Property Tax Estimator

Real estate tax calculator • 2026 rates

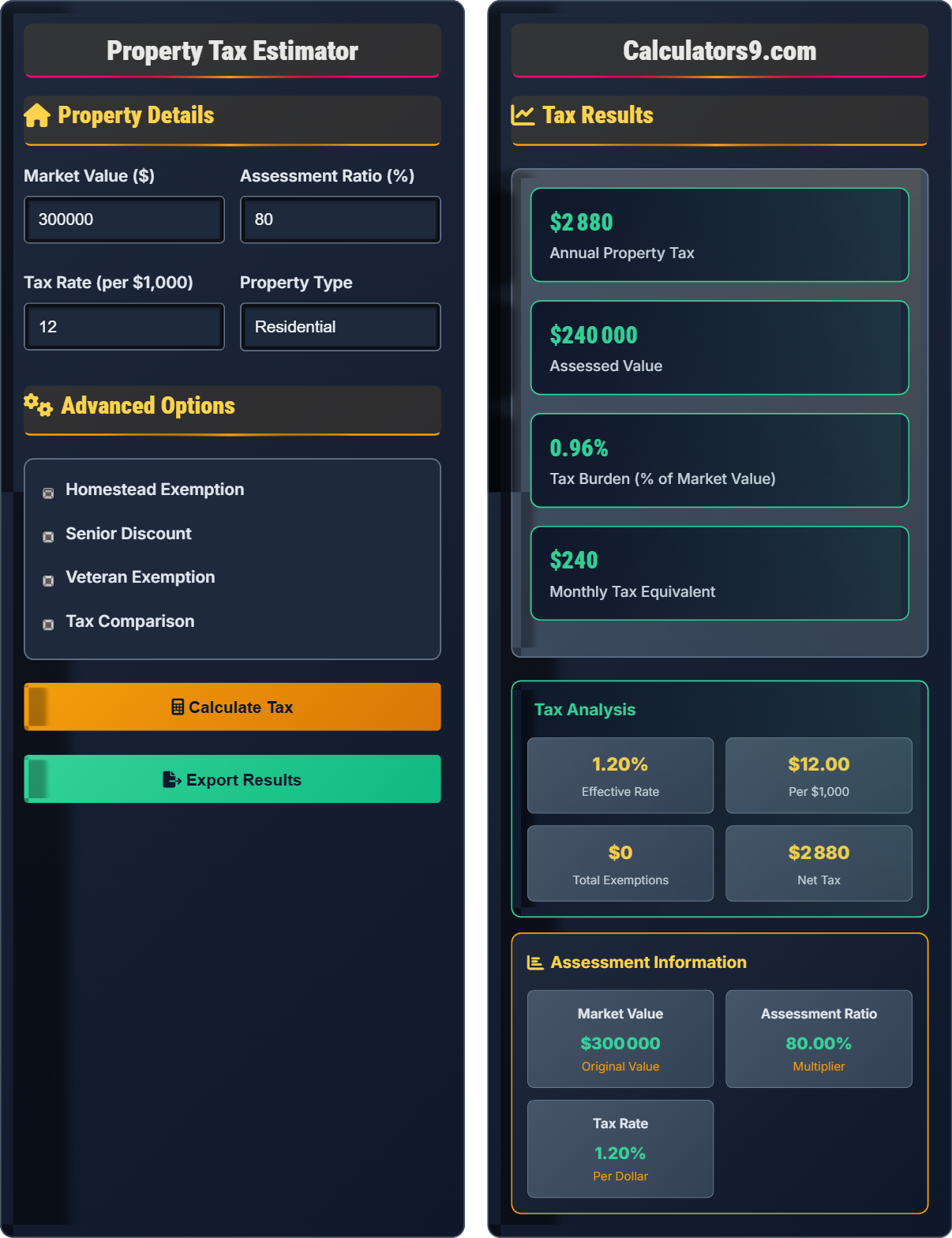

Property Tax Formula:

Show the calculator\( PT = AV \times TR \)

Where:

- \( PT \) = Property Tax

- \( AV \) = Assessed Value (market value × assessment ratio)

- \( TR \) = Tax Rate (expressed as decimal)

This formula calculates the annual property tax based on the assessed value of a property and the local tax rate. The assessed value is typically a percentage of the market value determined by local assessors.

