Retirement Withdrawal Calculator

Safe withdrawal strategy • 2026 edition

Retirement Withdrawal Formulas:

- 4% Rule: Withdraw 4% of portfolio in first year, adjust for inflation

- Safe Withdrawal Rate: Portfolio value × 0.04 = First year withdrawal

- Sequence of Returns Risk: Early poor returns increase failure risk

- Remaining Balance: Previous balance × (1 + return) - withdrawal

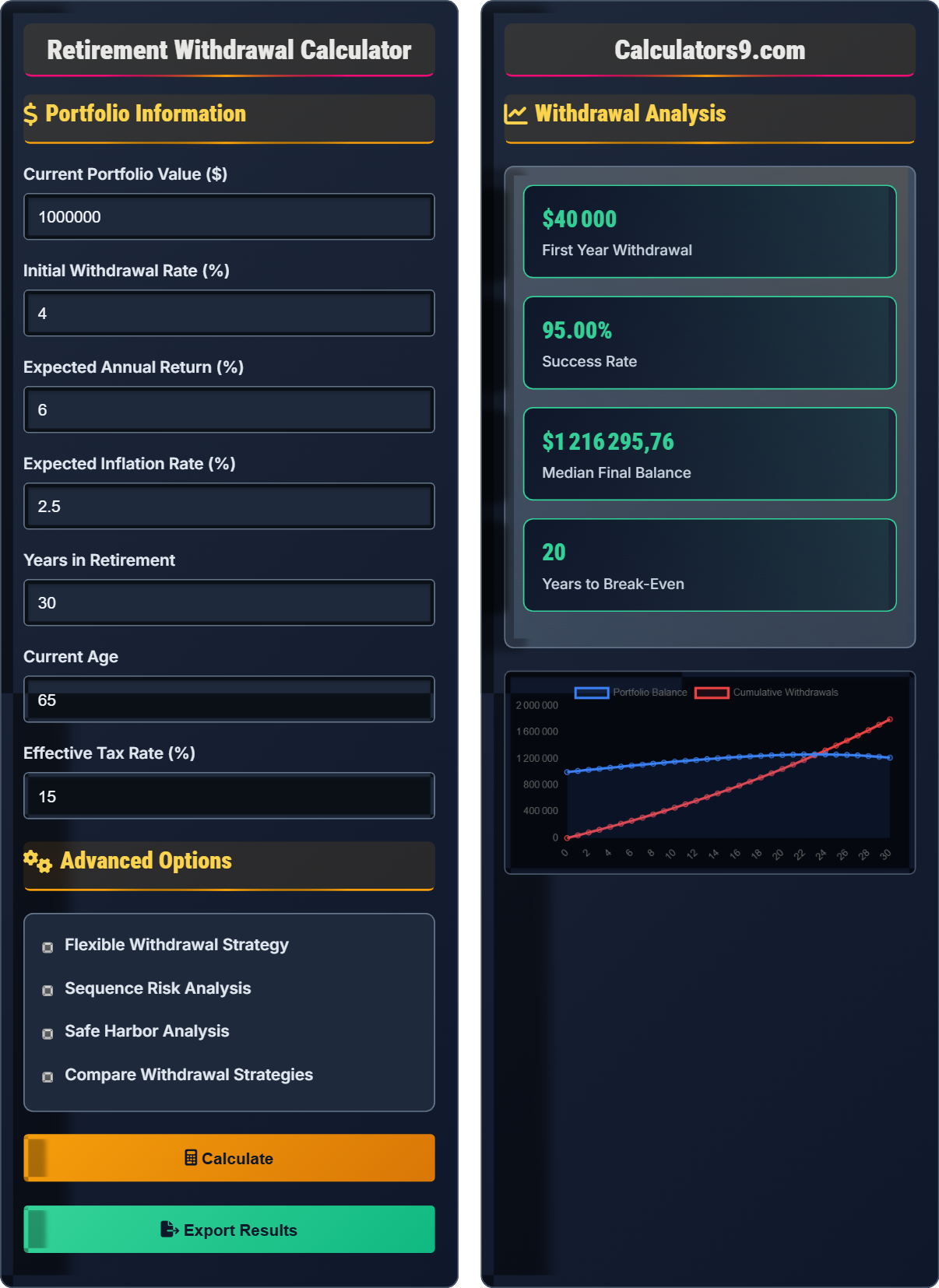

For example: $1,000,000 portfolio with 4% rule = $40,000 first year. If market gains 5% and inflation is 2%, second year withdrawal = $40,800.

