Social Security Estimator

Retirement planning tool • 2026 edition

Social Security Benefit Formulas:

- Primary Insurance Amount (PIA): Based on 35 highest earning years

- Full Retirement Age (FRA): 66-67 depending on birth year

- Early Retirement Penalty: 25-30% reduction for claiming at 62

- Delayed Retirement Bonus: 8% per year up to age 70

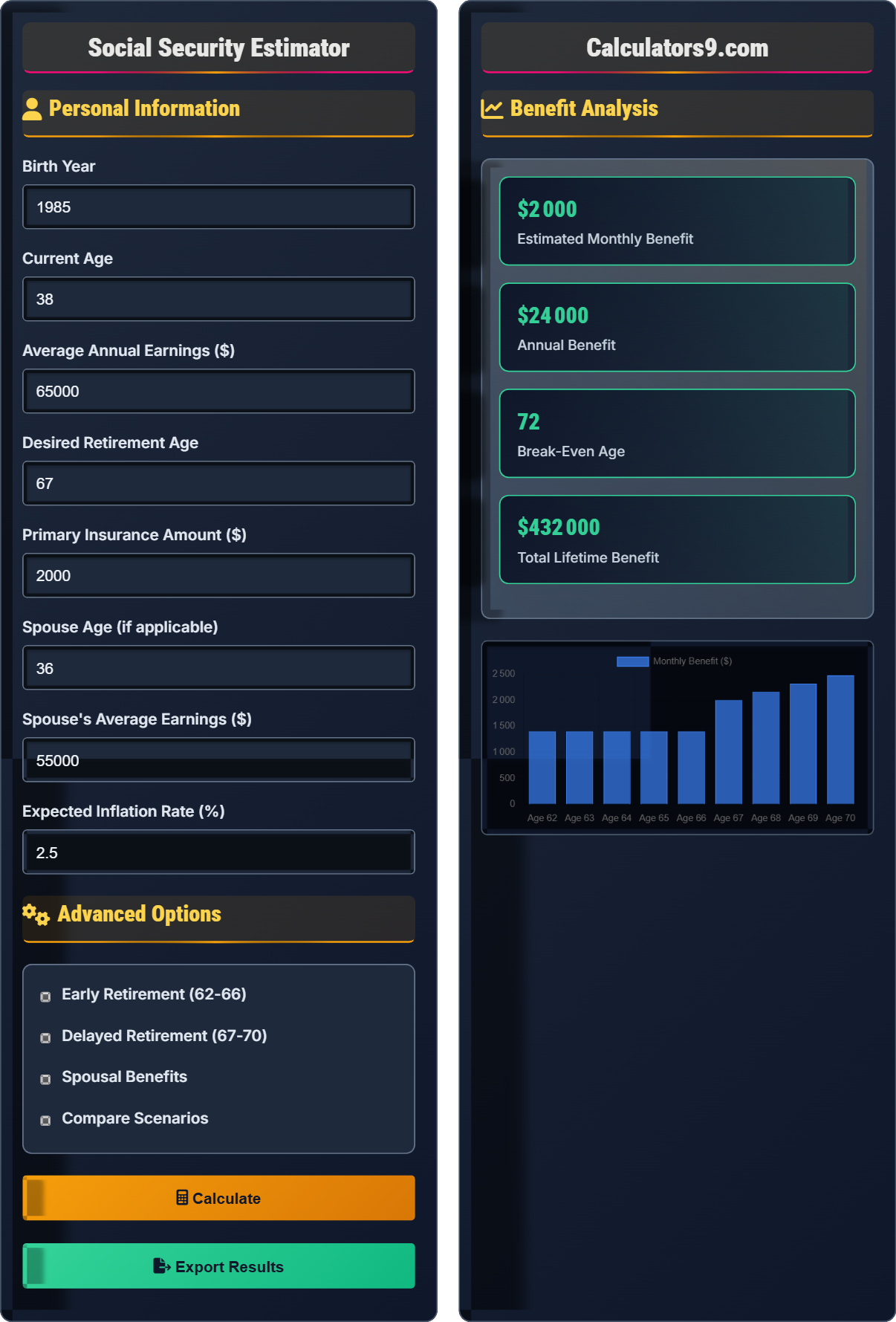

For example: With PIA of $2,000, claiming at 62 reduces benefits to $1,500 (-25%), while waiting until 70 increases to $2,640 (+32%).

Personal Information

Advanced Options

Benefit Analysis

| Scenario | Claiming Age | Monthly Benefit | Annual Benefit | Adjustment |

|---|

| Strategy | Advantages | Disadvantages | Best For |

|---|

Social Security Planning

Social Security benefits are calculated based on your 35 highest-earning years, adjusted for inflation. The system is designed to replace a higher percentage of income for lower earners than for higher earners. Understanding how benefits are calculated helps you make informed decisions about when to claim.

