Healthcare Cost in Retirement Calculator

Future security planning • 2026 edition

Healthcare Cost Formulas:

- Medicare Part B Premium: $170.10/month (2023)

- Medicare Part D Premium: $30-50/month

- Medicare Supplement: $100-500/month

- Annual Healthcare Cost: Part B + Part D + Supplements + Out-of-pocket

- Retirement Healthcare Total: Annual Cost × Years in Retirement

For example: $300/month × 12 months × 20 years = $72,000 total healthcare cost in retirement. Plus long-term care costs could bring total to $250,000+.

Healthcare Information

Advanced Options

Healthcare Cost Projection

| Category | Monthly Cost | Annual Cost | Notes |

|---|

| Planning Element | Amount | Timeline | Recommendation |

|---|

Healthcare Cost Planning

Healthcare costs are often the largest expense in retirement, frequently exceeding housing and food costs. Understanding the various components and planning ahead can significantly impact your financial security in retirement.

Key components of retirement healthcare costs:

- Medicare Parts A & B: Basic coverage (Part A is usually premium-free)

- Medicare Part D: Prescription drug coverage

- Medigap/Medicare Supplement: Fill gaps in Original Medicare

- Out-of-pocket costs: Deductibles, copays, and coinsurance

- Long-term care: Nursing home, assisted living, or in-home care

According to Fidelity research, the average 65-year-old couple retiring in 2023 will need approximately $315,000 to cover healthcare expenses in retirement. This includes:

- Medicare premiums: $150,000 over 20 years

- Out-of-pocket costs: $100,000 over 20 years

- Long-term care: $65,000 average

- HSA Contributions: Triple tax advantage for medical expenses

- Medigap Planning: Choose appropriate coverage level

- Prescription Programs: Utilize manufacturer discounts and generics

- Preventive Care: Reduce future costs through prevention

- Healthcare Advocacy: Negotiate costs and seek second opinions

Healthcare Cost Learning Quiz

Which part of Medicare covers prescription drugs?

The answer is D) Medicare Part D. Medicare Part D is the prescription drug coverage program that helps pay for prescription medications. Part A covers hospital stays, Part B covers doctor visits and outpatient services, and Part C (Medicare Advantage) is an alternative to Original Medicare that includes Parts A, B, and often D.

This question tests basic Medicare knowledge, which is crucial for retirement planning. Understanding the different parts of Medicare helps individuals plan for their specific healthcare needs and associated costs. Part D is particularly important because prescription drug costs can be substantial in retirement and are not covered by Original Medicare (Parts A and B).

Medicare Part A: Hospital insurance

Medicare Part B: Medical insurance for doctor visits

Medicare Part D: Prescription drug coverage

• Part A: Hospital coverage

• Part B: Doctor visits and outpatient care

• Part D: Prescription drug coverage

• Enroll in Part D when first eligible to avoid penalties

• Compare Part D plans annually during open enrollment

• Consider generic alternatives to reduce costs

• Assuming Original Medicare covers prescriptions

• Forgetting to enroll in Part D on time

• Not comparing plans annually

If a 55-year-old contributes the maximum to an HSA in 2023 ($3,650 for individual), and invests it with an average return of 6% annually, how much will they have at age 65?

Step 1: Calculate number of years = 65 - 55 = 10 years

Step 2: Use future value of annuity formula

FV = PMT × [((1 + r)^n - 1) / r]

FV = $3,650 × [((1.06)^10 - 1) / 0.06]

FV = $3,650 × [(1.7908 - 1) / 0.06]

FV = $3,650 × [0.7908 / 0.06]

FV = $3,650 × 13.18 = $48,107

Therefore: They will have approximately $48,107 at age 65.

This problem demonstrates the triple tax advantage of HSAs: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. The calculation shows how consistent contributions to an HSA can accumulate significant funds over time, especially when invested. This money can be used tax-free for healthcare expenses in retirement.

HSA (Health Savings Account): Tax-advantaged account for medical expenses

Triple Tax Advantage: Tax-deductible contributions, tax-free growth, tax-free withdrawals

