_e + T_s + T_p \), where each \( T \) represents the time for reporting, investigation, estimation, settlement offer, and payment respectively.

Q: How can I maximize my settlement amount?

A: To maximize your settlement amount:

- Document Everything: Take photos before and after the loss, keep receipts for repairs and temporary measures

- Understand Policy Terms: Know your coverage limits, exclusions, and special endorsements

- Get Multiple Estimates: Obtain repair/replacement estimates from licensed contractors

- Consider Upgrades: Upgrade to replacement cost coverage if you currently have actual cash value

- Keep Detailed Records: Document all communication with the insurance company

- Appeal if Necessary: Don't accept lowball offers without challenging them

For example, if your actual loss is \( L = \$10,000 \) but the insurance company offers only \( S = \$7,000 \), the difference of \( \$3,000 \) might be due to:

- Incorrect depreciation calculations

- Undervalued replacement costs

- Failure to consider inflation guard clauses

By providing detailed documentation and accurate estimates, you can often negotiate a settlement closer to the actual loss amount.