Family Budget Planner

Manage your finances • 2026 edition

50/30/20 Budget Rule:

Show the calculator\( \text{Income} = \text{Needs} (50\%) + \text{Wants} (30\%) + \text{Savings} (20\%) \)

Where:

- \( \text{Income} \) = Total monthly gross income

- \( \text{Needs} (50\%) \) = Essential expenses (housing, food, utilities)

- \( \text{Wants} (30\%) \) = Discretionary expenses (entertainment, dining)

- \( \text{Savings} (20\%) \) = Savings and debt repayment

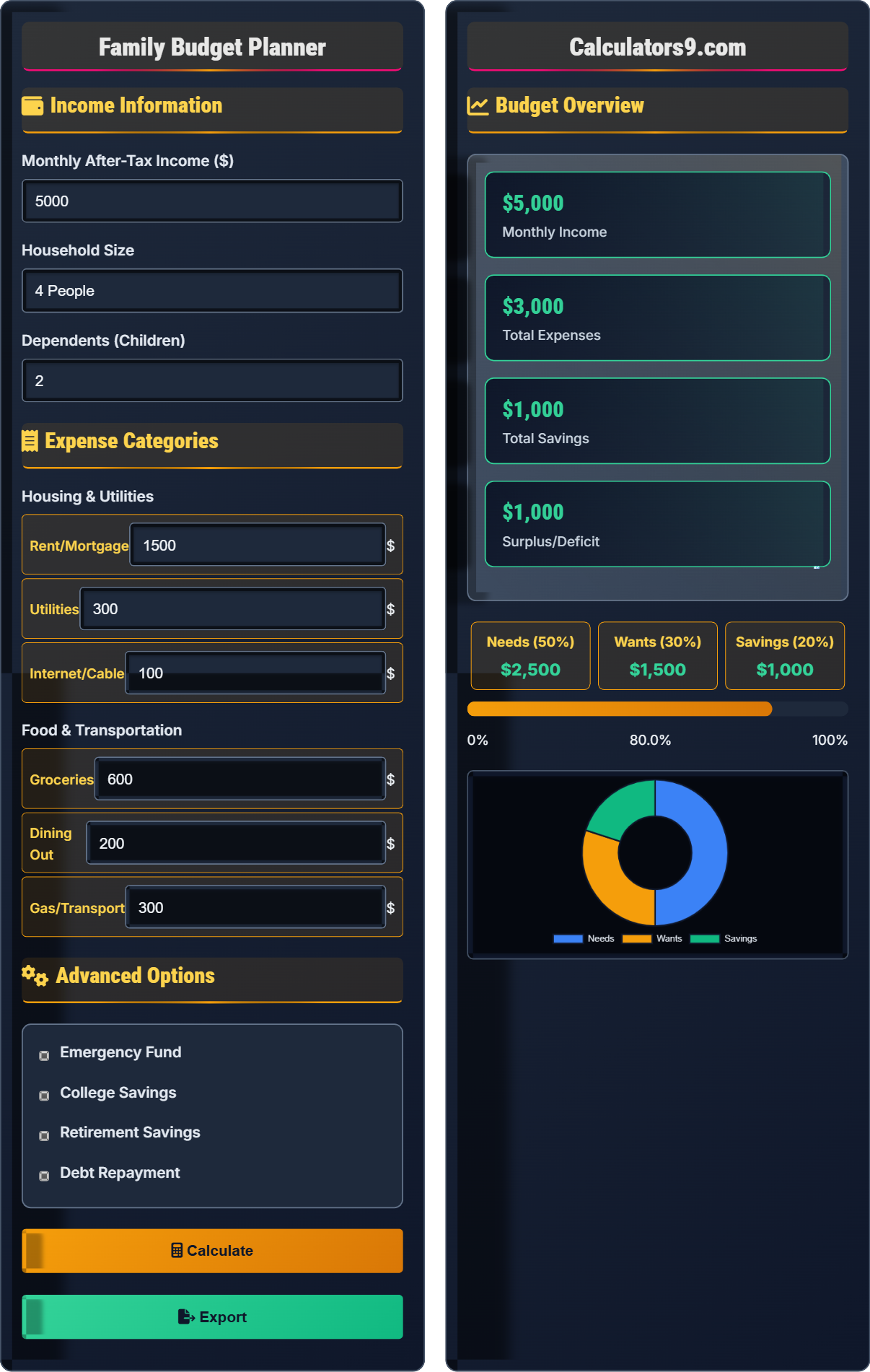

This formula provides a simple framework for allocating after-tax income across essential expenses, discretionary spending, and savings. The 50/30/20 rule helps families maintain financial stability while saving for the future.

