Risk Tolerance Calculator

Investment risk assessment • 2026 portfolio tool

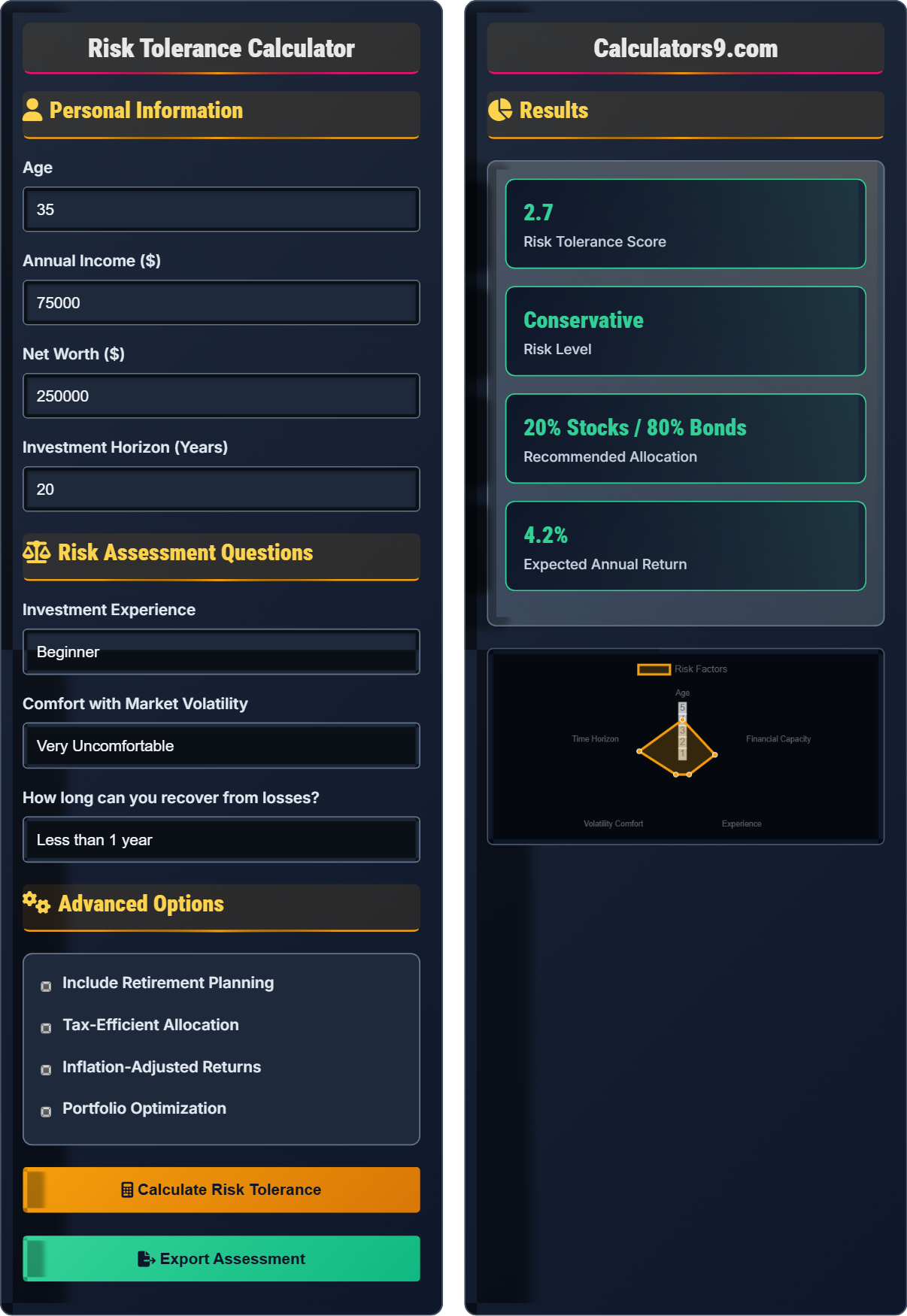

Risk Tolerance Assessment:

Show CalculatorRisk tolerance measures an investor's willingness to accept uncertainty and potential losses in pursuit of higher returns. The assessment considers multiple factors including age, financial situation, investment experience, and psychological comfort with market volatility. The formula combines weighted responses to determine a risk score.

