Loan Amortization Calculator

Detailed payment schedule • 2026 rates

Loan Amortization Formula:

Show the calculator\( M = P \frac{r(1+r)^n}{(1+r)^n - 1} \)

Where:

- \( M \) = monthly payment

- \( P \) = loan principal (total loan amount)

- \( r \) = monthly interest rate (annual rate divided by 12, in decimal form)

- \( n \) = total number of monthly payments (loan term in years × 12)

This formula calculates the fixed monthly payment required to fully pay off a loan over the loan term, taking into account compound interest.

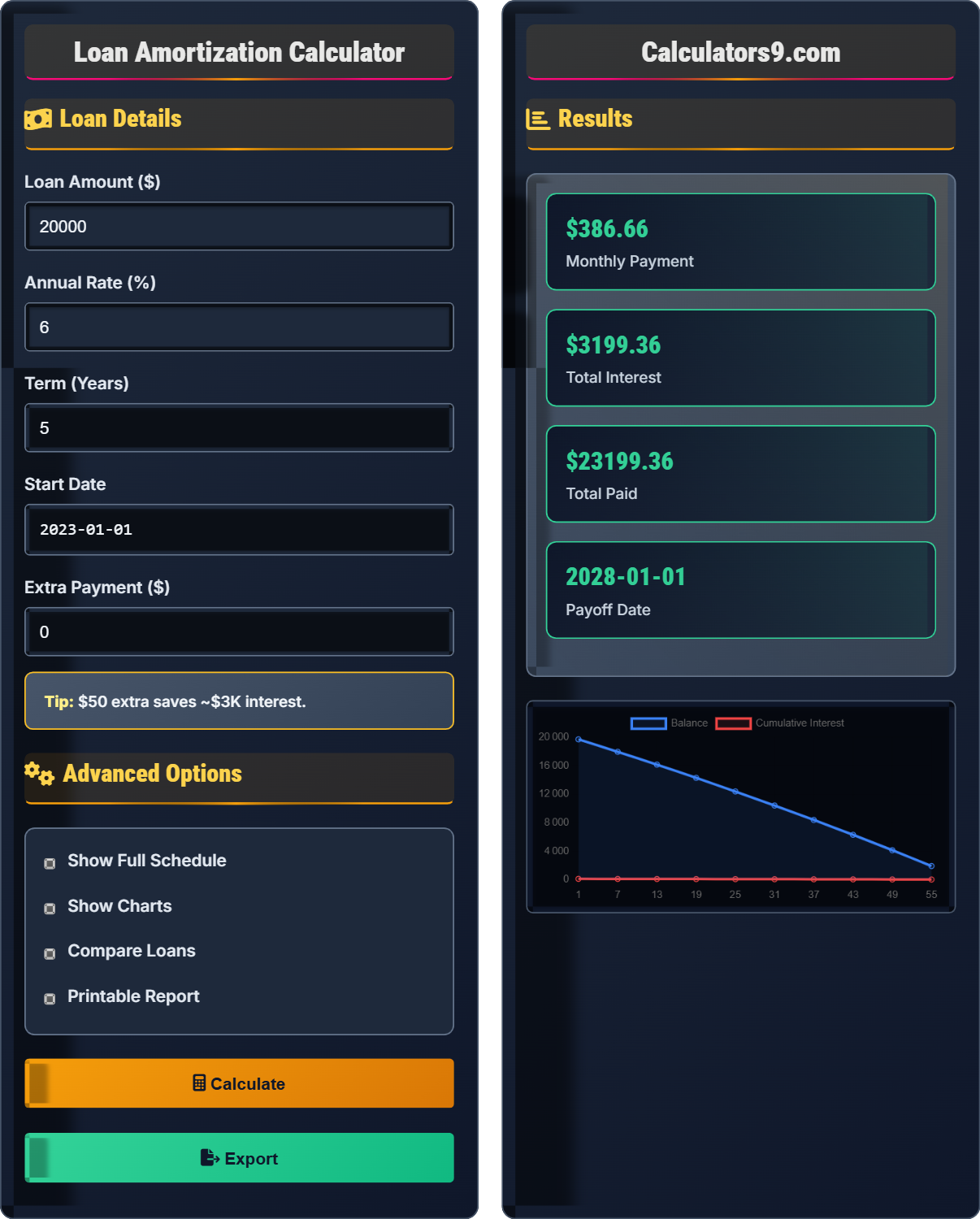

Example: For a loan of \( P = \$20{,}000 \) at an annual interest rate of 6% over 5 years:

Monthly interest rate: \( r = \frac{6\%}{12} = 0.005 \)

Total payments: \( n = 5 \times 12 = 60 \)

Monthly payment:

\( M = 20{,}000 \times \frac{0.005(1+0.005)^{60}}{(1+0.005)^{60} - 1} \approx \$387 \)

Thus, the borrower would pay approximately $387 per month for 5 years.

