Deductible Savings Calculator

Fast comparison tool • 2026 rates

Deductible Savings Formula:

Show the calculator\( \text{Savings} = (\text{Premium}_{\text{low}} - \text{Premium}_{\text{high}}) \times \text{Years} - (\text{Deductible}_{\text{high}} - \text{Deductible}_{\text{low}}) \times \text{Claims} \)

Where:

- \( \text{Premium}_{\text{low}} \) = Annual premium with low deductible

- \( \text{Premium}_{\text{high}} \) = Annual premium with high deductible

- \( \text{Deductible}_{\text{low}} \) = Low deductible amount

- \( \text{Deductible}_{\text{high}} \) = High deductible amount

- \( \text{Years} \) = Number of years in the plan

- \( \text{Claims} \) = Number of claims filed

This formula calculates the net financial impact of choosing a high-deductible plan versus a low-deductible plan, considering both premium savings and potential out-of-pocket costs.

Example: For a $1,000 annual premium difference with 2 years in the plan and $2,000 deductible difference with 1 claim:

\( \text{Savings} = (2000 - 1000) \times 2 - (5000 - 3000) \times 1 = 2000 - 2000 = 0 \)

Thus, the net savings would be $0 (break-even).

Plan Information

Claim Information

Advanced Options

Savings Analysis

| Category | Low Deductible | High Deductible | Difference |

|---|

| Year | Premium Saved | Out-of-Pocket | Net Impact |

|---|

| Scenario | Claims Frequency | Net Impact | Recommendation |

|---|

Comprehensive Deductible Planning Guide

A deductible is the amount you pay out-of-pocket for covered healthcare services before your insurance begins to pay. Choosing the right deductible involves balancing monthly premiums with potential out-of-pocket costs.

The financial impact of choosing different deductible levels can be calculated using:

Where:

- \( \text{Net Impact} \) = Overall financial impact (positive = savings, negative = cost)

- \( \text{Premium}_{\text{low}} \) = Annual premium for low deductible plan

- \( \text{Premium}_{\text{high}} \) = Annual premium for high deductible plan

- \( \text{Deductible}_{\text{low}} \) = Low deductible amount

- \( \text{Deductible}_{\text{high}} \) = High deductible amount

- \( \text{Years} \) = Expected plan duration

- \( \text{Claims} \) = Number of claims expected

Choose based on your specific circumstances:

- Low Deductible: Frequent medical care, chronic conditions, large families

- High Deductible: Good health, emergency fund available, HSA eligibility desired

- Break-even Calculation: Divide premium savings by deductible difference to find break-even claims

- Rule of Thumb: If you expect more than 1 major claim per year, lower deductible may be better

- Build an Emergency Fund: Save for your deductible amount plus copays and coinsurance

- Consider HSA Benefits: Tax advantages of HSA contributions can offset higher deductibles

- Track Medical Expenses: Monitor spending to evaluate if your plan choice is working

- Review Annually: Health and financial situation changes may warrant plan adjustments

- Understand All Costs: Consider premiums, deductibles, copays, and coinsurance together

- Factor in Prescriptions: Calculate annual medication costs under each plan

Deductible Planning Learning Quiz

What is a deductible in health insurance?

The answer is B) The amount you pay out-of-pocket before insurance starts paying. A deductible is the threshold amount you must pay for covered healthcare services before your insurance begins to share the costs. Once you meet your deductible, insurance typically pays a percentage of covered services.

Understanding the difference between premiums, deductibles, copays, and coinsurance is fundamental to health insurance literacy. The deductible specifically represents the initial out-of-pocket expense barrier before insurance coverage begins. This knowledge helps consumers make informed decisions about their coverage needs.

