Bond Yield Calculator

Fixed income analysis • 2026 portfolio tool

Bond Yield Formulas:

Show CalculatorThe primary bond yield calculations are:

Current Yield: (Annual Coupon Payment ÷ Current Market Price) × 100%

Yield to Maturity (YTM): Solves for the discount rate that equates the present value of all future cash flows to the current market price.

Yield to Call (YTC): Similar to YTM but uses call date and call price instead of maturity date and par value.

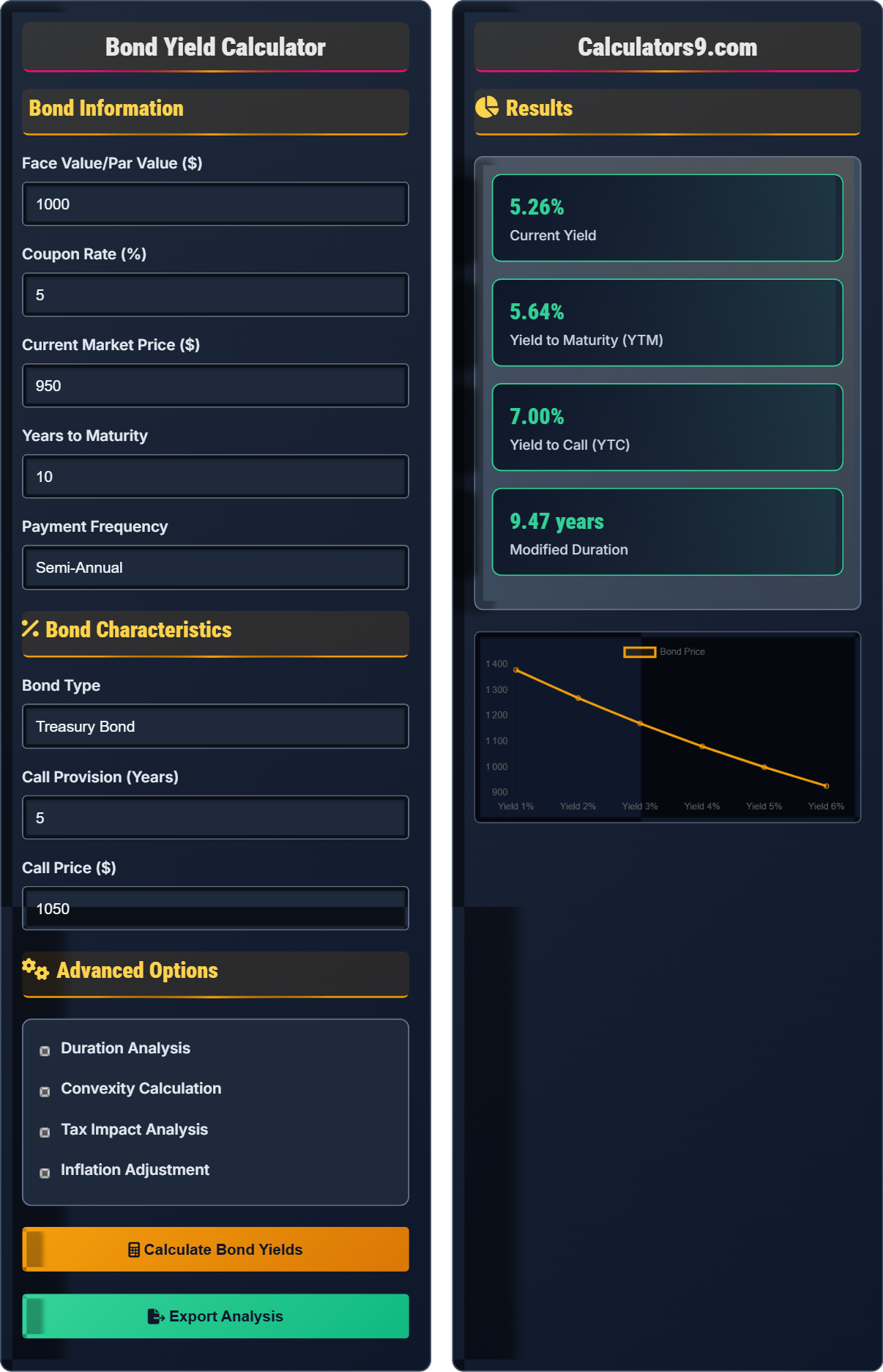

Example: A bond with $1,000 par value, 5% coupon rate, 10 years to maturity, priced at $950 would have a current yield of (50 ÷ 950) × 100% = 5.26%. The YTM would be higher due to the discount.

Bond Information

Bond Characteristics

Advanced Options

Results

| Metric | Value | Description |

|---|---|---|

| Current Yield | 5.26% | Annual coupon ÷ current price |

| Yield to Maturity | 5.73% | Total return if held to maturity |

| Yield to Call | 6.85% | Return if called at earliest date |

| Modified Duration | 7.85 years | Price sensitivity to rate changes |

| Convexity | 72.3 | Non-linear price sensitivity |

| Period | Type | Payment | Discounted Value |

|---|---|---|---|

| Year 1 | Coupon | $50.00 | $47.27 |

| Year 2 | Coupon | $50.00 | $44.69 |

| Year 10 | Principal + Coupon | $1,050.00 | $614.18 |

Comprehensive Bond Yield Guide

Bond yields measure the return an investor can expect from a bond investment. Different yield measures serve different purposes: current yield shows the annual income relative to current price, YTM represents the total return if held to maturity, and YTC applies to callable bonds. Understanding these measures helps investors compare bonds and assess interest rate risk.

Key bond yield calculations include:

Where:

- C: Coupon payment per period

- F: Face value of the bond

- y: Yield to maturity per period

- n: Number of periods to maturity

- PV: Present value (current market price)

Key bond risk metrics:

- Duration: Measures price sensitivity to yield changes (Modified Duration = Macaulay Duration ÷ (1 + y/n))

