Deduction Estimator

Tax savings calculator • 2026 rates

Tax Deduction Formula:

Show the calculator\( T = (G - D) \times R \)

Where:

- \( T \) = Tax savings

- \( G \) = Gross income

- \( D \) = Total deductions

- \( R \) = Marginal tax rate

This formula calculates the tax savings from deductions by multiplying the deduction amount by your marginal tax rate.

Example: With gross income of \( G = \$100{,}000 \), total deductions of \( D = \$25{,}000 \), and a marginal tax rate of 22%:

Taxable income: \( 100{,}000 - 25{,}000 = \$75{,}000 \)

Tax savings: \( 25{,}000 \times 0.22 = \$5{,}500 \)

Thus, the taxpayer saves approximately $5,500 in taxes from deductions.

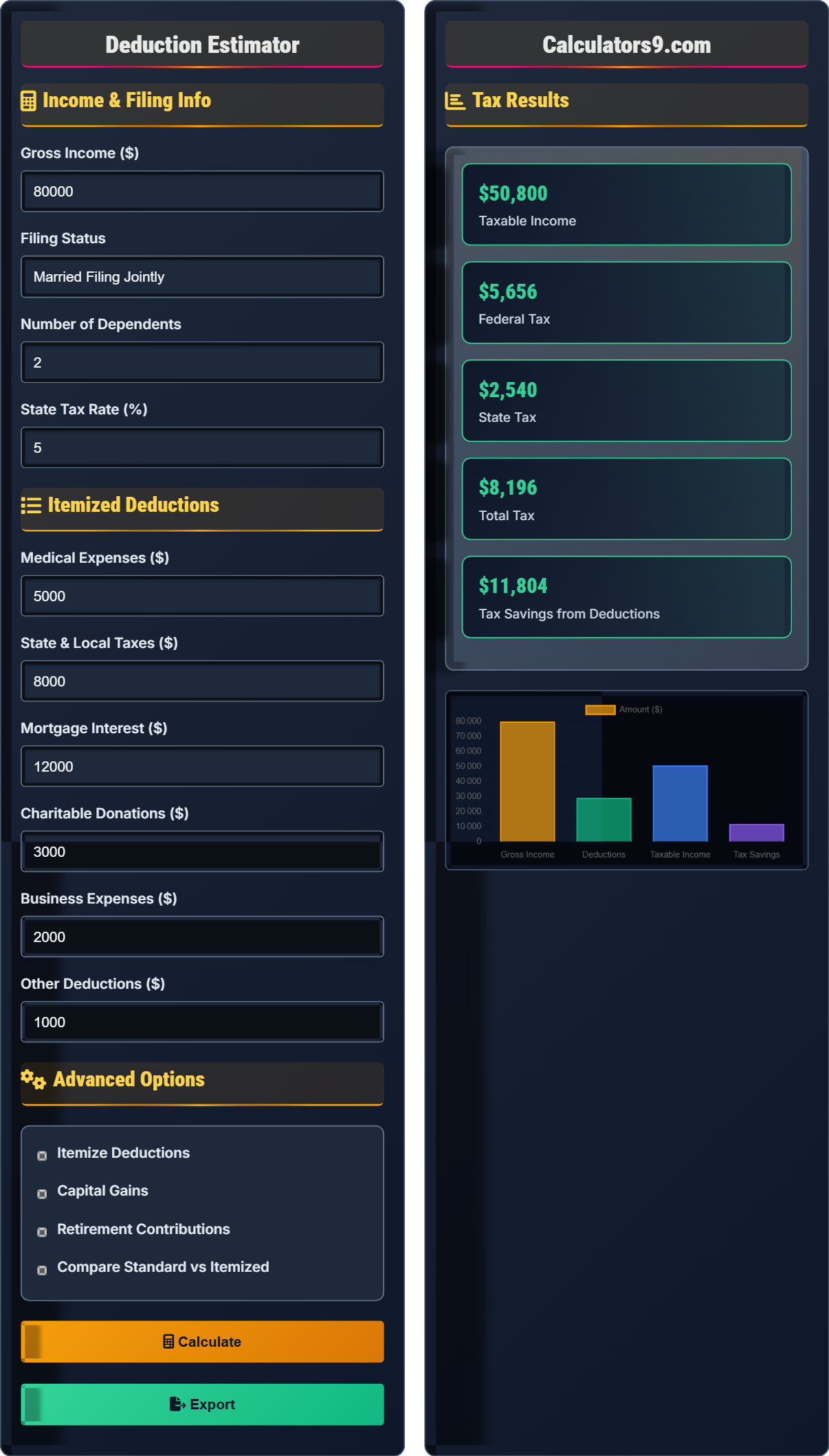

Income & Filing Info

Itemized Deductions

Advanced Options

Tax Results

| Deduction Type | Amount |

|---|---|

| Standard Deduction | $29,200 |

| Medical Expenses | $5,000 |

| State & Local Taxes | $8,000 |

| Mortgage Interest | $12,000 |

| Charitable Donations | $3,000 |

| Business Expenses | $2,000 |

| Other Deductions | $1,000 |

| Total Itemized | $31,000 |

| Scenario | Deduction | Taxable Income | Tax Savings |

|---|---|---|---|

| Standard Deduction | $29,200 | $50,800 | $10,000 |

| Itemized Deductions | $31,000 | $49,000 | $11,000 |

Comprehensive Tax Deduction Guide

Tax deductions are expenses that taxpayers can subtract from their gross income to reduce their taxable income. By lowering taxable income, deductions reduce the amount of tax owed. There are two main types of deductions: the standard deduction (a fixed amount) and itemized deductions (specific expenses).