Deductible: Amount paid before insurance coverage begins

Premium: Monthly fee paid for insurance coverage

Copay: Fixed amount paid for specific services

• Deductible must be met before insurance pays

• Higher deductibles typically mean lower premiums

• Deductibles reset annually

• Remember: Deductible = Out-of-pocket before coverage

• Deductibles are per calendar year

• Some services (preventive care) may be exempt

• Confusing deductible with premium

• Forgetting that deductibles reset annually

• Not considering emergency fund for deductible

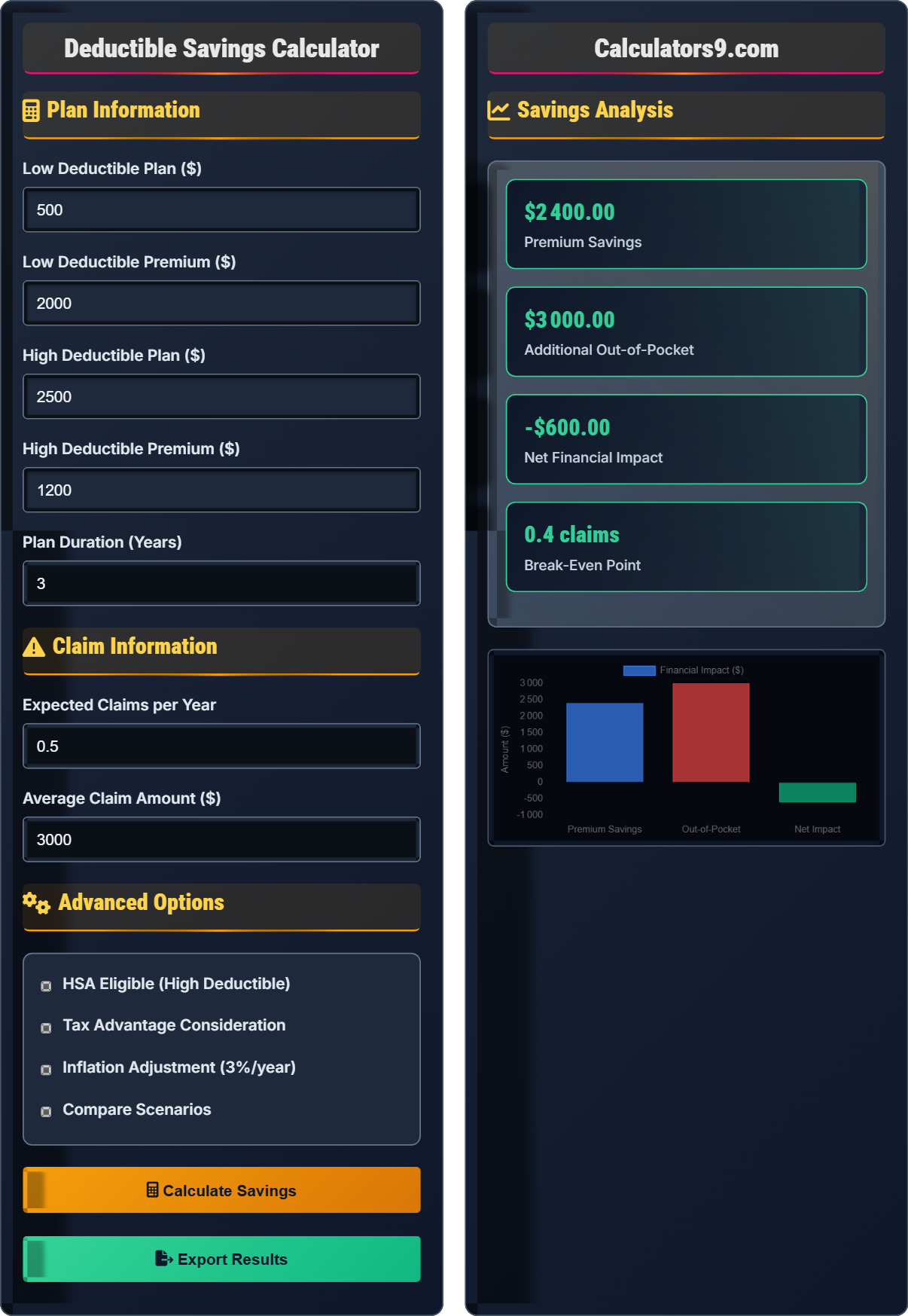

Calculate the break-even point for choosing a high-deductible plan that saves $800 annually in premiums but has a $2,000 higher deductible. Show your work.

Break-even occurs when premium savings equal additional out-of-pocket costs:

Formula: Break-even claims = Premium savings ÷ Additional deductible per claim

Given:

- Annual premium savings = $800

- Additional deductible = $2,000

Step 1: Calculate break-even point

Break-even = $800 ÷ $2,000 = 0.4 claims

Step 2: Interpretation

If you expect 0.4 or fewer claims per year, the high-deductible plan saves money. If you expect more than 0.4 claims per year, the low-deductible plan is more economical.