Example: For a home with a market value of \( MV = \$300{,}000 \), an assessment ratio of 80%, and a tax rate of 1.2%:

Assessment Ratio = 80% = 0.80

Tax Rate = 1.2% = 0.012

Assessed Value = \( 300{,}000 \times 0.80 = \$240{,}000 \)

Property Tax = \( 240{,}000 \times 0.012 = \$2{,}880 \)

Thus, the annual property tax would be approximately $2,880.

Property Details

Advanced Options

Tax Results

Property Tax Analysis Guide

Property tax is a tax levied on real estate by local governments to fund public services such as schools, roads, emergency services, and infrastructure. The tax is typically calculated based on the assessed value of the property and the local tax rate. Property taxes are one of the largest ongoing costs of homeownership, second only to mortgage payments.

The standard property tax calculation uses the following formula:

Where:

- \(PT\) = Property Tax

- \(AV\) = Assessed Value (Market Value × Assessment Ratio)

- \(TR\) = Tax Rate (expressed as decimal)

Many jurisdictions offer tax exemptions that can significantly reduce property tax bills:

- Homestead Exemption: Reduces taxable value for primary residences

- School Tax Relief: Discounts for elderly or disabled residents

- Veteran Exemptions: Special considerations for military veterans

- Disability Exemptions: Reduced rates for permanently disabled individuals

- Senior Citizen Discounts: Age-based tax reductions

- Appeal Assessment: Challenge unfair assessments through formal appeals

- Take Advantage of Exemptions: Apply for all eligible exemptions

- Property Improvements: Time improvements to minimize assessment impact

- Consider Location: Research tax rates when buying property

- Budget Planning: Set aside monthly funds for tax payments

Tax Calculation Basics

Property tax is a recurring tax based on the assessed value of real estate property, collected by local governments.

\(PT = AV \times TR\)

Where PT=property tax, AV=assessed value, TR=tax rate.

- Tax rates vary by jurisdiction

- Assessments occur regularly

- Exemptions can reduce tax burden

Tax Planning

Process to challenge property assessment if believed to be too high.

- Review assessment notice

- Gather comparable sales data

- File appeal within deadline

- Present case to review board

- Appeals deadlines are strict

- Requires documentation

- May need professional help

- Success not guaranteed

Property Tax Learning Quiz

A homeowner has a property with a market value of $400,000. The local assessment ratio is 75%, and the tax rate is $15 per $1,000 of assessed value. The owner qualifies for a homestead exemption of $25,000 and a senior discount of 10%. Calculate the annual property tax, showing all steps and explaining how each exemption affects the final tax bill.

Step 1: Calculate Assessed Value

Assessed Value = Market Value × Assessment Ratio

Assessed Value = $400,000 × 0.75 = $300,000

Step 2: Apply Homestead Exemption

Reduced Assessed Value = $300,000 - $25,000 = $275,000

Step 3: Calculate Base Tax

Tax Rate = $15 per $1,000 = 0.015

Base Tax = $275,000 × 0.015 = $4,125

Step 4: Apply Senior Discount

Discount Amount = $4,125 × 0.10 = $412.50

Final Tax = $4,125 - $412.50 = $3,712.50

The annual property tax is $3,712.50. The homestead exemption reduced the tax by $375 ($25,000 × 0.015), and the senior discount provided an additional $412.50 in savings.

Property tax calculations involve multiple steps and various exemptions that can significantly impact the final tax bill. The homestead exemption reduces the assessed value before tax calculation, providing a dollar-for-dollar reduction in taxes. The senior discount applies to the calculated tax amount, offering percentage-based savings on the base tax. Understanding these different types of exemptions helps taxpayers plan for their tax obligations and take advantage of available savings.