Future Value of Annuity: Value of regular contributions at future date

• Must be enrolled in HDHP to contribute

• Catch-up contributions allowed after age 55

• Funds roll over year to year

• Contribute the maximum if financially feasible

• Invest HSA funds for long-term growth

• Save receipts for tax-free reimbursement later

• Not contributing to HSA despite eligibility

• Using HSA funds for non-medical expenses before 65

• Not investing HSA funds for long-term growth

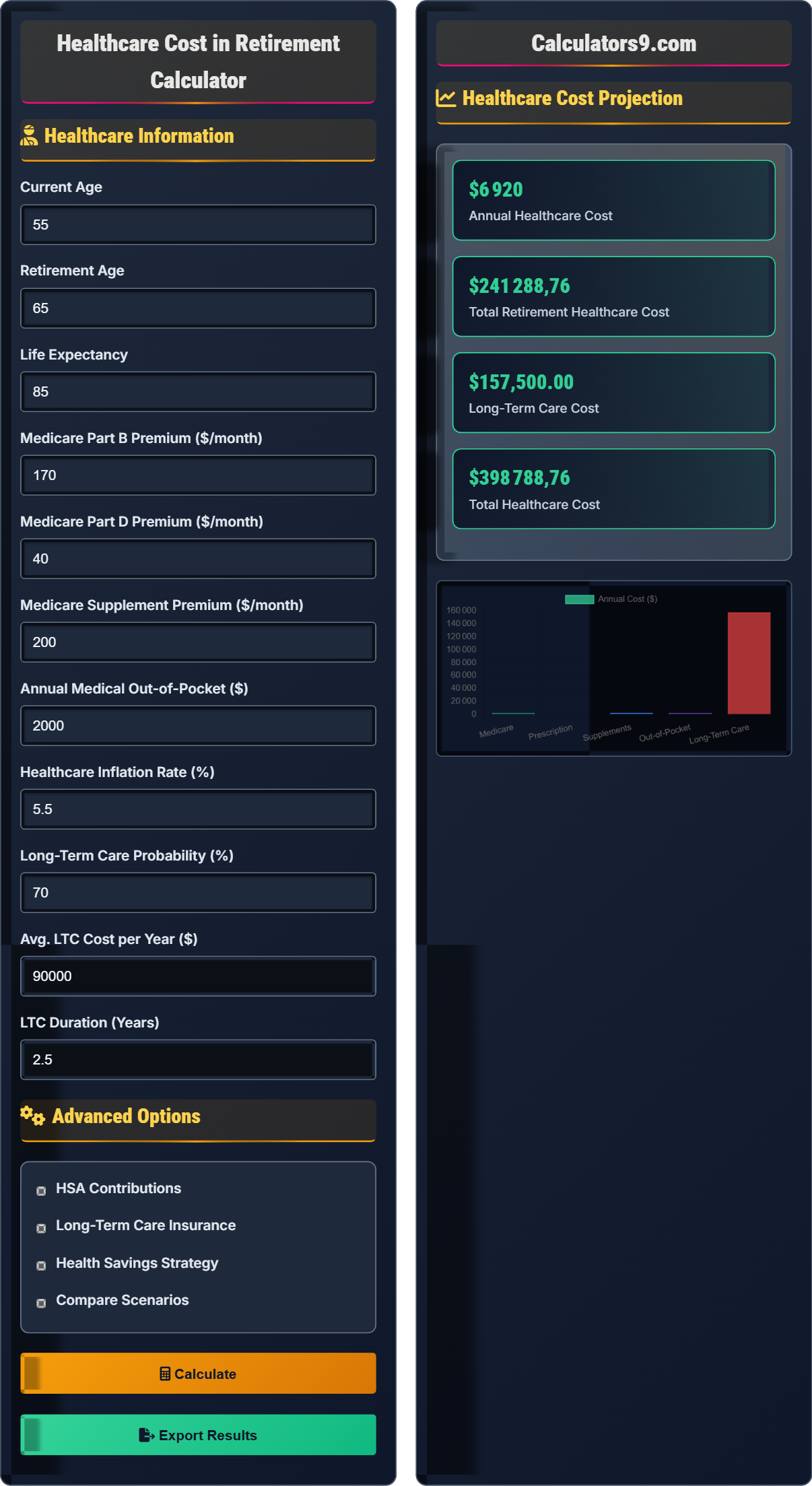

Sarah is 60 years old and estimates a 70% chance of needing long-term care for 2.5 years at an average cost of $90,000 per year. If healthcare costs increase by 5% annually, what is the present value of her expected long-term care costs at age 65?

Step 1: Calculate total LTC cost at age 65

Future cost per year = $90,000 × (1.05)^5 = $90,000 × 1.276 = $114,840

Total LTC cost = $114,840 × 2.5 years = $287,100

Step 2: Calculate expected cost based on probability

Expected LTC cost = $287,100 × 0.70 = $200,970

Step 3: Calculate present value using 3% discount rate

Present Value = $200,970 ÷ (1.03)^5 = $200,970 ÷ 1.159 = $173,400

Therefore: The present value of expected LTC costs is $173,400.

This problem demonstrates how to calculate the present value of future healthcare costs considering probability. The calculation involves three steps: projecting future costs with inflation, adjusting for probability of occurrence, and discounting back to present value. This approach helps determine how much to save today to cover expected future costs.

Long-Term Care: Extended care services for chronic illness or disability

Present Value: Today's value of future cash flows

Expected Value: Probability-weighted average outcome

• LTC costs grow faster than general inflation

• About 70% of seniors need LTC at some point

• Average LTC duration is 2-3 years

• Consider long-term care insurance for younger retirees

• Look into hybrid life/LTC policies

• Research state partnership programs

• Underestimating probability of needing LTC

• Not accounting for inflation in LTC costs

• Assuming family will provide free care

John is turning 65 and has $100,000 in his HSA. He estimates annual Medicare costs of $4,000 (Part B, D, and supplements) plus $2,000 in out-of-pocket expenses. How many years can he cover these costs with his HSA before depleting the account?