Key components of Social Security benefit calculation:

- Primary Insurance Amount (PIA): Base benefit amount

- Full Retirement Age (FRA): Age to receive full benefits

- Early Retirement Penalty: Permanent reduction for claiming early

- Delayed Retirement Bonus: Permanent increase for delaying

- Cost of Living Adjustments (COLA): Annual inflation adjustments

Reduction and bonus rates vary based on your birth year and claiming age:

- Early Retirement: 5/9% per month for first 36 months, 5/12% thereafter

- Delayed Retirement: 2/3% per month (8% per year) up to age 70

- Example (Born 1960+): 30% reduction at 62, 24% bonus at 70

- Health Considerations: Those with shorter life expectancy may benefit from early claiming

- Spousal Coordination: Coordinate claiming to maximize survivor benefits

- Working Past FRA: Delay claiming if continuing to work

- Survivor Benefits: Higher earner should delay to maximize survivor benefit

- Tax Planning: Consider tax implications of Social Security benefits

Social Security Learning Quiz

What is the Full Retirement Age (FRA) for someone born in 1960?

The answer is D) 67. For individuals born in 1960 or later, the Full Retirement Age is 67. The FRA gradually increased from 65 to 67 for those born between 1938 and 1960. This is the age at which you receive 100% of your Primary Insurance Amount (PIA).

This question tests knowledge of how Full Retirement Age has changed over time. The FRA was originally 65 for all workers, but Congress gradually increased it to address the financial challenges of Social Security. Workers born in 1937 or earlier have an FRA of 65, while those born in 1960 or later have an FRA of 67. This knowledge is essential for planning when to claim benefits.

Full Retirement Age (FRA): Age at which you receive 100% of your benefit

Primary Insurance Amount (PIA): Base monthly benefit amount

Birth Cohort: Group of people born in the same year

• Born 1937 or earlier: FRA = 65

• Born 1938-1959: FRA gradually increases from 65 to 67

• Born 1960+: FRA = 67

• Check SSA.gov for your specific FRA

• FRA affects early/late retirement penalties

• Consider your FRA when planning other retirement income

• Assuming FRA is always 65

• Not knowing how FRA affects benefit amounts

• Confusing FRA with early retirement age (62)

If someone's Primary Insurance Amount is $2,500 per month and they claim at age 62, what will their monthly benefit be? Assume they were born in 1960.

Step 1: Determine the reduction rate for claiming at 62

For those born in 1960+, claiming at 62 results in a 30% reduction from PIA

Step 2: Calculate the reduction amount = PIA × Reduction Rate

Reduction = $2,500 × 0.30 = $750

Step 3: Calculate the reduced benefit = PIA - Reduction

Reduced benefit = $2,500 - $750 = $1,750

Therefore: The monthly benefit will be $1,750.

This problem demonstrates the permanent reduction that occurs when claiming Social Security early. The 30% reduction is calculated from the Primary Insurance Amount and remains permanent for life. This reduction is applied monthly, so the person receives $750 less each month for life compared to waiting until Full Retirement Age. Over time, this adds up to hundreds of thousands of dollars in reduced lifetime benefits.

Primary Insurance Amount (PIA): Base monthly benefit at FRA

Early Retirement Penalty: Permanent reduction for claiming before FRA

Permanent Reduction: Benefit reduction that continues for life

• For 1960+ births: 30% reduction at age 62

• Reduction is calculated monthly

• Reduction is permanent for life

• Calculate the lifetime cost of early claiming

• Consider health and life expectancy

• Factor in other retirement income sources

• Forgetting that early reduction is permanent

• Not considering the lifetime impact

• Confusing reduction rates for different birth years

Sarah's PIA is $2,000 per month. If she claims at 62, she receives $1,500 per month. If she waits until 67, she receives $2,000 per month. At what age will she break even if she waits until 67 instead of claiming at 62?

Step 1: Calculate the total reduction by waiting

Monthly difference = $2,000 - $1,500 = $500

Years of early claiming = 67 - 62 = 5 years

Total early benefit = $1,500 × 12 × 5 = $90,000

Total delayed benefit = $2,000 × 12 × 5 = $120,000

Step 2: Calculate break-even point

Additional benefit per year after FRA = $500 × 12 = $6,000

Years to make up for early benefit = $90,000 ÷ $6,000 = 15 years

Break-even age = 67 + 15 = 82 years old

Therefore: Sarah will break even at age 82.

This problem demonstrates break-even analysis for Social Security claiming decisions. The analysis shows that waiting until Full Retirement Age results in a higher monthly benefit, but you miss out on 5 years of benefits by waiting. The break-even point is when the higher monthly benefit compensates for the missed early benefits. This calculation helps individuals decide whether to claim early or wait based on their expected lifespan.

Break-Even Analysis: When delayed benefits equal early benefits

Opportunity Cost: Benefits missed by waiting to claim

Lifetime Benefit: Total benefits received over a lifetime

• Break-even = Years to recover missed early benefits

• Higher monthly benefit = Faster recovery

• Life expectancy affects optimal claiming age

• Consider your health and family history

• Factor in spousal benefits

• Calculate break-even for different scenarios

• Not accounting for the time value of money

• Forgetting to consider inflation

• Assuming break-even is the only consideration

John's PIA is $2,800 and his wife Mary's PIA is $1,600. If John claims at 67 and Mary claims at 62, what is the maximum spousal benefit Mary could receive if it's greater than her own benefit? Assume Mary was born in 1960.