Risk tolerance calculation incorporates:

- Financial Capacity: Ability to withstand losses without affecting lifestyle

- Time Horizon: Investment duration before funds are needed

- Experience: Familiarity with market volatility and investment products

- Psychological Comfort: Emotional response to market fluctuations

Example: An investor with a high risk tolerance might have a portfolio with 80% stocks and 20% bonds, while a conservative investor might have 40% stocks and 60% bonds.

Personal Information

Risk Assessment Questions

Advanced Options

Results

| Factor | Score | Weight | Contribution |

|---|---|---|---|

| Age | 3.0 | 25% | 0.75 |

| Financial Capacity | 4.0 | 20% | 0.80 |

| Investment Experience | 2.0 | 15% | 0.30 |

| Volatility Comfort | 3.5 | 20% | 0.70 |

| Time Horizon | 4.0 | 20% | 0.80 |

| Asset Class | Allocation | Expected Return | Risk Level |

|---|---|---|---|

| Large Cap Stocks | 30% | 7.5% | High |

| International Stocks | 15% | 6.5% | High |

| Bonds | 40% | 3.5% | Low |

| Cash/Alternatives | 15% | 1.5% | Very Low |

Comprehensive Risk Tolerance Guide

Risk tolerance is an investor's ability and willingness to endure market volatility and potential losses in exchange for higher returns. It's influenced by both objective factors (financial capacity, time horizon) and subjective factors (psychological comfort, past experiences). Understanding your risk tolerance is crucial for building an appropriate investment portfolio that you can stick with during market fluctuations.

Risk tolerance is typically calculated using a weighted scoring model:

Where each factor is assigned a score (typically 1-5) and weighted based on its importance. The total score determines the risk level category (Conservative, Moderate, Aggressive).

Based on risk tolerance scores, investors are typically categorized as:

- Conservative (1-3): Focus on capital preservation, 20-40% stocks

- Moderate (4-6): Balanced approach, 40-70% stocks

- Aggressive (7-9): Growth-oriented, 70-90% stocks

- Very Aggressive (10): High growth, 90%+ stocks

- Diversification: Spread investments across different asset classes to reduce risk

- Asset Allocation: Adjust stock/bond mix based on risk tolerance and goals

- Rebalancing: Periodically adjust portfolio to maintain target allocation

- Time Diversification: Gradually shift to more conservative investments as goals approach

- Emergency Fund: Maintain liquid reserves to avoid selling investments during downturns

Risk Assessment

Your willingness to accept uncertainty and potential losses for higher returns.

\( \text{Risk Score} = \sum(\text{Factor Score} \times \text{Weight}) \)

Where factors include age, financial capacity, and investment experience.

- Risk tolerance decreases with age

- Higher income allows more risk

- Longer time horizon supports more risk

Portfolio Allocation

Distribution of investments across different asset classes based on risk tolerance.

- Conservative: 20-40% stocks

- Moderate: 40-70% stocks

- Aggressive: 70-90% stocks

- Rebalancing schedule

- Match allocation to risk tolerance

- Consider tax implications

- Account for inflation

- Review periodically

Risk Tolerance Learning Quiz

Which of the following factors would LEAST likely influence an investor's risk tolerance?

The answer is D) Current market sentiment and news headlines. Risk tolerance is a relatively stable characteristic based on personal financial circumstances, goals, and psychological comfort with volatility. While market conditions might influence tactical decisions, they shouldn't fundamentally change an investor's underlying risk tolerance. Age, financial capacity, and experience are core factors that determine long-term investment approach.

Risk tolerance should be based on stable personal factors rather than volatile external factors. Market sentiment changes rapidly and basing investment decisions on short-term news can lead to emotional investing mistakes. The core factors that determine risk tolerance remain relatively constant over time and should guide long-term investment strategy.