Portfolio Information

Advanced Options

Withdrawal Analysis

| Year | Age | Withdrawal | Balance | Return |

|---|

| Metric | Value | Interpretation | Recommendation |

|---|

Retirement Withdrawal Planning

Safe withdrawal rates help retirees determine how much they can spend each year without running out of money. The famous "4% rule" suggests that withdrawing 4% of your initial portfolio value, adjusted for inflation each year, has historically sustained portfolios for 30 years in most market conditions.

Key methods for determining sustainable withdrawal rates:

- Fixed Percentage: Consistent percentage of portfolio value

- Variable Spending: Adjust based on market performance

- Bucket Strategy: Separate funds for different time horizons

- Guardrails Method: Floor and ceiling for withdrawals

- Dynamic Spending: Adjust based on remaining life expectancy

Critical risks to retirement portfolio sustainability:

- Sequence Risk: Poor returns early in retirement significantly impact success

- Inflation Risk: Rising costs eroding purchasing power over time

- Longevity Risk: Outliving your savings

- Market Risk: Volatility affecting portfolio value

- Interest Rate Risk: Changing rates affecting bond investments

- Dynamic Spending: Reduce withdrawals during market downturns

- Asset Location: Hold tax-efficient assets in taxable accounts

- Required Minimum Distributions: Plan for RMDs in withdrawal strategy

- Healthcare Planning: Account for HSA contributions and long-term care

- Legacy Planning: Balance spending with inheritance goals

Retirement Withdrawal Learning Quiz

According to historical analysis, the 4% rule has what approximate success rate for a 30-year retirement period?

The answer is C) 95%. The 4% rule, developed by financial planner William Bengen in the 1990s, showed that withdrawing 4% of an initial portfolio and increasing it annually for inflation would have sustained the portfolio for 30 years in 95% of historical scenarios since 1926. This became known as the "safe withdrawal rate."

This question tests understanding of the foundational research behind the 4% rule. Bengen's study analyzed historical market data and found that a 4% initial withdrawal rate had a 95% success rate over 30-year periods. The success rate considers the portfolio lasting the entire retirement period without being depleted. It's important to note that past performance doesn't guarantee future results.

Safe Withdrawal Rate: Annual percentage that can be withdrawn with high probability of lasting 30 years

Success Rate: Percentage of historical scenarios where portfolio lasted full retirement period

Historical Analysis: Study of past market returns to predict future outcomes

• 4% rule has ~95% success rate for 30-year retirement

• Success rate varies with portfolio allocation

• Past performance doesn't guarantee future results

• Consider lower rates for longer retirements

• Adjust for current market valuations

• Use flexible spending strategies

• Assuming 4% rule is guaranteed

• Not adjusting for portfolio composition

• Ignoring sequence of returns risk

If you have a $800,000 portfolio and use the 4% rule, what is your first-year withdrawal amount? If inflation is 3% in the first year, what will your second-year withdrawal be?

Step 1: Calculate first-year withdrawal = Portfolio value × Withdrawal rate

First-year withdrawal = $800,000 × 0.04 = $32,000

Step 2: Calculate second-year withdrawal = First-year withdrawal × (1 + inflation rate)

Second-year withdrawal = $32,000 × (1 + 0.03) = $32,000 × 1.03 = $32,960

Therefore: First-year withdrawal is $32,000 and second-year withdrawal is $32,960.

This problem demonstrates the mechanics of the 4% rule with inflation adjustments. The initial withdrawal is calculated as a percentage of the portfolio value. Each subsequent year, the withdrawal is increased by the inflation rate to maintain purchasing power. This adjustment helps preserve the retiree's standard of living despite rising costs.