Since you can't have 0.4 of a claim, this means if you expect any claims at all, the low-deductible plan is better, but if you expect no claims, the high-deductible plan saves $800.

The break-even calculation is a fundamental concept in deductible planning. It quantifies exactly when one plan becomes more economical than another. This mathematical approach removes emotion from the decision-making process and provides a clear threshold for plan selection.

Break-even Point: The threshold where two options have equal costs

Premium Savings: Difference in annual insurance costs

Additional Deductible: Difference in out-of-pocket thresholds

• Break-even = Premium savings ÷ Deductible difference

• If expected claims > break-even, choose lower deductible

• If expected claims < break-even, choose higher deductible

• Calculate break-even for your specific situation

• Consider historical claims when estimating future

• Factor in family health history

• Forgetting to divide by deductible difference

• Not considering frequency of claims

• Ignoring the time value of money

Sarah is choosing between two health plans. Plan A has a $1,000 deductible and $300 monthly premium. Plan B has a $5,000 deductible and $150 monthly premium. Sarah expects to have 2 medical incidents this year, each costing $2,000. Which plan will cost less and by how much?

Step 1: Calculate annual premiums

Plan A: $300 × 12 = $3,600

Plan B: $150 × 12 = $1,800

Premium difference: $3,600 - $1,800 = $1,800

Step 2: Calculate out-of-pocket costs

Plan A: $1,000 (deductible) + ($4,000 - $1,000) = $4,000

Plan B: $5,000 (deductible) + ($4,000 - $5,000) = $5,000 (limited by deductible)

Step 3: Calculate total costs

Plan A: $3,600 + $4,000 = $7,600

Plan B: $1,800 + $5,000 = $6,800

Step 4: Compare

Plan B costs $7,600 - $6,800 = $800 less than Plan A

Conclusion: Plan B is better for Sarah given her expected utilization.

This example demonstrates how actual utilization patterns can change the financial outcome of plan selection. Despite the higher deductible, Plan B was more economical because Sarah's expected claims exceeded the deductible threshold. This shows the importance of matching plan selection to anticipated healthcare needs.

Total Cost: Premiums + Out-of-pocket expenses

Utilization: Actual use of healthcare services

Threshold Effect: When claims exceed deductible limits

• Total cost = Premiums + Out-of-pocket expenses

• Out-of-pocket includes deductible + copays/coinsurance

• You never pay more than the deductible for covered services

• Calculate total costs, not just premiums

• Consider your actual healthcare needs

• Factor in family members' expected usage

• Only comparing premiums, ignoring out-of-pocket costs

• Not considering actual healthcare utilization

• Forgetting that you pay the full deductible amount

Mike chooses a high-deductible plan with a $4,000 deductible and $200 monthly premium. The plan is HSA-eligible, allowing him to contribute $3,650 annually to a tax-free account. If Mike is in the 22% tax bracket, how much does the HSA tax advantage effectively reduce his healthcare costs? If he spends $2,000 from the HSA on medical expenses, what's the net cost?

Step 1: Calculate HSA tax advantage

Tax savings = HSA contribution × Tax rate

Tax savings = $3,650 × 0.22 = $803

Step 2: Calculate effective cost of HSA contribution

Effective cost = Contribution - Tax savings

Effective cost = $3,650 - $803 = $2,847

Step 3: Calculate net cost of $2,000 medical expense

Since HSA funds are tax-free for qualified medical expenses:

Net cost = $2,000 (paid from HSA, no additional tax)

Step 4: Calculate total benefit

The HSA effectively reduces Mike's healthcare costs by $803 due to tax advantages.

Additionally, the $3,650 in the HSA can be used for future medical expenses tax-free, and unused amounts roll over annually.

This demonstrates the triple tax advantage of HSAs: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. This creates a significant financial benefit that can offset the higher deductible costs, especially for those who can consistently contribute to the account.