Risk Tolerance: Willingness to accept uncertainty for potential higher returns

Market Sentiment: Collective attitude of investors toward market conditions

Investment Time Horizon: Length of time investments are held

• Risk tolerance is personal and stable

• Based on financial capacity and time horizon

• Should not change based on market news

• Assess risk tolerance based on personal circumstances

• Ignore short-term market noise

• Changing allocation based on market news

• Confusing risk tolerance with market timing

• Letting emotions drive investment decisions

An investor is 35 years old, has $100,000 annual income, $300,000 net worth, 25 years until retirement, intermediate investment experience, and feels somewhat comfortable with market volatility. Calculate their risk tolerance score using the following weights: Age (20%), Financial Capacity (25%), Experience (15%), Comfort (20%), Time Horizon (20%). Assume scores are on a 1-5 scale.

Factor Scoring:

Age (35 years): 4 (young with long time horizon)

Financial Capacity ($100k income, $300k net worth): 4 (solid financial foundation)

Experience (Intermediate): 3 (moderate experience)

Comfort (Somewhat comfortable): 3 (moderate comfort)

Time Horizon (25 years): 4 (long investment period)

Weighted Calculation:

Age: 4 × 20% = 0.8

Financial Capacity: 4 × 25% = 1.0

Experience: 3 × 15% = 0.45

Comfort: 3 × 20% = 0.6

Time Horizon: 4 × 20% = 0.8

Total Risk Score: 0.8 + 1.0 + 0.45 + 0.6 + 0.8 = 3.65

Classification: With a score of 3.65, this investor would be classified as having a Conservative to Moderate risk tolerance, suggesting a portfolio allocation of approximately 40-50% stocks and 50-60% bonds.

This calculation demonstrates how multiple factors contribute to risk tolerance assessment. Each factor is scored individually based on the investor's circumstances, then multiplied by its assigned weight to determine its contribution to the total score. The weighted approach ensures that the most important factors (like financial capacity in this example) have the greatest impact on the final risk classification. This systematic approach removes emotion from the risk assessment process.

Risk Score: Numerical representation of investor's risk tolerance

Weighted Average: Calculation that assigns different importance to factors

Risk Classification: Category based on risk tolerance score

• Multiply factor score by its weight

• Sum all weighted contributions

• Use the formula: Σ(Factor Score × Weight) = Risk Score

• Higher financial capacity allows more risk

• Longer time horizon supports more aggressive allocation

• Forgetting to multiply by weights

• Misclassifying factor scores

• Not considering all relevant factors

FAQ

Q: How often should I reassess my risk tolerance, and what life events might trigger a change?

A: Risk tolerance should typically be reassessed annually or whenever significant life changes occur. Key triggers for reassessment include:

Age-Related Changes: Risk tolerance generally decreases with age as recovery time shortens. The formula for age-based allocation often uses: Percentage in stocks = 110 - Age (or 100 - Age for more conservative approach).

Major Life Events: Marriage, birth of children, job changes, inheritance, or health issues can significantly impact financial capacity and time horizon. For example, with children, you might need more conservative investments for short-term goals (college) while maintaining growth for retirement.

Financial Changes: Significant changes in income, net worth, or emergency fund status affect your ability to absorb losses. If your net worth increases substantially, you might tolerate more risk with a smaller portion of your portfolio.

Regular reassessment ensures your portfolio remains aligned with your current situation and prevents emotional decision-making during market volatility.

Q: How do I differentiate between risk tolerance and risk capacity, and why does this distinction matter?

A: Risk tolerance is your psychological comfort with uncertainty, while risk capacity is your financial ability to withstand losses. The mathematical distinction is:

Risk Capacity: Function of financial resources, time horizon, and necessity for returns

Risk Tolerance: Psychological willingness to accept volatility

For example, a high-income young professional might have high risk capacity (can afford losses, long time horizon) but low risk tolerance (uncomfortable with volatility). Conversely, a wealthy retiree might have high capacity but low tolerance for losses that could deplete retirement funds.

Portfolio Impact: Your actual risk level should be the minimum of tolerance and capacity. If you have high capacity but low tolerance, you'll likely abandon your strategy during market stress. If you have high tolerance but low capacity, a significant loss could severely impact your financial security. The optimal approach balances both factors.