Loan Details

Advanced Options

Results

| Payment # | Date | Payment | Principal | Interest | Balance |

|---|

| Category | Amount | Percentage |

|---|

Comprehensive Loan Amortization Guide

Loan amortization is the process of paying off a debt over time through regular payments. Each payment consists of both principal and interest components. Initially, most of the payment goes toward interest, but as the loan matures, more of the payment goes toward reducing the principal. An amortization schedule shows exactly how much of each payment goes to principal and interest over the life of the loan.

The standard loan payment calculation uses the following formula:

Where:

- \(M\) = Monthly payment

- \(P\) = Principal loan amount

- \(r\) = Monthly interest rate (annual rate divided by 12)

- \(n\) = Total number of payments (loan term in years multiplied by 12)

Your monthly loan payment typically includes two main components:

- Principal: Portion that reduces the outstanding loan balance

- Interest: Cost of borrowing money, paid to the lender

- Make extra payments: Reduces principal faster, saving interest over the loan term

- Refinance: If rates drop significantly, refinancing can reduce your monthly payment

- Round up payments: Round your monthly payment up to the nearest hundred dollars

- Bi-weekly payments: Pay half your monthly payment every two weeks, resulting in one extra payment per year

- Pay off high-interest loans first: Use the avalanche method to minimize total interest

Loan Basics

Process of paying off debt with regular payments over time.

\(M = P\frac{r(1+r)^n}{(1+r)^n-1}\)

Where M=monthly payment, P=loan amount, r=monthly rate, n=payments.

- Interest calculated on remaining balance

- Early payments save more interest

- Small rate changes = big savings

Strategies

Early payments are mostly interest, later payments are mostly principal.

- Round up payments

- Extra annual payment

- Bi-weekly payments

- Apply windfalls

- Prepayment penalties

- Opportunity cost

- Credit score impact

- Tax implications

Loan Amortization Learning Quiz

What happens to the principal and interest portions of a loan payment over time?

The answer is C) Interest portion decreases, principal increases. In the early years of a loan, most of the payment goes toward interest because the outstanding balance is highest. As the loan progresses, the principal balance decreases, so less interest is charged, allowing more of each payment to go toward principal reduction.

This is a fundamental concept in loan amortization. Interest is always calculated on the remaining principal balance. At the beginning of the loan, the principal is at its maximum, so interest charges are highest. As you pay down the principal, the interest calculation is based on a smaller balance, meaning more of each payment can go toward reducing the principal.

Amortization: The process of paying off a loan with regular payments

Principal: The original loan amount being repaid

Interest: The cost of borrowing money

• Interest is calculated on remaining principal balance

• Early payments are mostly interest

• Later payments are mostly principal

• Look at your amortization schedule to see the principal/interest split

• Extra payments early in the loan term save more interest

• The 50/50 point occurs when equal amounts go to principal and interest

• Thinking all payments are equally split between principal and interest

• Believing that early payments don't reduce principal

• Not understanding that interest is recalculated each period

Calculate the monthly payment for a $15,000 loan at 5% annual interest over 4 years. Show your work.

Using the loan formula: \(M = P\frac{r(1+r)^n}{(1+r)^n-1}\)

Given:

- P = $15,000

- r = 0.05 ÷ 12 = 0.004167

- n = 4 × 12 = 48

Step 1: Calculate (1+r)^n = (1.004167)^48 = 1.2209

Step 2: Calculate numerator: r(1+r)^n = 0.004167 × 1.2209 = 0.005088

Step 3: Calculate denominator: (1+r)^n - 1 = 1.2209 - 1 = 0.2209

Step 4: Calculate M = P × (numerator/denominator) = $15,000 × (0.005088/0.2209) = $15,000 × 0.02303 = $345.47

This calculation shows how the amortization formula works for different loan types. Notice how the monthly payment is relatively small compared to the total loan amount, but over the 4-year term, the total interest paid will still be significant. The calculation involves converting the annual rate to a monthly rate and the term to months.

Compound Interest: Interest calculated on both the principal and previously accumulated interest

Monthly Rate: Annual interest rate divided by 12

Number of Payments: Loan term in years multiplied by 12

• Always convert annual interest rates to monthly rates for calculations

• Convert loan terms to months for accurate calculations

• The amortization formula accounts for compound interest over time

• Remember: r = annual rate ÷ 12

• Remember: n = loan years × 12

• Use a calculator for complex exponent calculations

• Forgetting to convert annual rates to monthly rates

• Using the wrong number of payments (not converting years to months)

• Making calculation errors with large exponents

Mike takes out a 5-year auto loan for $25,000 at an interest rate of 4.5%. His monthly payment is $466. What is the total interest he will pay over the life of the loan?

Step 1: Calculate total number of payments = 5 years × 12 months/year = 60 payments

Step 2: Calculate total amount paid = $466 × 60 = $27,960

Step 3: Calculate total interest = Total paid - Principal = $27,960 - $25,000 = $2,960

Therefore, Mike will pay $2,960 in interest over the life of his loan.

