Present Value Calculator

Financial planning tool • 2026 rates

Present Value Formula:

Show the calculator\( PV = \frac{FV}{(1 + r)^n} \)

Where:

- \( PV \) = Present Value

- \( FV \) = Future Value

- \( r \) = Discount rate (as a decimal)

- \( n \) = Number of periods

This formula calculates the current worth of a future sum of money, taking into account the time value of money. The present value represents how much a future amount is worth today, given a specific discount rate.

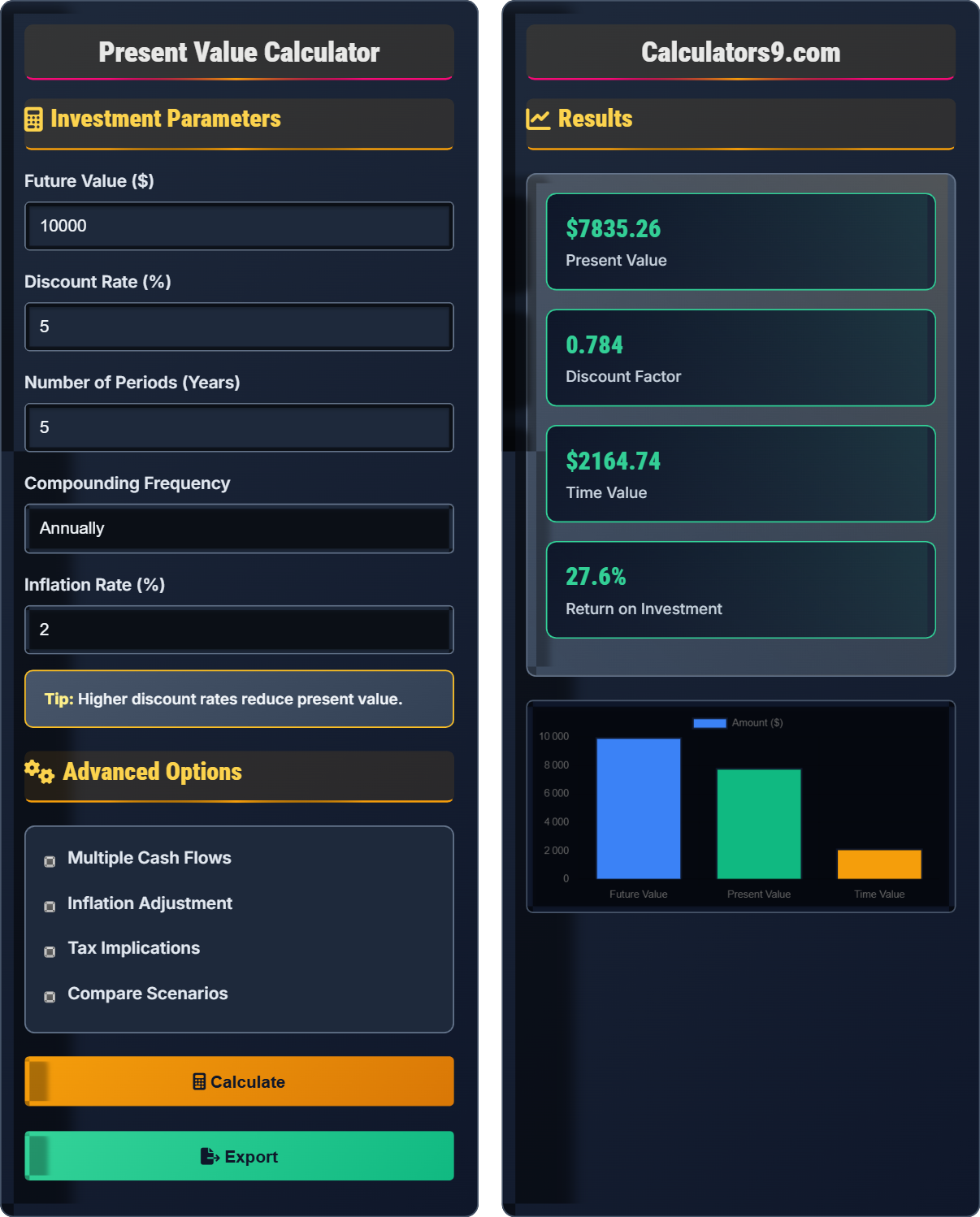

Example: To find the present value of \( FV = \$10{,}000 \) received in 5 years with a discount rate of 5%:

\( PV = \frac{10{,}000}{(1 + 0.05)^5} = \frac{10{,}000}{1.27628} \approx \$7{,}835.26 \)

Thus, the present value of $10,000 received in 5 years is approximately $7,835.26 today.

Investment Parameters

Advanced Options

Results

| Parameter | Value | Description |

|---|

| Period | Value | Discount Factor | Present Value |

|---|

Comprehensive Present Value Guide

Present Value (PV) is the current worth of a future sum of money or stream of cash flows given a specified rate of return. It's based on the principle that money available at the present time is worth more than the identical sum in the future due to its potential earning capacity.