HSA: Health Savings Account with tax advantages

Triple Tax Advantage: Tax deduction, tax-free growth, tax-free withdrawals

Tax Bracket: Percentage of income paid in taxes

• HSA contributions reduce taxable income

• HSA funds must be used for qualified medical expenses

• Unused HSA funds roll over annually

• Contribute to HSA if eligible for tax benefits

• Use HSA for current expenses or save for future

• Track medical receipts for potential reimbursement

• Not considering HSA tax advantages in plan selection

• Forgetting that HSA funds can be invested

• Misunderstanding qualified medical expenses

What is the recommended emergency fund amount when choosing a high-deductible health plan?

The answer is C) The deductible plus potential copays and coinsurance. When choosing a high-deductible plan, you should have an emergency fund that covers not only the full deductible but also potential copays, coinsurance, and other out-of-pocket expenses that may occur during the year. This ensures you can handle unexpected medical costs without financial strain.

Understanding the total potential out-of-pocket exposure is crucial for financial planning with high-deductible plans. The deductible is just one component of potential costs; copays and coinsurance continue even after meeting the deductible, and there's often an out-of-pocket maximum that represents the worst-case annual cost.

Emergency Fund: Savings set aside for unexpected expenses

Out-of-Pocket Maximum: Highest amount you'll pay annually

Copay: Fixed amount paid for specific services

• Emergency fund should cover full deductible amount

• Include potential copays and coinsurance in planning

• Consider out-of-pocket maximum for worst-case scenario

• Build emergency fund before switching to high-deductible plan

• Consider HSA as part of your emergency fund strategy

• Factor in family members' potential expenses

• Only considering the deductible amount

• Not planning for multiple medical incidents

• Underestimating potential medical costs

Deductible Basics

Amount paid before insurance coverage begins.

\( \text{Break-even} = \frac{\text{Premium Savings}}{\text{Deductible Difference}} \)

Where break-even is the number of claims needed to make higher deductible plan more economical.

- Higher deductible = Lower premium

- Lower deductible = Better protection

- Calculate total costs, not just premiums

Planning Strategies

Save at least the full deductible amount plus potential copays.

- Health status and family history

- Financial situation and emergency fund

- Expected healthcare utilization

- HSA eligibility and tax advantages

- Prescription medication needs

- More than 1 major claim favors lower deductible

- Healthy individuals may benefit from higher deductible

- HSA plans offer significant tax advantages

- Review plan annually based on changing needs

FAQ

Q: How do I decide between a high-deductible and low-deductible plan?

A: The decision depends on your expected healthcare utilization and financial situation:

- Choose Low Deductible if: You expect frequent medical care, have chronic conditions, or prefer predictable costs

- Choose High Deductible if: You're generally healthy, want to minimize monthly premiums, and have an emergency fund

Mathematically, calculate the break-even point: if your annual premium savings exceed your additional out-of-pocket costs, the high-deductible plan wins.

For example, if a high-deductible plan saves $1,200 annually in premiums but has a $2,000 higher deductible, you'll only come out ahead if you have fewer than 0.6 claims that year ($1,200 ÷ $2,000 = 0.6). Since you can't have 0.6 of a claim, this means you'd need zero claims to come out ahead.

Consider the formula: \( \text{Net Impact} = (\text{Premium}_{\text{low}} - \text{Premium}_{\text{high}}) \times \text{Years} - (\text{Deductible}_{\text{high}} - \text{Deductible}_{\text{low}}) \times \text{Claims} \)

Q: Are there tax advantages to high-deductible health plans?

A: Yes! High-deductible health plans (HDHPs) that meet certain criteria are HSA-eligible, offering significant tax advantages:

- Tax-Deductible Contributions: HSA contributions reduce your taxable income

- Tax-Free Growth: Investments in your HSA grow tax-free

- Tax-Free Withdrawals: Funds used for qualified medical expenses are tax-free

For 2026, HSA contribution limits are $3,850 for self-only coverage and $7,750 for family coverage (with catch-up contributions allowed for those 55+).

For example, if you're in the 22% tax bracket and contribute $3,850 to an HSA, you save $847 in federal taxes immediately ($3,850 × 0.22). This tax advantage can significantly offset the higher deductible costs.

Mathematically, the effective cost of your HSA contribution is: \( \text{Effective Cost} = \text{Contribution} \times (1 - \text{Tax Rate}) \)

So $3,850 × (1 - 0.22) = $3,003 effective cost for a $3,850 tax-free medical account.