Biweekly Mortgage Calculator

Accelerated payment calculator • 2026 rates

Biweekly Payment Formula:

Show the calculator\( Biweekly\_Payment = \frac{Monthly\_Payment}{2} \)

Where:

- \( Biweekly\_Payment \) = Payment every two weeks

- \( Monthly\_Payment \) = Standard monthly mortgage payment

This formula calculates the biweekly payment amount, which is half of the standard monthly payment. With 26 biweekly payments per year (equivalent to 13 monthly payments), an extra monthly payment is effectively made annually, accelerating mortgage payoff.

Example: For a standard monthly payment of \( \$1{,}500 \), the biweekly payment would be \( \$750 \). Over a year, 26 biweekly payments total \( \$19{,}500 \), equivalent to 13 monthly payments of \( \$1{,}500 \) each, providing one extra payment annually.

This accelerates mortgage payoff by reducing principal faster, resulting in significant interest savings over the loan term.

Loan Details

Advanced Options

Results

| Metric | Monthly Payments | Biweekly Payments | Difference |

|---|

| Payment # | Date | Payment | Principal | Interest | Balance |

|---|

Comprehensive Biweekly Mortgage Guide

A biweekly mortgage involves making payments every two weeks (26 payments per year) instead of monthly (12 payments per year). Since 26 biweekly payments equal 13 monthly payments, you effectively make one extra payment per year. This accelerates principal reduction, saving thousands in interest and shortening the loan term.

The biweekly payment calculation uses the following formula:

Where:

- \(Biweekly\_Payment\) = Payment every two weeks

- \(Monthly\_Payment\) = Standard monthly mortgage payment

Key differences between biweekly and monthly mortgage payments:

- Payment Frequency: 26 payments per year vs 12 payments per year

- Total Annual Payments: 13 monthly payments equivalent vs 12 monthly payments

- Principal Reduction: Faster with biweekly payments

- Total Interest: Lower with biweekly payments

- Set Up Automatic Payments: Ensure consistent biweekly payments without forgetting

- Combine with Extra Payments: Add additional principal payments for maximum acceleration

- Align with Paycheck Schedule: Match payments to biweekly income for easier budgeting

- Refinance to Take Advantage: Switch to biweekly after refinancing to a better rate

- Use Windfalls: Apply bonuses or tax refunds to further accelerate payoff

Biweekly Basics

Pay every 2 weeks instead of monthly, getting 13 payments per year.

\(Biweekly\_Payment = \frac{Monthly\_Payment}{2}\)

Where Biweekly_Payment=payment every 2 weeks, Monthly_Payment=standard monthly payment.

- 26 biweekly payments = 13 monthly payments

- One extra payment per year

- Faster principal reduction

Strategies

Extra payment each year accelerates mortgage payoff.

- Set up automatic payments

- Combine with extra payments

- Align with paycheck schedule

- Use windfalls strategically

- Verify lender accepts biweekly payments

- Some lenders charge setup fees

- Manual calculations may be needed

- Impact on budgeting

Biweekly Mortgage Learning Quiz

How many biweekly payments equal one monthly payment?

The answer is B) 2. A biweekly payment is half of a monthly payment. Therefore, 2 biweekly payments equal 1 monthly payment. Since there are 26 biweekly payments per year (every 2 weeks), this equals 13 monthly payments, providing one extra payment annually.

This is the fundamental principle behind biweekly mortgage payments. Each biweekly payment is exactly half of the standard monthly payment. When you make 26 payments per year instead of 12, you're essentially making 13 monthly payments annually (26 ÷ 2 = 13), which means one extra payment each year.

Biweekly Payment: Payment made every two weeks (26 times per year)

Monthly Payment: Standard mortgage payment made 12 times per year

Extra Payment: Additional payment made annually due to biweekly schedule

• 26 biweekly payments = 13 monthly payments

• Each biweekly payment = Monthly payment ÷ 2

• One extra payment per year accelerates payoff

• Remember: 2 biweekly payments = 1 monthly payment

• 26 biweekly payments = 13 monthly payments

• One extra payment annually accelerates mortgage

• Thinking biweekly payments are the same as monthly

• Not understanding the extra payment effect

• Confusing the frequency with the amount

Calculate the biweekly payment for a standard monthly payment of $1,600. Show your work.

Using the biweekly payment formula: \(Biweekly\_Payment = \frac{Monthly\_Payment}{2}\)

Given:

- Monthly Payment = $1,600

Step 1: Calculate biweekly payment = $1,600 ÷ 2 = $800

Therefore, the biweekly payment would be $800.

The biweekly payment calculation is straightforward - it's simply half of the monthly payment. This makes budgeting easier since each biweekly payment is exactly half of what you would normally pay monthly. The real benefit comes from making 26 payments per year instead of 12, which effectively provides one extra payment annually.