The basic present value calculation uses the following formula:

Where:

- \(PV\) = Present Value

- \(FV\) = Future Value

- \(r\) = Discount rate (as a decimal)

- \(n\) = Number of periods

Several factors influence the present value calculation:

- Future Value: Higher future values increase present value

- Discount Rate: Higher rates decrease present value

- Time Period: Longer periods decrease present value

- Compounding Frequency: More frequent compounding affects PV

- Inflation: Reduces real purchasing power over time

- Investment Decisions: Evaluate profitability of projects

- Retirement Planning: Determine savings needed today

- Loan Analysis: Calculate present value of loan payments

- Bond Valuation: Assess bond worthiness

- Capital Budgeting: Net Present Value calculations

PV Fundamentals

Current worth of future cash flows.

\(PV = \frac{FV}{(1+r)^n}\)

Where PV=present value, FV=future value, r=rate, n=periods.

- Higher discount rates = lower PV

- Longer time periods = lower PV

- Higher future values = higher PV

Applications

Money today is worth more than money tomorrow.

- Investment evaluation

- Retirement planning

- Loan analysis

- Bond valuation

- Discount rate selection

- Inflation adjustment

- Tax implications

- Risk assessment

Present Value Learning Quiz

Why is the present value of $1,000 received in 5 years less than $1,000 today?

The answer is D) All of the above. The present value concept encompasses multiple factors: inflation reduces purchasing power over time, money available today can earn returns through investments, and there's uncertainty about receiving future payments. These combined factors mean that a dollar today is worth more than a dollar in the future.

The time value of money is a fundamental financial principle that explains why present value calculations are essential. This concept recognizes that money has earning potential and that future payments carry risk. Understanding this principle is crucial for making informed investment and financing decisions, as it allows for proper comparison of cash flows occurring at different times.

Time Value of Money: The principle that money available now is worth more than the same amount in the future

Opportunity Cost: The return that could be earned by investing money today

Discount Rate: The rate used to calculate present value, reflecting opportunity cost and risk

• Money has earning potential over time

• Future payments carry inherent risk

• Inflation erodes purchasing power

• Remember: Money today can be invested to earn returns

• Use higher discount rates for riskier investments

• Consider inflation when evaluating long-term investments

• Treating future and present money as equivalent without discounting

• Using inappropriate discount rates for the risk level

• Ignoring inflation effects in long-term calculations

Calculate the present value of $25,000 to be received in 8 years with a discount rate of 6%. Show your work.

Using the present value formula: \(PV = \frac{FV}{(1+r)^n}\)

Given:

- FV = $25,000

- r = 0.06 (6% as decimal)

- n = 8 years

Step 1: Calculate (1+r)^n = (1.06)^8 = 1.59385

Step 2: Calculate PV = $25,000 ÷ 1.59385 = $15,686.42

Therefore, the present value is $15,686.42.

This calculation demonstrates the inverse relationship between time and present value. As the time horizon increases, the present value decreases significantly. The compounding effect of the discount rate over 8 years reduces the future value by nearly 40%. This illustrates why long-term investments require careful consideration of the time value of money.

Future Value (FV): The amount of money expected in the future

Discount Rate (r): The rate used to discount future cash flows

Periods (n): The number of time periods until receipt

• Always convert percentages to decimals for calculations

• The discount factor is 1/(1+r)^n

• Present value is always less than future value (when r > 0)

• Use a calculator for exponent calculations

• Double-check decimal conversion of percentages

• Verify that PV is less than FV (when discount rate is positive)

• Forgetting to convert percentages to decimals

• Incorrectly calculating the exponent

• Getting PV greater than FV with positive discount rate

You have the option to receive $50,000 in 10 years or $30,000 today. If your discount rate is 7%, which option has a higher present value? By how much?

Step 1: Calculate the present value of $50,000 in 10 years at 7%:

\(PV = \frac{50,000}{(1.07)^{10}} = \frac{50,000}{1.96715} = \$25,417.46\)

Step 2: The present value of $30,000 today is simply $30,000

Step 3: Compare the options: $30,000 > $25,417.46

Step 4: Difference = $30,000 - $25,417.46 = $4,582.54

Therefore, receiving $30,000 today has a higher present value by $4,582.54.

This problem demonstrates the practical application of present value in decision-making. By converting future cash flows to their present value, we can make direct comparisons between different timing options. This is essential for investment decisions, loan evaluations, and financial planning. The calculation shows that despite the larger future amount, the present value is significantly reduced due to the time value of money.