Initial Withdrawal: First-year withdrawal calculated as percentage of portfolio

Inflation Adjustment: Annual increase to maintain purchasing power

Purchasing Power: Real value of money after accounting for inflation

• Initial withdrawal = Portfolio value × Withdrawal rate

• Subsequent withdrawals = Previous withdrawal × (1 + inflation)

• Adjustments maintain real spending power

• Track actual inflation rates each year

• Consider flexible adjustments based on portfolio performance

• Plan for periods of high inflation

• Forgetting to adjust for inflation each year

• Using average inflation instead of actual annual rates

• Not considering the compounding effect of inflation

Sarah retires with $1,000,000 and begins withdrawing $40,000 (4% rule). In her first three years, she experiences returns of -15%, -8%, and +5%. What is her portfolio value at the end of year 3, and how does this compare to the original portfolio value?

Step 1: Year 1 - Start with $1,000,000

Subtract withdrawal: $1,000,000 - $40,000 = $960,000

Apply return: $960,000 × (1 - 0.15) = $960,000 × 0.85 = $816,000

Step 2: Year 2 - Start with $816,000

Subtract withdrawal: $816,000 - $40,000 = $776,000

Apply return: $776,000 × (1 - 0.08) = $776,000 × 0.92 = $713,920

Step 3: Year 3 - Start with $713,920

Subtract withdrawal: $713,920 - $40,000 = $673,920

Apply return: $673,920 × (1 + 0.05) = $673,920 × 1.05 = $707,616

End of Year 3 Portfolio: $707,616

Decrease from original: ($1,000,000 - $707,616) ÷ $1,000,000 = 29.2%

Therefore: Portfolio value is $707,616 (29.2% decrease from original).

This problem illustrates sequence of returns risk - the danger of experiencing poor returns early in retirement. When withdrawals are made from a declining portfolio, the effect is compounded. The retiree not only faces a reduced portfolio value but also continues to withdraw the same dollar amount (adjusted for inflation), accelerating depletion. This demonstrates why early retirement losses are more damaging than late retirement losses.

Sequence Risk: Risk that poor returns early in retirement harm portfolio longevity

Portfolio Depletion: Running out of retirement savings

Compounding Effect: How losses magnify the impact of withdrawals

• Early losses have disproportionate impact on portfolio longevity

• Withdrawals from declining portfolio accelerate depletion

• Recovery takes longer from large early losses

• Maintain cash reserves for early retirement years

• Consider flexible withdrawal strategies

• Diversify across asset classes to reduce volatility

• Not accounting for the compounding effect of early losses

• Assuming average returns apply evenly over time

• Ignoring the impact of withdrawals during down markets

Tom uses a flexible withdrawal strategy with a floor of 2.5% and ceiling of 6% of portfolio value. If his portfolio drops from $1,000,000 to $750,000 due to market decline, what would his withdrawal be under this strategy compared to the traditional 4% rule?

Step 1: Calculate traditional 4% rule withdrawal on reduced portfolio

Traditional withdrawal = $750,000 × 0.04 = $30,000

Step 2: Calculate floor withdrawal = Portfolio × Floor rate

Floor withdrawal = $750,000 × 0.025 = $18,750

Step 3: Calculate ceiling withdrawal = Portfolio × Ceiling rate

Ceiling withdrawal = $750,000 × 0.06 = $45,000

Step 4: Determine actual withdrawal under flexible strategy

Since $30,000 is between the floor ($18,750) and ceiling ($45,000), the flexible strategy allows $30,000

However, some flexible strategies adjust to floor during severe declines

Therefore: Under traditional 4% rule, withdrawal is $30,000. Under flexible strategy, it could be reduced to $18,750 (floor) to preserve capital.

This problem demonstrates how flexible withdrawal strategies can protect against sequence risk. When portfolio values decline, rigid percentage-based withdrawals (like 4% rule) result in lower dollar amounts, but the impact on the portfolio is still significant. Flexible strategies with floors provide a minimum income while protecting the principal during downturns. The strategy can reduce withdrawals during market declines and increase them during good years.

Flexible Spending: Withdrawal strategy that adjusts based on portfolio performance

Floor Rate: Minimum withdrawal rate to preserve capital

Ceiling Rate: Maximum withdrawal rate to limit spending

• Flexible strategies adjust withdrawals based on portfolio value

• Floor protects against excessive spending during downturns

• Ceiling prevents overspending during good years

• Set realistic floor and ceiling rates

• Consider psychological impacts of reduced spending

• Plan for temporary spending reductions

• Setting floors too high to provide protection

• Not accounting for lifestyle adjustment needs

• Confusing flexible strategies with constant percentage rules

When implementing a retirement withdrawal strategy, which asset location approach is most tax-efficient?