The basic formula for calculating tax savings from deductions:

Where:

- \(T\) = Tax savings

- \(G\) = Gross income

- \(D\) = Total deductions

- \(R\) = Marginal tax rate

Popular deductions that can exceed the standard deduction:

- Medical Expenses: Only deductible if exceeding 7.5% of AGI

- State & Local Taxes: Capped at $10,000 combined

- Mortgage Interest: On loans up to $750,000 principal

- Charitable Donations: Up to 60% of AGI for cash donations

- Business Expenses: For self-employed individuals

- Bunching: Concentrating charitable donations in alternate years

- Timing: Accelerating deductions into high-income years

- Maximizing: Contributing to retirement accounts before year-end

- Tracking: Keeping receipts for all potential deductions

- Comparing: Calculating both standard and itemized annually

Deduction Basics

Expenses that reduce taxable income to lower tax liability.

\(T = (G - D) \times R\)

Where T=tax savings, G=gross income, D=deductions, R=rate.

- Itemize if deductions > standard deduction

- Medical expenses only if >7.5% of AGI

- SALT deduction capped at $10,000

Strategies

Choose standard or itemized based on which provides greater benefit.

- Track all eligible expenses

- Time deductions strategically

- Consider bunching charitable donations

- Maximize retirement contributions

- Standard deduction amounts vary by filing status

- Some deductions phase out at higher incomes

- Keep documentation for all claimed deductions

- Consider AMT impact on deductions

Tax Deduction Learning Quiz

Which of the following is TRUE about tax deductions?

The answer is C) Medical expenses are only deductible if they exceed 7.5% of AGI. The IRS allows medical expense deductions only for amounts that exceed 7.5% of adjusted gross income (AGI). For example, if your AGI is $50,000, only medical expenses over $3,750 ($50,000 × 0.075) are deductible.

Tax deductions follow specific thresholds and limitations set by the IRS. Understanding these rules is crucial because many taxpayers incorrectly assume all expenses are fully deductible. The medical expense threshold is designed to exclude routine healthcare costs and focus on significant medical burdens. This percentage-based threshold ensures that only substantial medical expenses provide tax benefits.

AGI: Adjusted Gross Income - gross income minus certain adjustments

Threshold: Minimum amount that must be exceeded before a deduction is allowed

Itemized Deductions: Specific expenses that taxpayers can claim instead of standard deduction

• Medical expenses must exceed 7.5% of AGI to be deductible

• State and local tax deductions are capped at $10,000

• Charitable donations are limited to 60% of AGI for cash contributions

• Remember "7.5% threshold" for medical expenses

• Use the acronym "SALT" for state/local tax limit of $10,000

• Claiming all medical expenses without considering the 7.5% threshold

• Assuming unlimited deductions for state/local taxes

Sarah has a gross income of $120,000 and itemized deductions totaling $35,000. The standard deduction for her filing status is $29,200. Her marginal tax rate is 24%. Calculate Sarah's tax savings from itemizing instead of taking the standard deduction.

1. Calculate the difference between itemized and standard deductions: $35,000 - $29,200 = $5,800

2. Multiply the difference by the marginal tax rate: $5,800 × 0.24 = $1,392

3. Sarah saves $1,392 in taxes by itemizing instead of taking the standard deduction.

This problem demonstrates the fundamental principle of tax deductions: they reduce taxable income, which reduces the tax owed. The key insight is that the tax savings equal the difference in deductions multiplied by the marginal tax rate. The marginal tax rate applies because each additional dollar of deduction reduces tax by the rate at which the next dollar of income would be taxed.

Marginal Tax Rate: The rate at which the last dollar of income is taxed

Standard Deduction: A fixed amount that reduces taxable income automatically

Itemized Deductions: Specific expenses that can exceed the standard deduction

• Tax savings = (Itemized - Standard) × Marginal tax rate

• Choose the higher of standard or itemized deductions

• Marginal tax rate applies to deduction savings

• Compare total itemized vs standard deduction amount

• Only itemize if total exceeds standard deduction

• Adding deductions instead of comparing them to standard

• Using average tax rate instead of marginal rate for savings calculation

FAQ

Q: When should I itemize deductions instead of taking the standard deduction?

A: You should itemize deductions when your total itemized deductions exceed the standard deduction amount for your filing status. For 2026, the standard deduction is $29,200 for married filing jointly, $14,600 for single filers, and $21,900 for head of household.

Mathematically, if your total itemized deductions (\(D_i\)) exceed the standard deduction (\(D_s\)), then itemizing saves you money:

\(Savings = (D_i - D_s) \times Marginal\_Tax\_Rate\)

For example, if your itemized deductions total $35,000 and the standard deduction is $29,200, you have an excess of $5,800. At a 24% marginal rate, this saves you $1,392 in taxes ($5,800 × 0.24). However, consider the time and effort required to track and document itemized deductions against the potential savings.

Q: How much of my mortgage interest can I deduct?

A: For mortgages taken out after December 15, 2017, you can deduct interest on up to $750,000 of qualified residence debt. For mortgages taken out before December 16, 2017, the limit is $1 million.

The calculation follows the formula:

\(Deduction = Min(Actual\_Interest, Interest\_on\_Qualified\_Debt)\)

Where qualified debt is the lesser of $750,000 ($1M for older loans) or the actual mortgage balance. For example, if you have a $800,000 mortgage with $30,000 in annual interest, only the interest on the first $750,000 is deductible. If the interest rate is 4%, that's $30,000 on $750,000, so you can deduct the full $30,000.