Assessment Ratio: Percentage of market value used for taxation purposes

Homestead Exemption: Reduction in taxable value for primary residence

Senior Discount: Percentage reduction in tax bill for qualifying seniors

• Exemptions must be applied for separately

• Different exemptions may not stack

• Deadlines for applications are strict

• File exemption applications early to avoid missing deadlines

• Keep documentation of property value changes

• Research all available exemptions in your area

• Forgetting to apply for exemptions

• Misunderstanding assessment ratios

• Not accounting for tax rate changes

A family is considering buying a home in two different cities. City A has a market value of $350,000, an assessment ratio of 85%, and a tax rate of $14 per $1,000. City B has a market value of $320,000, an assessment ratio of 100%, and a tax rate of $12 per $1,000. Calculate the annual property tax for each city and determine which has the higher tax burden. Also calculate the tax burden as a percentage of market value for each city.

City A Calculation:

Assessed Value = $350,000 × 0.85 = $297,500

Tax Rate = $14 per $1,000 = 0.014

Annual Tax = $297,500 × 0.014 = $4,165

Tax Burden = ($4,165 ÷ $350,000) × 100 = 1.19%

City B Calculation:

Assessed Value = $320,000 × 1.00 = $320,000

Tax Rate = $12 per $1,000 = 0.012

Annual Tax = $320,000 × 0.012 = $3,840

Tax Burden = ($3,840 ÷ $320,000) × 100 = 1.20%

City A has a higher annual tax ($4,165 vs $3,840), but City B has a slightly higher tax burden as a percentage of market value (1.20% vs 1.19%). This demonstrates that absolute tax amounts and tax burden percentages can tell different stories about the relative cost of property ownership.

This problem illustrates the importance of understanding both absolute tax amounts and relative tax burdens when comparing property tax costs. While City A has a higher dollar amount in taxes, City B has a higher percentage burden. The tax burden percentage (tax as % of market value) is particularly useful for comparing tax costs across different property values. This metric normalizes the tax cost relative to the property value, allowing for fair comparisons regardless of price point.

Tax Burden: Property tax expressed as a percentage of market value

Assessment Ratio: Percentage of market value subject to taxation

Tax Rate: Amount of tax per unit of assessed value

• Compare both absolute and relative tax costs

• Consider assessment ratios in comparisons

• Tax rates may vary by property type

• Calculate tax burden percentage for meaningful comparisons

• Research assessment appeal processes in target areas

• Factor in other local taxes and fees

• Only comparing absolute tax amounts

• Forgetting to apply assessment ratios

• Misconverting tax rates from per $1,000 format

FAQ

Q: How often are property assessments conducted, and can I contest my assessment if I believe it's too high?

A: Property assessments are typically conducted on a regular cycle, which varies by jurisdiction but is commonly every 1-6 years. Some areas reassess annually, while others may go 3-5 years between assessments. The frequency depends on local laws and the resources available to the assessor's office.

Yes, you can contest your assessment if you believe it's too high. The process typically involves:

- Reviewing your assessment notice for accuracy of property details

- Gathering comparable sales data of similar properties in your area

- Filing an appeal within the specified deadline (usually 30-60 days)

- Presenting your case to the local assessment review board

- Providing evidence such as recent appraisals or sales of comparable properties

Success in appealing an assessment depends on the strength of your evidence and whether the assessment was indeed incorrect. Professional appraisals can strengthen your case, though they come with additional costs. Many jurisdictions allow for informal appeals before requiring a formal hearing, which can resolve issues more quickly.

Q: What's the difference between property tax and property tax assessment, and how do they relate to my mortgage payments?

A: Property tax assessment is the process by which local assessors determine the value of your property for taxation purposes. This assessment results in an assessed value that is typically a percentage of the market value. Property tax is the actual amount you owe based on this assessed value multiplied by the local tax rate.

The relationship to your mortgage payments is significant. Most mortgage lenders require borrowers to pay property taxes through an escrow account. The lender collects 1/12 of your annual property tax with each monthly mortgage payment and holds these funds in escrow. When the tax bill comes due, the lender pays it on your behalf.

For example, if your annual property tax is $3,600, your lender would collect $300 per month as part of your mortgage payment to cover the taxes. This ensures that taxes are paid on time and protects the lender's interest in the property. If your property tax assessment increases significantly, your monthly mortgage payment may also increase to accommodate the higher tax obligation.

Some homeowners opt to pay property taxes directly rather than through escrow, but this requires meeting certain criteria set by the lender and demonstrating financial responsibility to ensure timely payment of these important obligations.