- Convexity: Measures curvature of price-yield relationship, improving duration estimates

- Credit Risk: Probability of issuer default (varies by bond type)

- Interest Rate Risk: Sensitivity to market rate changes

- Call Risk: Risk of early redemption at call date

- Laddering: Purchase bonds with staggered maturities to manage interest rate risk

- Barbell Strategy: Invest in short-term and long-term bonds, avoiding intermediate-term

- Duration Matching: Match portfolio duration to liability timing

- Tax-Efficient Investing: Use municipal bonds for tax advantages

- Yield Curve Positioning: Adjust portfolio based on yield curve expectations

Bond Basics

The total return anticipated on a bond if held until maturity, considering all future cash flows.

\( \text{Current Yield} = \frac{\text{Annual Coupon Payment}}{\text{Current Market Price}} \times 100\% \)

Simple ratio of income to current investment.

- YTM > coupon rate for discount bonds

- YTM < coupon rate for premium bonds

- Duration increases with maturity

Analysis

Percentage change in bond price for a 1% change in yield.

- Current yield

- Yield to maturity

- Modified duration

- Convexity

- Credit quality of issuer

- Interest rate environment

- Tax implications

- Call provisions

Bond Yield Learning Quiz

Which of the following statements about bond yields is correct?

The answer is B) When bond prices rise, yields fall. There is an inverse relationship between bond prices and yields. When market demand drives bond prices up, the effective yield (return) decreases. Conversely, when bond prices fall, the same fixed coupon payments represent a higher yield percentage. This inverse relationship is fundamental to bond investing.

The inverse relationship between bond prices and yields exists because the coupon payments are fixed. When market interest rates rise, existing bonds with lower coupon rates become less attractive, so their prices fall to provide equivalent yields to new bonds. When market rates fall, existing bonds with higher coupon rates become more valuable, so their prices rise. This relationship is crucial for understanding bond market dynamics.