Biweekly Payment: Half of the monthly payment amount

Payment Frequency: How often payments are made

Annual Equivalent: Total payments made in one year

• Biweekly payment = Monthly payment ÷ 2

• 26 biweekly payments per year

• Equals 13 monthly payments annually

• Remember: Biweekly = Monthly ÷ 2

• 26 biweekly payments = 13 monthly payments

• One extra payment accelerates mortgage payoff

• Calculating biweekly as monthly ÷ 4 instead of ÷ 2

• Forgetting the extra payment effect

• Confusing payment amount with frequency

Compare the total annual payments for a $1,400 monthly mortgage: Option A is standard monthly payments, Option B is biweekly payments. What is the difference in annual payments?

Step 1: Calculate total annual payments for monthly option

Monthly payments: 12 × $1,400 = $16,800

Step 2: Calculate biweekly payment amount

Biweekly payment: $1,400 ÷ 2 = $700

Step 3: Calculate total annual payments for biweekly option

Biweekly payments: 26 × $700 = $18,200

Step 4: Calculate difference

Difference: $18,200 - $16,800 = $1,400

Therefore, the biweekly option results in $1,400 more in annual payments, equivalent to one extra monthly payment.

This demonstrates the core mechanism of biweekly payments. While each individual payment is smaller (half of monthly), the increased frequency results in an extra payment annually. This extra payment goes directly toward principal reduction, accelerating the mortgage payoff and saving significant interest over the loan term.

Extra Payment: Additional payment made annually due to biweekly schedule

Principal Reduction: Decrease in loan balanceInterest Savings: Money saved by paying down principal faster

• 26 biweekly payments = 13 monthly payments

• One extra payment annually accelerates payoff

• More frequent payments reduce interest charges

• Remember: 26 biweekly = 13 monthly payments

• Extra payment goes to principal reduction

• Faster principal reduction saves interest

• Not recognizing the extra payment effect

• Thinking biweekly is just splitting monthly payment

• Forgetting the annual payment difference

A borrower has a $250,000 mortgage at 4.5% for 30 years with a monthly payment of $1,267. If they switch to biweekly payments of $633.50, how much interest could they save and how much time would they save on the mortgage? (Hint: The extra payment each year accelerates principal reduction)

Step 1: Calculate total interest for standard monthly payments

Total payments: 360 × $1,267 = $456,120

Total interest: $456,120 - $250,000 = $206,120

Step 2: For biweekly payments, the effective result is making 13 monthly payments per year

This accelerates principal reduction significantly

Step 3: With biweekly payments, the mortgage would be paid off in approximately 25 years instead of 30

Step 4: Calculate approximate total interest with biweekly payments

Total payments: 300 × $1,267 = $380,100 (equivalent)

Total interest: $380,100 - $250,000 = $130,100

Step 5: Calculate savings

Interest savings: $206,120 - $130,100 = $76,020

Time saved: 30 - 25 = 5 years

Therefore, biweekly payments could save approximately $76,020 in interest and 5 years.

This demonstrates the powerful effect of accelerated principal reduction. The extra payment each year (equivalent to one monthly payment) goes entirely to principal, which immediately reduces the interest calculated on the remaining balance. This creates a compounding effect where each subsequent payment has more impact on principal reduction, leading to substantial interest savings and time reduction.

Principal Reduction: Decrease in loan balance that reduces future interest

Compounding Effect: Where early principal reduction amplifies future savings

Time Acceleration: Shorter loan term due to faster principal reduction

• Extra payment goes directly to principal

• Reduced principal = less interest charged

• Earlier principal reduction has greater impact

• The extra payment each year is key to acceleration

• Earlier principal reduction saves more interest

• The effect compounds over time

• Not understanding the compounding effect of principal reduction

• Thinking savings are just the extra payment amount

• Underestimating the time reduction benefit

Which of the following borrowers would LEAST benefit from a biweekly mortgage payment plan?

The answer is B) Someone planning to sell in 3-5 years. Biweekly payments provide maximum benefit to borrowers who plan to keep their mortgage for a long period, as the interest savings accumulate over time. For someone planning to sell in 3-5 years, the benefits of biweekly payments would be minimal since most of the interest savings occur in the later years of the loan when more of each payment goes toward principal.

Biweekly payment benefits are front-loaded in terms of principal reduction but back-loaded in terms of total interest savings. In the early years of a mortgage, more of each payment goes to interest than principal. The biweekly payment strategy is most beneficial for long-term homeowners who will stay in their homes for 10+ years, allowing them to realize the full benefit of accelerated principal reduction and interest savings.

Front-Loaded Interest: More interest paid in early years of mortgage

Back-Loaded Savings: Interest savings accumulate over time

Long-Term Benefit: Maximum advantage for extended ownership

• Biweekly benefits increase with time

• More beneficial for long-term ownership

• Minimal benefit for short-term ownership

• Consider planned ownership period

• Biweekly is better for long-term homeowners

• Evaluate total benefit vs. time horizon

• Assuming biweekly benefits apply equally regardless of time frame

• Not considering ownership timeline

• Thinking all borrowers benefit equally

FAQ

Q: How much can I really save with biweekly payments?

