Interest-Only Mortgage Calculator

IO payment calculator • 2026 rates

Interest-Only Payment Formula:

Show the calculator\( IO\_Payment = Principal \times \frac{Annual\_Rate}{12} \)

Where:

- \( IO\_Payment \) = Monthly interest-only payment

- \( Principal \) = Outstanding loan balance

- \( Annual\_Rate \) = Annual interest rate (as decimal)

This formula calculates the monthly payment during the interest-only period, which covers only the interest on the loan principal.

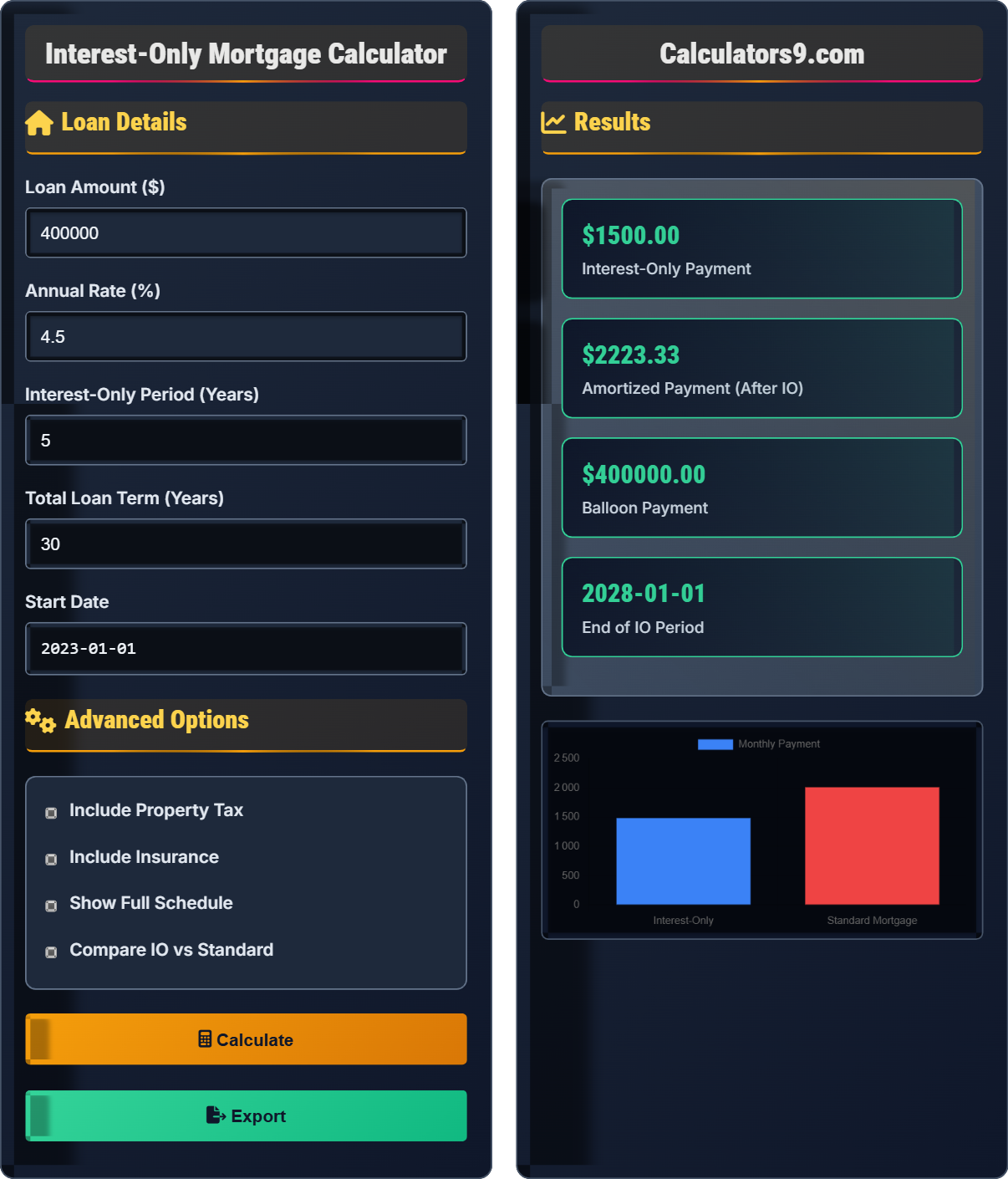

Example: For a loan of \( Principal = \$400{,}000 \) at an annual interest rate of 4.5%:

Monthly interest rate: \( \frac{4.5\%}{12} = 0.375\% = 0.00375 \)

Monthly payment:

\( IO\_Payment = 400{,}000 \times 0.00375 = \$1{,}500 \)

Thus, the borrower would pay $1,500 per month during the interest-only period.