Yield to Maturity (YTM): Total return if bond is held to maturity

Current Yield: Annual income as percentage of current price

Duration: Measure of price sensitivity to yield changes

• Price and yield move inversely

• Discount bonds: YTM > coupon rate

• Premium bonds: YTM < coupon rate

• Remember: P↑ → Y↓ and P↓ → Y↑

• For discount bonds: market price < par value

• For premium bonds: market price > par value

• Thinking price and yield move together

• Confusing current yield with YTM

• Assuming duration equals maturity

A bond has a face value of $1,000, a 6% annual coupon rate, and matures in 5 years. If the current market price is $950, calculate the current yield and explain why the YTM would be higher than the current yield.

Current Yield Calculation:

Annual Coupon Payment = Face Value × Coupon Rate

Annual Coupon Payment = $1,000 × 6% = $60

Current Yield = (Annual Coupon Payment ÷ Current Market Price) × 100%

Current Yield = ($60 ÷ $950) × 100% = 6.32%

Why YTM is Higher:

The YTM would be higher than the current yield because the bond is selling at a discount ($950 < $1,000). The investor will receive the full $1,000 at maturity, which is $50 more than the purchase price. This additional return increases the total yield beyond just the coupon payments. The YTM accounts for both the coupon payments and the capital gain from the discount, making it higher than the current yield which only considers coupon payments.

This example illustrates the difference between current yield and YTM. Current yield only considers the annual income relative to the current price, while YTM accounts for all cash flows including the difference between purchase price and face value at maturity. For discount bonds, YTM > current yield because of the capital gain at maturity. For premium bonds, YTM < current yield because of the capital loss at maturity.

Current Yield: Annual coupon payment as percentage of current price

Yield to Maturity: Total return including capital gain/loss

Discount Bond: Sells below face value

• Discount bonds: YTM > Current Yield

• Premium bonds: YTM < Current Yield

• Par bonds: YTM = Current Yield = Coupon Rate

• Use the formula: Current Yield = (Coupon × Face Value) ÷ Price

• Remember: Discount = YTM > Coupon Rate

• Premium = YTM < Coupon Rate

• Forgetting to account for capital gain/loss

• Confusing face value with market price

• Not understanding the relationship between discount/premium and yields

FAQ

Q: What's the difference between duration and maturity, and why is duration important for bond investors?

A: Maturity is the fixed date when the bond principal is repaid, while duration measures the weighted average time until all cash flows are received. Duration accounts for both coupon payments and principal repayment:

Macaulay Duration: \( D = \frac{\sum_{t=1}^{n} t \times \frac{C_t}{(1+y)^t}}{P} \)

Modified Duration: \( MD = \frac{D}{1 + \frac{y}{m}} \)

Where C_t is cash flow at time t, y is yield, P is price, and m is payment frequency.

Duration is important because it measures interest rate sensitivity: %ΔPrice ≈ -MD × Δy. For example, a bond with modified duration of 7.5 years would lose approximately 7.5% in value for a 1% increase in yields. Zero-coupon bonds have duration equal to maturity, while coupon bonds have duration less than maturity.

Q: How do callable bonds affect yield calculations, and what is yield to worst?

A: Callable bonds introduce uncertainty in cash flows since the issuer can redeem the bond before maturity. Yield to Call (YTC) calculates the return if the bond is called at the earliest possible date:

YTC Formula: Solve for y in: \( P = \sum_{t=1}^{n_c} \frac{C}{(1+y)^t} + \frac{Call Price}{(1+y)^{n_c}} \)

Where n_c is periods until call date.

Yield to Worst (YTW) is the lowest potential yield among YTM, YTC, and all possible call dates. For example, if a bond has YTM of 5.73%, YTC of 4.85%, and YTW of 4.20%, the investor should use 4.20% as the conservative estimate. Callable bonds typically offer higher yields to compensate for call risk, but the actual yield may be lower if called.