A: The savings from biweekly payments depend on your loan amount, interest rate, and remaining term. Generally, you can expect to save:

- Time: 4-8 years off a 30-year mortgage

- Interest: $20,000-$100,000+ on a typical mortgage

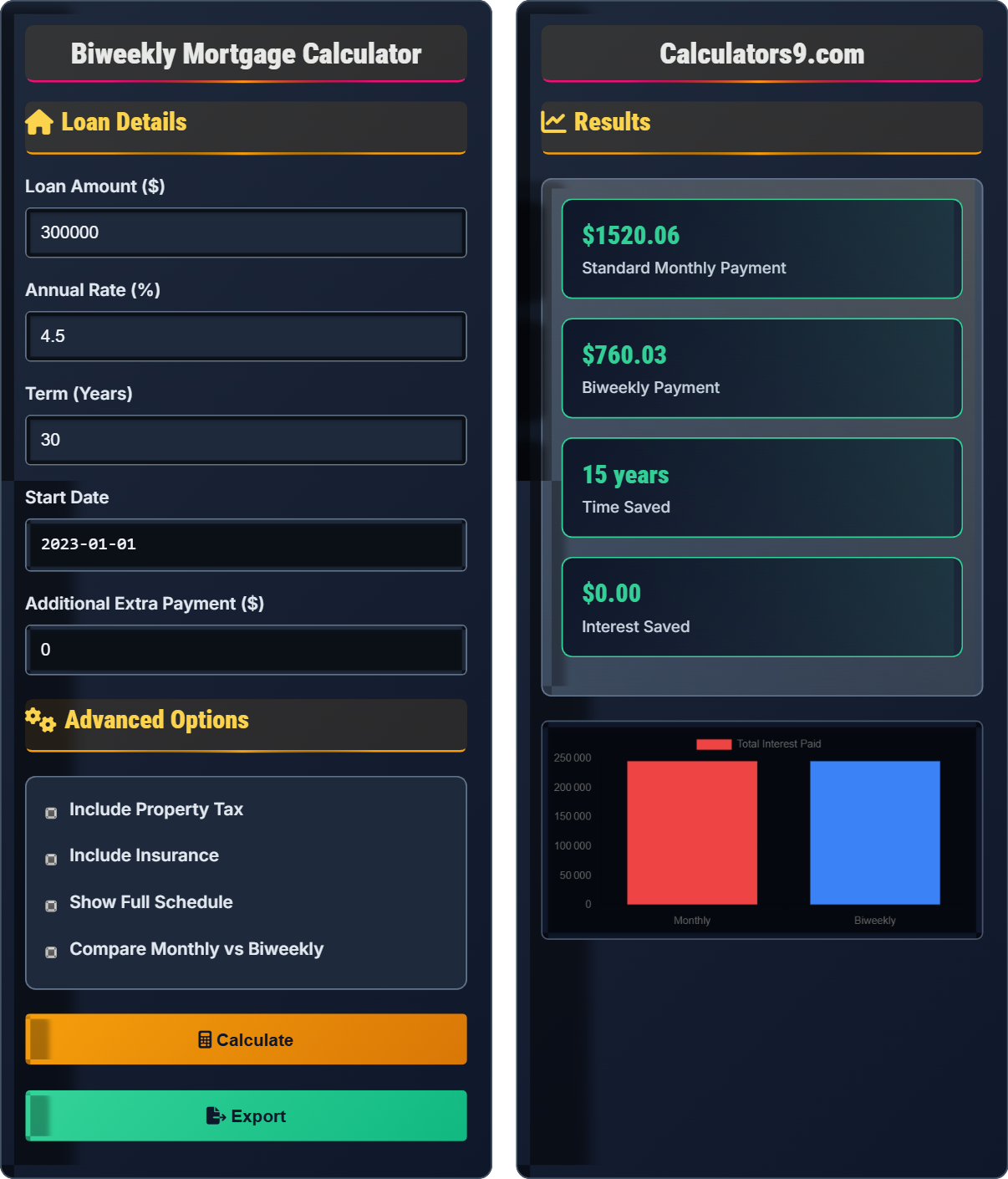

For example, on a loan of \( Principal = \$300{,}000 \) at 4.5%, the standard 30-year payment is approximately \( \$1{,}520 \). With biweekly payments of \( \$760 \), you make 26 payments per year (equivalent to 13 monthly payments), saving about \( \$67{,}000 \) in interest and paying off the loan about 4 years early.

The key is that the extra payment each year (13th monthly payment) goes directly to principal, accelerating payoff significantly.

Q: Do I need to sign up with a special biweekly payment service?

A: No, you don't need a special service. You can achieve the same benefits by:

- Manually: Making an extra payment each year

- Automatically: Setting up biweekly payments directly with your lender

- Alternative: Making 13 monthly payments per year instead of 12

Many lenders offer biweekly payment options directly, but some charge setup fees. If your lender doesn't support biweekly payments, you can manually make an extra payment each year (equal to one monthly payment) to achieve the same effect without fees.