Loan Details

Advanced Options

Results

| Metric | Interest-Only | Standard Mortgage | Difference |

|---|

| Year | Payment Type | Payment | Principal | Interest | Balance |

|---|

Comprehensive Interest-Only Mortgage Guide

An interest-only mortgage allows borrowers to pay only the interest on the loan for a specified period (typically 5-10 years). During this interest-only (IO) period, the monthly payment is lower because it doesn't include principal repayment. After the IO period ends, payments increase significantly as they include both principal and interest to pay off the loan over the remaining term.

The interest-only payment calculation uses the following formula:

Where:

- \(IO\_Payment\) = Monthly interest-only payment

- \(Principal\) = Outstanding loan balance

- \(Annual\_Rate\) = Annual interest rate (as decimal)

Key differences between interest-only and standard mortgages:

- Initial Payments: IO payments are lower during the IO period

- Principal Repayment: IO doesn't reduce principal during IO period

- Payment Shock: IO payments increase significantly after IO period ends

- Total Interest: IO typically results in higher total interest paid

- Income Fluctuation: Beneficial for those with variable income (bonuses, commissions)

- Short-Term Ownership: Good for those planning to sell before IO period ends

- Cash Flow Management: Frees up cash for investments or other expenses

- Refinance Before End: Refinance to a standard mortgage before payment shock

- Investment Property: Useful for rental properties with expected appreciation

IO Mortgage Basics

Pay only interest for a set period, then principal plus interest.

\(IO\_Payment = Principal \times \frac{Annual\_Rate}{12}\)

Where IO_Payment=monthly payment, Principal=loan balance, Annual_Rate=interest rate.

- Principal remains unchanged during IO period

- Payments increase after IO period ends

- Total interest is typically higher than standard mortgage

Strategies

Sudden increase in payments after IO period ends.

- Plan for payment increase

- Build reserves for higher payments

- Consider refinancing before end

- Plan to sell before end

- No equity buildup during IO

- Payment shock after IO period

- Higher total interest cost

- Requires careful planning

Interest-Only Mortgage Learning Quiz

During the interest-only period of an IO mortgage, what happens to the principal balance?

The answer is B) It remains unchanged. During the interest-only period, the monthly payment covers only the interest charges, so the principal balance stays the same. No principal is repaid during this time, which is why the payment is lower than a standard amortizing mortgage.

This is the fundamental characteristic of interest-only mortgages. Unlike standard amortizing mortgages where each payment reduces the principal, IO payments only cover the interest cost. This means the borrower is essentially renting the money for the IO period, paying only the cost of borrowing without reducing the amount owed.

Interest-Only Period: Time when only interest is paid, principal remains unchanged

Principal Balance: Amount still owed on the loan

Payment Shock: Significant increase in payments after IO period ends

• IO payments cover only interest charges

• Principal balance remains constant during IO period

• Payments increase after IO period ends

• Remember: IO = Interest Only, no principal reduction

• Plan for payment increase after IO period

• Consider refinancing before payment shock

• Thinking IO payments reduce principal

• Not preparing for payment increase after IO period

• Assuming IO mortgages build equity during IO period

Calculate the monthly interest-only payment for a $350,000 loan at 4.25% annual interest. Show your work.

Using the IO payment formula: \(IO\_Payment = Principal \times \frac{Annual\_Rate}{12}\)

Given:

- Principal = $350,000

- Annual Rate = 4.25% = 0.0425

Step 1: Calculate monthly interest rate = 0.0425 ÷ 12 = 0.003542

Step 2: Calculate IO payment = $350,000 × 0.003542 = $1,239.58

Therefore, the monthly interest-only payment would be $1,239.58.

This calculation shows how the IO payment is simply the annual interest rate applied monthly to the principal balance. Since only interest is paid, the calculation is straightforward: divide the annual rate by 12 to get the monthly rate, then multiply by the principal.

Monthly Interest Rate: Annual rate divided by 12

Interest Charge: Cost of borrowing money for the month

Principal Balance: Outstanding loan amount

• IO payment = Principal × (Annual Rate ÷ 12)

• Principal balance remains unchanged during IO

• Payment is only for interest charges

• Remember: IO payment = Principal × Monthly Rate

• Monthly rate = Annual Rate ÷ 12

• No principal reduction during IO period

• Including principal in IO payment calculation

• Forgetting to convert annual rate to monthly

• Assuming IO payments reduce principal

Compare the initial monthly payments for a $500,000 loan: Option A is a 30-year standard mortgage at 4.5%, Option B is a 5-year interest-only mortgage at 4.5% followed by a 25-year amortizing mortgage. What is the difference in initial payments?