Net Present Value (NPV): Difference between present value of cash inflows and outflows

Decision Criterion: Choose option with highest NPV

Comparative Analysis: Converting cash flows to same time period for comparison

• Convert all cash flows to the same time period for comparison

• Higher present value indicates better investment opportunity

• Consider the appropriate discount rate for risk level

• Always bring all cash flows to the same time period

• Use consistent discount rates for comparison

• Consider the context of the discount rate (risk-free vs. risky)

• Comparing cash flows at different time periods without discounting

• Using inconsistent discount rates for comparison

• Not considering the time value of money in decisions

Calculate the present value of $100,000 to be received in 15 years at three different discount rates: 4%, 7%, and 10%. How sensitive is the present value to changes in the discount rate?

At 4%: \(PV = \frac{100,000}{(1.04)^{15}} = \frac{100,000}{1.80094} = \$55,526.45\)

At 7%: \(PV = \frac{100,000}{(1.07)^{15}} = \frac{100,000}{2.75903} = \$36,244.60\)

At 10%: \(PV = \frac{100,000}{(1.10)^{15}} = \frac{100,000}{4.17725} = \$23,939.16\)

The present value ranges from $55,526.45 at 4% to $23,939.16 at 10%, showing a sensitivity of $31,587.29 between the lowest and highest discount rates.

Therefore, the present value is highly sensitive to changes in the discount rate, with a 150% increase in rate (from 4% to 10%) resulting in a 57% decrease in present value.

This sensitivity analysis demonstrates the critical importance of selecting an appropriate discount rate. Small changes in the discount rate can lead to significant differences in present value calculations, especially for longer time horizons. This is why financial analysts perform sensitivity analyses to understand how different assumptions affect investment valuations. The exponential nature of the discounting formula amplifies these effects over time.

Sensitivity Analysis: Testing how changes in input parameters affect output

Discount Rate Sensitivity: How present value changes with discount rate

Exponential Decay: The mathematical property causing rapid decline in PV

• Present value is exponentially sensitive to discount rate

• Sensitivity increases with longer time horizons

• Higher discount rates cause steeper reductions in PV

• Perform sensitivity analysis for critical investment decisions

• Use ranges of discount rates to assess risk

• Consider worst-case and best-case scenarios

• Using a single discount rate without sensitivity analysis

• Underestimating the impact of discount rate changes

• Not considering risk-adjusted discount rates

Which of the following statements about present value calculations is TRUE?

The answer is D) Both B and C are correct. Let's examine each option:

A) False - Present value decreases with higher discount rates

B) True - As time periods increase, the denominator (1+r)^n becomes larger, reducing the present value

C) True - When r = 0, PV = FV/(1+0)^n = FV/1 = FV

Therefore, both B and C are correct statements about present value calculations.

Understanding the relationships in present value calculations is crucial for financial analysis. The formula PV = FV/(1+r)^n shows that present value is inversely related to both the discount rate and the time period. When the discount rate is zero, there's no time value of money, so present value equals future value. These relationships help explain why long-term investments require careful consideration of discount rates and time horizons.

Inverse Relationship: As one variable increases, the other decreases

Compound Interest: Interest earned on both principal and accumulated interest

Discount Factor: The multiplier applied to future value to get present value

• Present value decreases with higher discount rates

• Present value decreases with longer time periods

• At zero discount rate, PV equals FV

• Remember that PV and discount rate have an inverse relationship

• Longer time periods result in smaller present values

• Zero discount rate means no time value of money

• Confusing the direction of the relationship between PV and discount rate

• Forgetting that time periods affect present value

• Not understanding the special case when discount rate is zero

FAQ

Q: How do I choose the appropriate discount rate for present value calculations?

A: Selecting the appropriate discount rate is crucial for accurate present value calculations. The discount rate should reflect the opportunity cost of capital and the risk associated with the cash flows.

For risk-free investments, use the rate of return on government securities (like Treasury bonds). For example, if a 10-year Treasury bond yields 3.5%, that could be your discount rate for a risk-free cash flow in 10 years.

For risky investments, add a risk premium to the risk-free rate:

\( \text{Discount Rate} = \text{Risk-Free Rate} + \text{Risk Premium} \)

Common benchmarks include:

- Corporate bonds: 4-8% depending on credit rating

- Stock market: 8-12% average return

- Real estate: 6-10% depending on property type

- Private equity: 12-20% for high-risk investments

Remember that the discount rate is a critical assumption, and small changes can significantly impact the present value, especially for long-term cash flows.

Q: What's the difference between present value and net present value?

A: While related, Present Value (PV) and Net Present Value (NPV) serve different purposes:

Present Value (PV): Calculates the current worth of a single future cash flow or a series of future cash flows.

\( PV = \frac{FV}{(1+r)^n} \)

Net Present Value (NPV): Calculates the difference between the present value of cash inflows and the present value of cash outflows.

\( NPV = \sum \frac{\text{Cash Flow}_t}{(1+r)^t} - \text{Initial Investment} \)

For example, if you invest $10,000 today to receive $12,000 in one year at a 5% discount rate:

- PV of future cash flow: $12,000 ÷ (1.05) = $11,428.57

- NPV: $11,428.57 - $10,000 = $1,428.57

NPV is used for investment decision-making, while PV is used to value individual cash flows.