This example shows how interest adds up over time. For a $25,000 loan, Mike will pay nearly $3,000 in interest over 5 years. This demonstrates why paying off a loan early can save substantial amounts of money. The calculation shows the relationship between monthly payments, loan term, and total interest.

Total Interest: The sum of all interest payments over the life of the loan

Loan Term: The length of time to repay the loan

Principal: The original loan amount

• Total interest = (Monthly payment × Number of payments) - Principal

• Longer loan terms result in more total interest paid

• Even with fixed payments, most early payments go toward interest

• Remember: Total paid = Monthly payment × Total number of payments

• Total interest is always Total paid minus Principal

• Use this calculation to compare different loan scenarios

• Forgetting to multiply monthly payment by total number of payments

• Subtracting the wrong amounts when calculating interest

• Confusing monthly interest with total interest over the loan term

Sarah has a 5-year auto loan for $20,000 at 6% interest. Her regular monthly payment is $387. She decides to pay an extra $25 each month toward principal. How much will this save her in interest over the life of the loan? (Hint: Calculate how many months early she'll pay off the loan and estimate interest savings)

Step 1: Regular scenario - Total payments over 60 months = $387 × 60 = $23,220

Step 2: With extra payments - Each month, Sarah pays $387 + $25 = $412

Step 3: With extra payments, the loan will be paid off earlier due to reduced principal

Step 4: Using amortization calculations, the loan would be paid off approximately 6 months earlier (around 54 months)

Step 5: Total paid with extra payments ≈ $387 × 54 = $20,898

Step 6: Interest savings = $23,220 - $20,898 = $2,322

Therefore, Sarah saves approximately $2,322 in interest by paying an extra $25 monthly.

This demonstrates the power of paying extra toward principal. Since interest is calculated on the remaining principal balance, reducing the principal early significantly reduces the total interest paid. The extra $25 per month doesn't just reduce the final payment - it reduces interest charges on all future payments. This is why even small extra payments can result in substantial savings over time.

Principal Reduction: Paying extra toward the loan balance to decrease interest charges

Amortization: The process of gradually paying off a debt through regular payments

Interest Savings: The difference between total interest paid with and without extra payments

• Extra payments go directly to principal reduction

• Principal reduction decreases future interest charges

• Small extra payments can result in significant long-term savings

• Round up your monthly payment to the next hundred dollars

• Make an extra payment once a year (equivalent to bi-weekly payments)

• Use tax refunds or bonuses for extra principal payments

• Thinking extra payments only affect the final payment

• Not realizing that extra payments reduce interest on all future payments

• Confusing interest-only savings with principal reduction benefits

Which of the following statements about loan terms is TRUE?

The answer is B) Longer terms result in higher total interest. While longer loan terms may have lower monthly payments, they result in more interest being paid over the life of the loan because interest accrues over a longer period. For example, a $20,000 loan at 6% would pay approximately $3,220 in interest over 5 years but $6,670 over 10 years.

While longer loan terms provide lower monthly payments, they come at the cost of significantly higher total interest. This is because interest continues to accrue over the extended term. The trade-off is between affordability (lower monthly payments) and long-term cost (higher total interest). Understanding this relationship helps borrowers make informed decisions based on their financial situation.

Loan Term: The length of time to repay the loan

Interest Rate Risk: The risk that interest rates will change during the loan term

Payment Affordability: The ability to make regular monthly payments

• Longer loan terms generally result in more total interest

• Shorter terms result in higher monthly payments but lower total interest

• The longer the loan term, the more interest accumulates

• Compare total interest costs between different loan terms

• Consider your monthly budget when choosing a term

• If you can afford higher payments, shorter terms save interest

• Focusing only on monthly payments and ignoring total interest costs

• Assuming longer terms always have higher interest rates

• Not considering how the term affects total interest paid

FAQ

Q: Why do early loan payments consist mostly of interest?

A: Interest is calculated based on the remaining principal balance. At the beginning of the loan, the principal balance is at its maximum (the full loan amount), so the interest charge is highest. As you make payments and reduce the principal, the interest calculation is based on a smaller balance, allowing more of each payment to go toward principal reduction.

For example, in a loan of \( P = \$20{,}000 \) at 6% annual interest (0.5% monthly), the first month's interest would be \( 20{,}000 \times 0.005 = \$100 \). If the monthly payment is \( \$387 \), then \( \$287 \) goes to principal. But in the last month, with only say \( \$385 \) left, the interest would be \( \$385 \times 0.005 = \$1.93 \), with almost the entire payment going to principal.

Q: Should I choose a shorter loan term or make extra payments on a longer term?

A: The best choice depends on your financial situation and discipline.

Shorter term: Lower total interest, higher monthly payments, forced discipline

Longer term with extra payments: Lower required payments for flexibility, potential for same interest savings if you're disciplined

Mathematically, both approaches can yield similar results if you're consistent with extra payments. However, shorter terms eliminate the temptation to spend extra money elsewhere and protect against interest rate changes if it's a variable rate loan.