Step 1: Calculate Mary's reduced benefit at 62

Reduction for 1960 birth year at 62 = 30%

Mary's reduced benefit = $1,600 × (1 - 0.30) = $1,600 × 0.70 = $1,120

Step 2: Calculate the maximum spousal benefit

Maximum spousal benefit = ½ of John's PIA = $2,800 ÷ 2 = $1,400

Step 3: Determine which benefit Mary receives

Mary will receive the higher of her own reduced benefit ($1,120) or the spousal benefit ($1,400)

Since $1,400 > $1,120, Mary would receive $1,400 as a spousal benefit

Therefore: Mary would receive $1,400 per month as a spousal benefit.

This problem demonstrates spousal benefits, which can provide a higher benefit than one's own Social Security. Spouses can receive up to 50% of their partner's Primary Insurance Amount, but only if that exceeds their own benefit. This creates important coordination opportunities for married couples to maximize their total household benefits. The spousal benefit is not reduced if the spouse waits until FRA to claim.

Spousal Benefit: Up to 50% of spouse's PIA

Coordination: Strategic timing of benefits for couples

Survivor Benefit: Benefits for surviving spouse

• Spousal benefit = up to 50% of spouse's PIA

• Spouse receives higher of own benefit or spousal benefit

• Requires spouse to have claimed benefits

• Higher earner should generally delay to maximize survivor benefit

• Consider claiming strategies for both spouses

• Evaluate all possible combinations of claiming ages

• Not understanding that spousal benefits are reduced if claimed early

• Forgetting that own benefit is compared to spousal benefit

• Not considering survivor benefit implications

For someone born in 1960, what is the delayed retirement bonus for waiting until age 70 instead of 67?

The answer is A) 24%. For someone born in 1960, the Full Retirement Age is 67. The delayed retirement bonus is 8% per year for each year beyond FRA up to age 70. Waiting from 67 to 70 is 3 years: 3 × 8% = 24% bonus. So if the PIA is $2,000, waiting until 70 would increase it to $2,000 × 1.24 = $2,480 per month.

This question tests knowledge of delayed retirement credits. For each year you delay claiming beyond Full Retirement Age (up to age 70), you earn an 8% bonus on your Primary Insurance Amount. This is a guaranteed, inflation-adjusted return that cannot be matched by most investments. The bonus stops at age 70, so there's no benefit to waiting beyond that age.

Delayed Retirement Credit: Bonus for waiting to claim

Guaranteed Return: Guaranteed increase in benefits

Maximum Age: Age 70 is the latest to claim

• 8% bonus per year beyond FRA

• Maximum bonus at age 70

• No bonus for waiting beyond age 70

• The bonus is permanent for life

• Consider health and longevity expectations

• Factor in other income sources when deciding

• Thinking the bonus continues after age 70

• Not understanding that the bonus is permanent

• Confusing bonus rates for different birth years

Social Security Basics

Full Retirement Age, Primary Insurance Amount, and benefit calculation methods.

Early Retirement: PIA × (1 - Reduction Rate)

Delayed Retirement: PIA × (1 + Bonus Rate)

Spousal Benefit: MAX(Own Benefit, ½ × Spouse's PIA)

- Early claiming reduces benefits permanently

- Delayed claiming increases benefits permanently

- Maximum claiming age is 70

Claiming Strategies

Optimize claiming age based on health, life expectancy, and other income sources.

- Assess your life expectancy

- Consider spousal coordination

- Factor in other retirement income

- Calculate break-even points

- Health and family history

- Other income sources

- Spousal benefits and survivor benefits

- Current financial needs

FAQ

Q: I'm 63 and still working. Should I claim Social Security now or wait?

A: The decision depends on several factors:

Claiming at 63:

- 25% permanent reduction from your PIA

- Early access to benefits

- If earning above the annual limit ($21,240 in 2023), benefits may be temporarily reduced

Waiting until FRA:

- No reduction in benefits

- Full PIA amount

- No earnings limit

Considerations:

- Health and life expectancy

- Other retirement income sources

- Current financial needs

- Whether you plan to continue working

For someone born in 1960, FRA is 67. Each year you wait from 63 to 67 increases your benefit by about 8%, so waiting could significantly boost your lifetime benefits.

Q: How do spousal benefits work, and should my spouse and I coordinate our claiming strategies?

A: Spousal benefits and coordination are crucial for maximizing household income:

Spousal Benefit Rules:

- Up to 50% of higher-earning spouse's PIA

- Only available if higher earner has filed for benefits

- Reduced if claimed before own FRA

- Spouse receives higher of own benefit or spousal benefit

Coordination Strategies:

- Higher earner typically delays to maximize survivor benefit

- Lower earner may claim earlier and switch to spousal benefit later

- File and suspend strategy (if born before May 1, 1954)

- Restricted application for spousal benefit only (if born before May 1, 1954)

Example: If John's PIA is $2,800 and Mary's is $1,200, Mary could receive up to $1,400 as a spousal benefit (50% of John's PIA) if that's higher than her own benefit.

Proper coordination can significantly increase total household benefits over both lifetimes.