Step 1: Calculate total annual healthcare costs

Annual costs = Medicare premiums + Out-of-pocket = $4,000 + $2,000 = $6,000

Step 2: Calculate number of years HSA will last

Years = HSA balance ÷ Annual costs = $100,000 ÷ $6,000 = 16.67 years

Step 3: Consider HSA growth if invested

If HSA grows at 5% annually: $100,000 × (1.05)^10 = $162,890

With growth, HSA would last longer as the balance increases

Therefore: Without growth, HSA covers 16-17 years. With investment growth, significantly longer.

This problem demonstrates how an HSA can serve as a healthcare retirement account. The calculation shows that a $100,000 HSA can cover about 16-17 years of average healthcare costs. However, if the HSA is invested and grows, the account can last much longer due to compound growth. This highlights the importance of both contributing to and investing HSA funds.

HSA Depletion: When account balance reaches zero

Healthcare Budget: Annual healthcare cost requirements

Compound Growth: Growth on previous growth

• HSA funds roll over year to year

• After 65, HSA can be used for any purpose

• Tax-free for qualified medical expenses

• Keep receipts to reimburse yourself later

• Invest HSA funds for long-term growth

• Use other funds for current medical expenses

• Not maximizing HSA contributions

• Using HSA for non-medical expenses before 65

• Not investing HSA for growth

Healthcare costs typically rise at what rate compared to general inflation?

The answer is C) Faster than general inflation. Healthcare costs have historically risen faster than general inflation. While general inflation might average 2-3% annually, healthcare costs often rise 4-6% annually. This differential growth means healthcare will consume an increasing portion of retirement budgets over time. For example, if general inflation is 2% and healthcare inflation is 5%, healthcare costs will double in about 14 years versus 35 years for general costs.

This question addresses a critical planning consideration: the differential inflation rates between healthcare and general expenses. Because healthcare costs rise faster than general inflation, the percentage of retirement income devoted to healthcare will increase over time. This is why healthcare costs are often the largest expense in later retirement years, even if they seem manageable initially.

Healthcare Inflation: Annual increase in medical costs

General Inflation: Overall price level increase

Differential Growth: Different rates of increase

• Healthcare inflation typically 4-6% annually

• General inflation typically 2-3% annually

• Difference compounds over time

• Plan for 5% annual healthcare inflation

• Use higher inflation rates for longer retirements

• Consider this when estimating healthcare costs

• Using general inflation rate for healthcare costs

• Not accounting for differential growth

• Underestimating long-term impact

Healthcare Planning Basics

Medicare, HSA, long-term care, and healthcare inflation.

Annual Healthcare Cost = Medicare Premiums + Out-of-pocket + LTC Costs

Present Value = Future Value ÷ (1 + r)^n

HSA Growth = Principal × (1 + r)^n

- Healthcare costs rise faster than general inflation

- HSA offers triple tax advantage

- 70% of seniors need long-term care

Planning Strategies

Maximize HSA contributions and plan for long-term care.

- Maximize HSA contributions

- Invest HSA funds for growth

- Research long-term care options

- Plan for inflation

- Healthcare costs increase with age

- Medicare doesn't cover everything

- Long-term care insurance may be beneficial

- Consider health status in planning

FAQ

Q: How can I estimate my healthcare costs if I'm in good health now?

A: Even healthy individuals should plan for increasing healthcare costs:

Baseline Estimates:

- Medicare Part B premium: $170/month (2023)

- Medicare Part D: $30-50/month

- Medigap Plan G: $150-300/month

- Out-of-pocket costs: $2,000-5,000 annually

Age-Based Increases:

- Costs typically increase 3-5% annually

- Major cost jumps around age 80+

- Chronic conditions become more likely

Example Calculation: For a 65-year-old, average first-year costs are $4,000-6,000. Over 20 years with 4% annual increases, total costs could reach $120,000-150,000. This doesn't include potential long-term care costs.

Plan conservatively by using average costs for your age group, then adjust as your health status changes. Consider that health can deteriorate suddenly, so it's better to overestimate than underestimate.

Q: Should I purchase long-term care insurance or self-insure?

A: The decision depends on your financial situation:

Long-Term Care Insurance is Better If:

- Annual premium is 1-2% of assets

- You have substantial assets to protect

- You're in good health for your age

- You want peace of mind

Self-Insurance is Better If:

- You have very high net worth (>$2M)

- Insurance premium is >3% of assets

- You're comfortable with risk

- You have other care resources

Example: If you have $500,000 in assets and LTC insurance costs $3,000/year, that's 0.6% of assets - likely worth it. But if you have $1,000,000 in assets and LTC costs $8,000/year (0.8%), you might consider self-insuring.

Consider hybrid life/long-term care policies which provide death benefits if LTC benefits aren't used.