Example: For a family with $5,000 monthly after-tax income:

Needs (50%): $5,000 × 0.50 = $2,500

Wants (30%): $5,000 × 0.30 = $1,500

Savings (20%): $5,000 × 0.20 = $1,000

This allocation ensures 20% is saved while maintaining balance between necessities and wants.

Income Information

Expense Categories

Advanced Options

Budget Overview

| Category | Budget | Spent | Remaining |

|---|

| Goal | Amount | Timeline | Progress |

|---|

Savings Recommendations

Family Budget Planning Guide

Family budgeting involves tracking income and expenses to ensure financial stability and growth. A successful family budget considers all household members' needs while planning for both short-term expenses and long-term financial goals like college education and retirement.

Experts recommend dividing after-tax income as follows:

Where:

- \(I\) = Total monthly after-tax income

- \(N\) = Needs (essential expenses)

- \(W\) = Wants (discretionary expenses)

- \(S\) = Savings and debt repayment

After covering essentials, allocate remaining funds wisely:

- Entertainment: Movies, hobbies, subscriptions

- Dining Out: Restaurants and takeout

- Travel: Vacations and trips

- Shopping: Clothing, electronics, gifts

- Track spending: Use apps or spreadsheets to monitor expenses

- Set priorities: Focus on needs before wants

- Automate savings: Set up automatic transfers

- Review monthly: Adjust budget based on actual spending

- Plan for seasons: Account for holiday expenses

Budgeting Basics

Plan for household income and expenses.

\(I = N(50\%) + W(30\%) + S(20\%)\)

Where I=income, N=needs, W=wants, S=savings.

- Track all income sources

- Categorize all expenses

- Save consistently

Planning Strategies

3-6 months of essential expenses.

- Pay yourself first

- Automate transfers

- Start small if needed

- Build gradually

- Adjust for family size

- Account for seasonal expenses

- Plan for unexpected costs

- Review regularly

Family Budget Planning Learning Quiz

According to the 50/30/20 budget rule, what percentage of after-tax income should go toward savings and debt repayment?

The answer is B) 20%. According to the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings and debt repayment. This framework ensures that families prioritize their financial security while maintaining flexibility for discretionary spending.

The 50/30/20 rule provides a simple yet effective framework for budget allocation. The 20% savings portion is crucial for financial security, including emergency funds, retirement contributions, and debt reduction. This percentage helps families build wealth and protect against financial emergencies.

50/30/20 Rule: Income allocation framework

Needs: Essential living expenses

Wants: Discretionary spending

• 50% for essential expenses

• 30% for discretionary spending

• 20% for savings and debt

• Adjust percentages based on situation

• Prioritize high-interest debt

• Automate savings transfers

• Not saving enough for emergencies

• Confusing wants with needs

• Skipping the savings portion

If a family has $4,500 in monthly after-tax income, how much should they allocate to needs according to the 50/30/20 rule?

Using the 50/30/20 rule:

Needs allocation = $4,500 × 0.50 = $2,250

Wants allocation = $4,500 × 0.30 = $1,350

Savings allocation = $4,500 × 0.20 = $900

Therefore, $2,250 should go toward needs.

This calculation demonstrates how to apply the 50/30/20 rule to a specific income amount. The needs category includes essential expenses like housing, utilities, food, transportation, and minimum debt payments. Understanding this calculation helps families plan their budgets accurately.

After-Tax Income: Income after deductions

Essential Expenses: Necessary for survival

Needs Category: Housing, food, utilities

• Calculate based on after-tax income

• Include all essential expenses

• Review regularly for accuracy

• Use budgeting apps for tracking

• Round allocations for simplicity

• Adjust for unique situations

• Including pre-tax income

• Not accounting for all expenses

• Being too rigid with percentages

The Johnson family has monthly essential expenses totaling $3,200. They want to build an emergency fund covering 6 months of expenses. If they can save $400 per month, how many months will it take to reach their emergency fund goal?

Step 1: Calculate emergency fund goal

Emergency fund = Monthly expenses × 6 months

Emergency fund = $3,200 × 6 = $19,200

Step 2: Calculate months to reach goal

Months needed = Emergency fund ÷ Monthly savings

Months needed = $19,200 ÷ $400 = 48 months

Step 3: Convert to years

48 months ÷ 12 = 4 years

The Johnson family will need 48 months (4 years) to build their emergency fund.