Step 1: Calculate standard mortgage payment

Monthly rate = 4.5% ÷ 12 = 0.375% = 0.00375

Number of payments = 30 × 12 = 360

Standard payment = $500,000 × [0.00375(1.00375)^360] / [(1.00375)^360 - 1] = $2,533.43

Step 2: Calculate IO payment

IO payment = $500,000 × 0.00375 = $1,875.00

Step 3: Calculate difference

Difference = $2,533.43 - $1,875.00 = $658.43

Therefore, the IO payment is $658.43 lower than the standard payment initially.

This example illustrates the primary advantage of IO mortgages: lower initial payments. However, borrowers must be prepared for the significant payment increase after the IO period ends, when the full amortizing payment begins. The savings during the IO period can be substantial, but the future payment shock must be carefully planned for.

Payment Shock: Sudden increase in payments after IO period ends

Amortizing Payment: Payment that includes both principal and interest

Initial Savings: Lower payments during IO period

• IO payments are lower during IO period

• Payment increases significantly after IO period

• Total interest is typically higher with IO

• Calculate both initial and post-IO payments

• Plan for payment increase after IO period

• Consider refinancing before payment shock

• Only considering initial payment savings

• Not planning for payment increase after IO period

• Forgetting about total interest costs

A borrower takes a $400,000 IO mortgage with a 5-year interest-only period followed by a 25-year amortizing period at 4.25% annual interest. What is the balloon payment due at the end of the IO period, and what would the new monthly payment be?

Step 1: Calculate balloon payment

Since no principal is repaid during the IO period, the entire principal remains due.

Balloon payment = $400,000

Step 2: Calculate new monthly payment after IO period

Remaining term = 25 years = 300 months

Monthly rate = 4.25% ÷ 12 = 0.3542% = 0.003542

New payment = $400,000 × [0.003542(1.003542)^300] / [(1.003542)^300 - 1] = $2,129.28

Therefore, the balloon payment is $400,000 and the new monthly payment would be $2,129.28.

This demonstrates the "payment shock" characteristic of IO mortgages. After the IO period, the borrower faces the full amortizing payment on the remaining principal. In this case, the payment jumps from the IO payment of $1,417 to the amortizing payment of $2,129 - a significant increase. This is why IO mortgages require careful financial planning.

Balloon Payment: Large payment due at the end of a loan term

Payment Shock: Significant increase in payments after IO period

Principal Balance: Amount still owed on the loan

• Principal balance remains unchanged during IO period

• Full principal is due after IO period

• Payment increases significantly after IO period

• Plan for payment increase after IO period

• Consider refinancing before end of IO

• Understand the full payment obligation

• Forgetting that principal remains unchanged during IO

• Not preparing for payment increase after IO period

• Assuming IO reduces the loan balance

Which of the following borrowers would MOST benefit from an interest-only mortgage?

The answer is C) Someone planning to sell before IO period ends. Interest-only mortgages are ideal for borrowers who plan to sell their property before the IO period ends, as they benefit from lower payments without facing the payment shock. They avoid the principal repayment issue since they'll sell before the payment increase occurs.

IO mortgages work best for short-term ownership scenarios. Borrowers who plan to stay long-term face the challenge of payment shock after the IO period ends. Those who sell before the IO period expires benefit from lower payments without experiencing the increased payments or the lack of equity buildup that occurs during the IO period.

Payment Shock: Significant increase in payments after IO period

Short-Term Ownership: Planning to sell before IO period ends

Equity Building: Principal reduction that builds ownership

• IO mortgages work best for short-term ownership

• Payment shock occurs after IO period ends

• No equity buildup during IO period

• Consider your planned ownership timeline

• Plan for payment increase if keeping long-term

• IO is best for short-term ownership plans

• Using IO for long-term ownership without planning

• Not considering payment shock after IO period

• Expecting equity buildup during IO period

FAQ

Q: What happens when the interest-only period ends?

A: When the interest-only period ends, the loan converts to a fully amortizing loan. This means your monthly payment will increase significantly as it now includes both principal and interest payments to pay off the remaining balance over the remaining loan term.

For example, with a loan of \( Principal = \$400{,}000 \) at 4.5%, the interest-only payment would be \( \$400{,}000 \times 0.00375 = \$1{,}500 \). After the IO period ends, if 25 years remain, the payment would jump to approximately \( \$2{,}220 \) per month to pay off the full principal balance over the remaining term.

This dramatic increase is called "payment shock" and is why IO loans require careful financial planning.

Q: Are interest-only mortgages risky?

A: Yes, interest-only mortgages carry specific risks:

- Payment Shock: Payments increase significantly after the IO period ends

- No Equity Building: Principal balance remains unchanged during IO period

- Higher Total Interest: More interest paid over the life of the loan

- Refinancing Risk: Need to refinance before payment shock or qualify for higher payments

However, IO mortgages can be beneficial for borrowers with variable income or those planning to sell before the IO period ends. They require careful financial planning and discipline to manage successfully.