The answer is B) Place tax-inefficient assets in tax-advantaged accounts. The most tax-efficient strategy is to hold tax-inefficient assets (like bonds, REITs, or actively managed funds that generate frequent distributions) in tax-advantaged accounts (401k, Traditional IRA) where they can grow tax-free or tax-deferred. Meanwhile, tax-efficient assets (like index funds, ETFs, or municipal bonds) should be held in taxable accounts where they generate minimal taxable events.

This question tests understanding of asset location - the strategic placement of different types of investments in the most tax-efficient account types. Tax-inefficient assets generate frequent taxable distributions, dividends, or capital gains that are better sheltered in tax-advantaged accounts. Tax-efficient assets produce minimal taxable events, making them suitable for taxable accounts. This strategy maximizes after-tax returns over the entire portfolio.

Asset Location: Strategic placement of investments in different account types

Tax-Inefficient Assets: Investments that generate frequent taxable distributions

Tax-Advantaged Accounts: Accounts with tax benefits (401k, IRA)

• Place tax-inefficient assets in tax-advantaged accounts

• Hold tax-efficient assets in taxable accounts

• Consider withdrawal order for tax efficiency

• Bonds and REITs are typically tax-inefficient

• Index funds and ETFs are tax-efficient

• Consider Roth conversions for tax diversification

• Placing tax-inefficient assets in taxable accounts

• Not considering withdrawal order in retirement

• Ignoring tax implications of different account types

Withdrawal Planning Basics

Safe withdrawal rates, sequence risk, and portfolio sustainability.

Initial Withdrawal = Portfolio Value × Withdrawal Rate

Adjusted Withdrawal = Previous Withdrawal × (1 + Inflation Rate)

Portfolio Balance = (Previous Balance - Withdrawal) × (1 + Return Rate)

- Start with conservative withdrawal rates

- Adjust for market performance

- Account for inflation annually

Optimization Strategies

Maximize portfolio longevity through diversified withdrawal strategies.

- Implement flexible withdrawal rules

- Optimize asset location

- Consider bucket strategies

- Plan for healthcare costs

- Health and longevity expectations

- Market conditions and valuations

- Tax implications of different account types

- Legacy planning goals

FAQ

Q: Should I adjust my withdrawal strategy if the market crashes early in retirement?

A: Yes, early retirement market crashes require immediate strategy adjustments:

Immediate Actions:

- Suspend COLA increases for 2-3 years

- Reduce withdrawal amount temporarily

- Shift to more conservative spending

- Delay major purchases or gifts

Portfolio Management:

- Rebalance to maintain target allocation

- Consider temporary shift to defensive assets

- Preserve remaining principal

- Look for opportunities during recovery

Example: If your portfolio drops 20% in the first year, consider reducing withdrawals by 10-15% for the next few years. This gives your portfolio time to recover before resuming normal withdrawal levels. The key is preserving capital during downturns.

Many retirees use a "guardrails" approach, setting floor and ceiling withdrawal rates to automatically adjust spending based on portfolio performance.

Q: How should I sequence my withdrawals from different account types?

A: The optimal withdrawal sequence depends on your specific situation:

General Order:

- Step 1: Taxable accounts (to let tax-advantaged grow)

- Step 2: Tax-advantaged (Traditional IRA/401k) - pay taxes now

- Step 3: Roth accounts (tax-free forever)

Exceptions to Consider:

- Large RMDs may change sequence

- High tax bracket years may alter strategy

- Healthcare costs may require taxable liquidity

- Legacy planning may preserve Roths

Example Sequence: Start with taxable account withdrawals to let tax-advantaged accounts continue growing. Once taxable is depleted, withdraw from Traditional accounts while managing tax brackets. Preserve Roths for later years when RMDs and Social Security create higher tax burdens.

Consider Roth conversions in low-income years to convert tax-advantaged to tax-free while managing tax brackets.