This problem demonstrates how to calculate an appropriate emergency fund size and the time needed to reach it. Emergency funds provide financial security during unexpected events like job loss or medical emergencies. The 3-6 month guideline balances preparedness with opportunity cost of having funds in low-yield accounts.

Emergency Fund: Savings for unexpected expenses

Essential Expenses: Necessary monthly costs

Financial Security: Protection against emergencies

• Emergency fund covers 3-6 months

• Include only essential expenses

• Keep in accessible account

• Start with $1,000 minimum

• Build gradually

• Replenish after use

• Not accounting for all essential expenses

• Keeping emergency fund in risky investments

• Using for non-emergency expenses

Sarah's family has $5,000 monthly income and follows the 50/30/20 rule. Their actual expenses are: $2,800 needs, $1,200 wants, and $500 savings. Are they following the 50/30/20 rule? If not, how should they adjust their budget?

Step 1: Calculate 50/30/20 allocations

Needs (50%): $5,000 × 0.50 = $2,500

Wants (30%): $5,000 × 0.30 = $1,500

Savings (20%): $5,000 × 0.20 = $1,000

Step 2: Compare actual vs. recommended

Actual needs: $2,800 (recommended: $2,500) → $300 over

Actual wants: $1,200 (recommended: $1,500) → $300 under

Actual savings: $500 (recommended: $1,000) → $500 under

Step 3: Adjustment recommendation

Reduce needs by $300 and redirect to savings: $500 + $300 = $800 savings

Still $200 short of recommended $1,000 savings goal.

Sarah's family is overspending on needs and undersaving.

This demonstrates how to evaluate actual spending against budget guidelines. The family is spending too much on needs (possibly housing or transportation) and not saving enough. To improve, they should look for ways to reduce essential expenses and increase savings, perhaps by refinancing loans or finding more affordable housing.

Budget Analysis: Comparing actual to planned

Expense Optimization: Reducing unnecessary costs

Financial Alignment: Matching spending to goals

• Track actual spending

• Compare to budget goals

• Adjust as needed

• Review monthly spending

• Look for expense reductions

• Prioritize savings goals

• Not tracking actual spending

• Confusing wants with needs

• Skipping savings for wants

How should a family budget change when they have young children compared to when they're childless?

The answer is B) Increase needs allocation for childcare. When a family has young children, expenses for childcare, diapers, formula, clothing, and other necessities increase significantly. These are essential expenses that fall under the "needs" category. While the 50/30/20 rule provides a guideline, families may need to adjust these percentages based on their specific situation, potentially allocating more than 50% to needs when caring for young children.

Family budgets must adapt to changing needs throughout different life stages. With children, the "needs" category expands to include childcare, education expenses, clothing, and other necessities. The key is maintaining the focus on essential expenses while still trying to preserve some savings, even if the percentages shift from the ideal 50/30/20.

Life Stage Budgeting: Adjusting for family changes

Childcare Costs: Essential expenses for working parents

Budget Flexibility: Adapting to circumstances

• Adjust for family size changes

• Prioritize essential expenses

• Maintain some savings if possible

• Plan for increased childcare costs

• Consider flexible budget percentages

• Look for family discounts

• Not accounting for child-related expenses

• Eliminating savings completely

• Treating all child expenses as wants

FAQ

Q: How do I budget when my income varies each month?

A: For variable income, calculate your average monthly income over the past 12 months and budget based on that. Use the 50/30/20 rule:

\( \text{Avg Income} = \frac{\sum_{i=1}^{12} \text{Monthly Income}_i}{12} \)

During high-income months, save the excess to cover lower-income months. For example, if your average is $4,500 but one month you earn $6,000, put the extra $1,500 toward savings. During a low month of $3,000, use $1,500 from your buffer to maintain your budget allocations.

Q: What if I can't save 20% of my income with children?

A: The 50/30/20 rule is a guideline, not a strict requirement. With children, your needs category may expand beyond 50%. If you can only save 5-10% initially, that's better than nothing. Start with an emergency fund of $1,000, then gradually increase savings as your budget allows.

Even small amounts can grow over time. For example, saving $100/month at 7% annual return for 20 years yields:

\( FV = 100 \times \frac{(1.00583)^{240} - 1}{0.00583} \approx \$52,000 \)

Focus on building the habit of saving consistently, even if the amount is small.